|

|

|

Why Interest Rates Are Rising, and Will Keep on Rising (July 8, 2008) The standard financial forecast calls for sunny skies and low interest rates for the foreseeable future. As usual, it's wrong. Interest rates will rise longer and higher than anyone suspects. The reason is not complex. Money is a commodity like any other, and as a result it is ruled by supply and demand. When money is plentiful --that is, when banks have created money via extending credit to anyone with a pulse--then the cost is low. But when money supply shrinks--as in a credit contraction--then money becomes expensive. In other words, it costs more to use the money; interest rates rise. As the credit crunch/crisis shreds banks' ability to create money via credit, then interest rates will rise, regardless of what the Fed does or doesn't do. The Federal Reserve cannot repeal the influence of supply and demand, nor can it enable banks to create credit as their assets plummet. Finally, it cannot force consumers who have maxed out their credit and who face stunning drops in their own assets (houses, stocks, etc.) to borrow more. The virtuous cycle of exporting money to Asia in exchange for cheap goods and then watching China trade the dollars for Treasury bills to fund our stupendous deficits is ending as well. Those who believe China can "decouple" from the U.S. fail to weigh the reality that about 75% of the Chinese economy is export-based, in comparison to about 20% for exporters like the U.S. and Japan. Furthermore, China's GDP is grossly overstated by the usual purchasing power parity (PPP) methodology, as noted by Harold Brown of the Center for Strategic Studies in the March/April 2008 issue of Foreign Affairs:

Per capita GDP at PPP is a good measure of affluence, that is, the of the individual standard of living. Butt he appropriate measure of the potential influence of a national economy on the rest of the world is the national GDP at exchange rates.In other words, China is extraordinarily vulnerable to a reduction in exports. Its domestic economy is relatively tiny and largely dependent on exports for its growth. As the U.S. recession cuts imports from China, its surplus dollars will shrink, and so too will its ability to buy hundreds of billions more U.S. Treasury notes.

Even as the supply of money available to borrow is plummeting, the Federal government expects to borrow ever larger sums. Recall that U.S. borrowing (public and private) has been sucking up 80% of the entire world's savings for quite some time. As supply shrinks and demand rises, what happens to price? Even Bill Gross is admitting rates will have to rise: (link courtesy of Craig M.) Obama May Produce $1 Trillion Deficit, Gross Says

June 30 (Bloomberg) -- Bill Gross, manager of the world's biggest bond fund, said a Barack Obama administration may produce the first $1 trillion deficit and intermediate-and long- term bond yields have already reached cyclical lows.As the credit contraction spreads, interest rates for many are already zooming: Municipal Market `Fire in the Disco' Burns Borrowers:

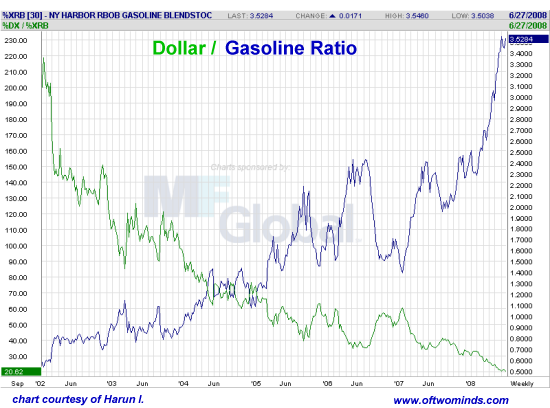

David Verinder, chief financial officer of the Sarasota Memorial Health Care System, received daily e-mail messages last month informing him that interest costs on an $83 million bond issue were rising to 1.45 percent, to 1.75 percent, to 3.25 percent, to 5.9 percent, and finally to 9 percent by June 24, a more than fivefold increase.The usual suspects are quick to suggest that all the Fed has to do is print money and buy the $1 trillion in US T-bills needed to fund the deficit. Sounds so carefree, but why hasn't the Fed pulled this trick in the past? Why sell trillions in bonds to non-U.S. investors if it is so easy to just "print money" and fund our trillion-dollar deficits that way? (Note: it isn't as easy as it sounds to "print money.") Could the answer be that there are disastrous consequences of such profligacy, such as the destruction of the dollar and our purchasing power? Take a look at this chart of the dollar/gasoline ratio, courtesy of Harun I. The green line depicts the actual ratio and the blue line is the raw futures price of Unleaded Gas:

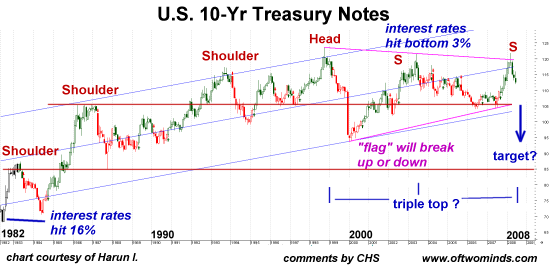

Are there technical reasons to suspect interest rates could be entering a 20-year upcycle? I asked frequent contributor Harun I. for comments. (Please note that I have marked up his chart according to my own interpretation).

There is both a bull case and a bear case for bonds. I believe the bull case to be limited in scope, however my opinion will not affect the way I trade.For further fundamental evidence of credit contraction and a reduction in the supply of credit, here are two stories courtesy of astute reader J.B.: BIS slams central banks, warns of worse crunch to come

A year ago, the Bank for International Settlements startled the financial world by warning that we might soon face challenges last seen during the onset of the Great Depression. This has proved frighteningly accurate. From a Bank for International Settlements (BIS) 2005 report:

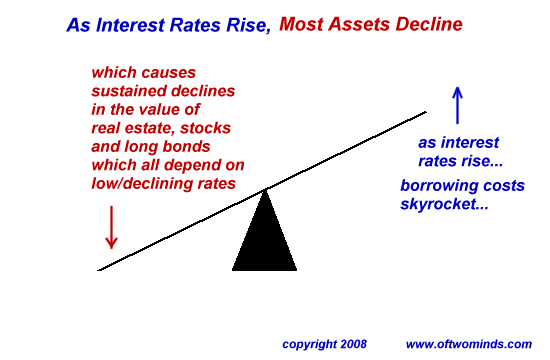

THE SUPERCYCLE OF DEBTIn summary: as credit contracts, money becomes dear. Interest rates rise. And as rates rise, real estate is slammed, stocks are slammed and existing bonds are slammed. All asset classes will decline in unison, leaving investors "no way out" except commodities, which will suffer their own contraction of demand as the global economy contracts sharply. In a nutshell: real estate and housing are entirely dependent on cheap, easily available credit. Once those disappear, real estate values fall. Why risk money in stocks, which historically earns 7% or so, if you can get 8% in short-term bonds? High interest rates destroy stock valuations. As interest rates rise, the market value of existing long bonds paying 3-4% interest will plummet, just as they did in the early 80s when rates rose sharply. If history offers any lessons, gold and cash earning high interest rates will outperform real estate, stocks and long bonds. Here is a visual display of the dynamic:

Put another way: how much longer will bond buyers accept a bond yield which doesn't even keep pace with the depreciation in the dollar's buying power? How much longer will they be content to lose money on every bond they buy? History suggests the answer is: not much longer. Interest rates dropped for 22 years, from 1981 to 2003. Could rates rise for the next two decades? The long waves of price interest rate movement provide clear historical evidence that the answer will categorically be "yes." NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Michael F. ($25), for your encouragement and very generous contribution to this

site.

I am greatly honored by your support and readership.

For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||