|

|

|

Of Onions and Oil: Don't Blame Speculators for Supply and Demand (July 10, 2008) Two seemingly unrelated reports--one on onions, one on oil--from frequent contributors fit together perfectly to destroy the popular notion that nasty, brutish speculators are to blame for big price fluctuations. You may be forgiven if your first reaction to this story (sent by Michael Goodfellow) is to reckon it parody: but it is the real pungent deal: What onions teach us about oil prices Onions have no futures market, yet their recent price volatility makes the swings in oil and corn look tame.

(Fortune Magazine) -- Before the U.S. Commodity Futures Trading Commission starts scrutinizing the role that speculators may have played in driving up fuel and food prices, investigators may want to take a look at price swings in a commodity not in today's news: onions.Now consider this report from the Commodity Futures Trading Exchange (sent by Harun I.) which dismantles the claim that speculators are the cause of oil's recent spike in price.

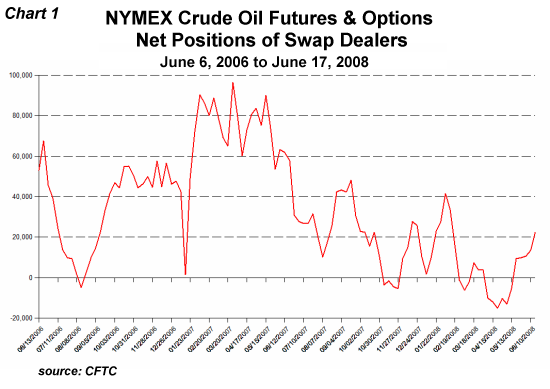

The 70% figure includes swaps dealers in the speculative category and includes only the long side positions of both swaps dealers and speculators, without showing, or netting against, short positions of almost equal size.

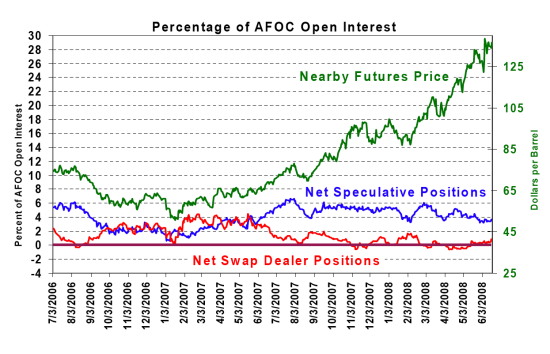

As we can easily see in this chart, net speculative positions have remained in a narrow band, and were actually considerably higher in 2006 than they are now.

Consider the role of "speculation" in securing predictable prices of fuel for airlines. Southwest Airlines reaps benefits of fuel hedging strategy:

What would it be like to pay $2 for a gallon of gasoline when everyone else is paying twice that much?So the net effect of banning speculation in petroleum products would be to force huge losses on Southwest, and possibly push them into bankruptcy. Good thinking, politicos--ban one of the few tools airlines and other transport companies have to lock in fuel prices. Speculation is a healthy and necessary part of any market. Outlaw it and you get 400% price swings--in onions, and everything else. If you want to finger the cause of $145/barrel oil, try the millions of autos in China (25,000 more added each day) that didn't exist five years ago, or the millions of new scooters and motorcycles tooling around India and other countries, and the profligate waste of fuel in oil exporting nations like Venezuela and Iran which heavily subsidize their citizens' gasoline prices. Or maybe the 21+ million barrels of oil we consume in the U.S.--fully 25% of total global demand--70% of which is burned for transportation. NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Tom S. ($50), for your amazingly generous contributions both financial

and intellectual to this site.

I am greatly honored by your support and readership.

For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||