This shadow inventory could reach as high as 7 million homes by some estimates;

other analysts reckon it will

take 103 months (about 8.5 years) to clear this

gigantic inventory of foreclosed, distressed and defaulted homes.

To put these numbers in context:

according to the U.S. Census Bureau, 51 million households have a mortgage and

24 million own homes free and clear (no mortgage), and about 37 million households rent.

Consider a fact that might be considered staggering in an environment in which "obvious" isn't

quite so manipulated:

the total number of vacant dwellings in the U.S. increased to

a record 19 million in the first quarter of the year, up from 18.9 million in the

fourth quarter. As new homes continued to be constructed, the housing inventory

rose last year by 1.14 million to 130.9 million, while occupied homes increased by

1.07 million to 111.9 million.

The Census Bureau reckons about 4 million of those vacant housing units are

vacation or second homes. Even if millions more of these vacant homes are in undesirable areas few

or suffering from severe structural issues, that still leaves

well over 10 million vacant dwellings in the U.S.--a truly monumental overhang of supply.

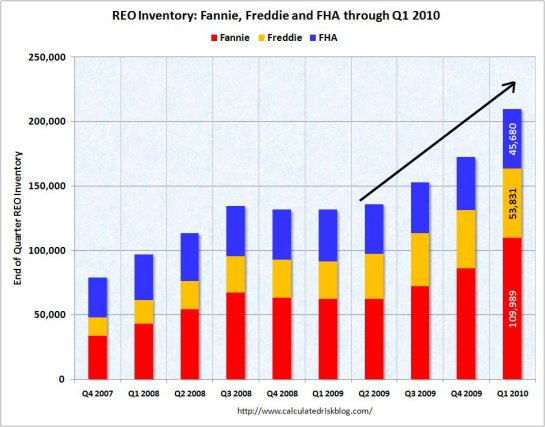

This inventory of vacant and/or defaulted dwellings is not static: as this chart

illustrates, the inventory of defaulting loans reverting to

Fannie Mae, Freddie Mac and the FHA is rising.

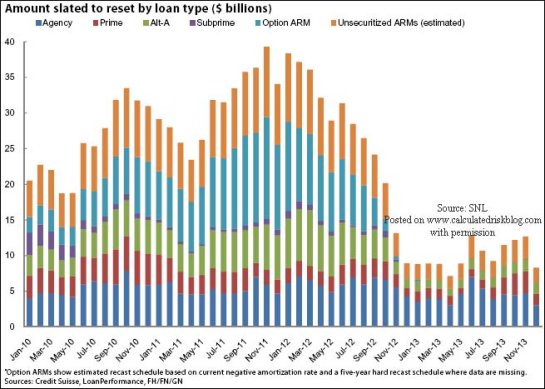

Then there is the looming surge of mortgage re-sets which will continue through 2012:

Given the imbalance between supply and demand, some housing observers are issuing

forecasts of 50% declines in housing values.

As I have noted here many times, the intervention in the nation's mortgage market

by the Federal Reserve and the Federal government via its GSEs Fannie and Freddie and its

housing loan agencies FHA and VA, is absolutely unprecedented in size and scope.

Government-backed loans accounted for 99%, or $1.5 trillion, of mortgage securities

in 2009. Banks and other private firms have issued a mere $15 billion. In addition,

the Federal Reserve and Treasury have spent nearly $1.25 trillion buying those bonds

to support the housing and broader credit markets. "The government is literally plowing

trillions of dollars into the U.S. mortgage market to keep it afloat," says Guy D.

Cecala, publisher of Inside Mortgage Finance.

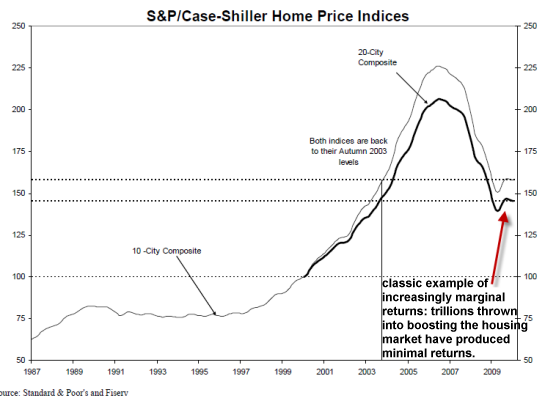

And what has been the result of this complete Federal/Fed absorption of mortgage risk?

A very modest blip up in home valuations, in certain highly desirable areas of the

nation. This is marginal returns writ large:

The Federal Reserve's exit from buying mortgages (if in fact it has actually ceased

propping up the nation's mortgage market) will eventually cause

mortgages to either rise in cost and/or become less readily available. Some analysts

see this unprecedented Fed intervention in what were once largely private mortgage

markets to be a development with

highly negative consequences going forward.

It is an understatement to say that the Fed, the Federal Housing Administration (FHA) and the government-sponsored

housing agencies, Fannie Mae and Freddie Mac, have not managed mortgage risk

very well;

FHA problem loans have risen to 24% of all loans originated in 2007,

and

taxpayers face $1 trillion in losses on Fannie and Freddie alone in the

years ahead.

The U.S. housing market is one defined by a rising supply and faltering demand,

and a total dependency on a

mortgage market propped up by

government or quasi-government agencies which have shown poor risk management in

service of sustaining or reinvigorating an unsustainable credit bubble.

These stupendous government interventions have simply staved off the consequences

of the supply-demand imbalance for the past two years. At some point these interventions

will fail and the returns on the investment will go negative: all the trillions

of dollars committed to propping up housing prices will fail to boost prices at all.

At that point public support for the prop-job will evaporate and the market will finally

get a chance to clear the imbalance between supply and demand.

Thank you, readers and contributors: As a result of your readership

and support, oftwominds.com is now a Page Rank 6 site. This may not seem like a big

deal, but the Google Page Rank is a basically impossible to "game" measure of

influence: not just the number of visitors or links, but a measure of link-ins,

scope and reach of content, etc. I am honored and humbled to reach PR 6. Special

thanks to Mary for suggesting the cool "Page Rank history" graphic in the right

sidebar.

If you would like to post a comment where others can read it, please go to

DailyJava.net,

(registering only takes a moment), select Of Two Minds-Charles Smith, and then go to The daily topic.

To see other readers recent comments, go to

New Posts.

Order Survival+: Structuring Prosperity for Yourself and the Nation and/or

Survival+ The Primer

from your local bookseller or from amazon.com or in ebook

and

Kindle formats

.