(June 15, 2009)

A quick glance at the "green shoots" rally is followed by a persuasive analysis

of the dollar's strength by correspondent B.C.

The favorite fantasy of the Powers That Be--that the U.S. economy

"is improving" and "the worst is over"--requires the "green shoots" Bull Market rally

to continue. Yet the melt-up enters its 14th straight week on wobbly

legs.

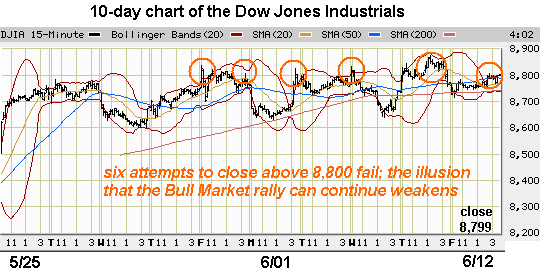

Over the past two weeks, the Dow Jones Industrial Average has attempted to close

above 8,800 on at least six occasions, and failed to do so each time.

This failure to break through to new technically persuasive highs has been mirrored

by the S&P 500, which traded for the past 7 days in an extremely narrow band:

6/4: 942.46

6/5: 940.09

6/8: 939.18

6/9: 942.43

6/10: 939.27

6/11: 944.89

6/12: 946.21

Everyone with even a passing interest in technical analysis has heard that "once the SPX

closes above 950 then that will trigger another leg up in this Bull Market." Hence

the PTB's (Powers That Be) desperation to stage a close over 8,800 on the DJIA and

above 950 on the SPX.

But exactly how much of the "green" in all those shoots have been spray-painted on dying

weeds of bad debt? Correspondent U. Doran sent in this article from Bloomberg

documenting that the EU has thrown staggering sums at its banking sector:

Bank Rescue Costs EU States $5.3 Trillion, More Than German GDP :

European governments have approved $5.3 trillion of aid, more than the annual

gross domestic product of Germany, to support banks during the credit crunch,

according to a European Union document.

The U.S. government and the Federal Reserve had spent, lent or committed $12.8

trillion, an amount that approaches the value of everything produced in the

country last year, as of March 31.

In other words, the gargantuan pillaging of public funds in the EU, an economy larger

than the U.S., is not even half the amount looted from the U.S. taxpayers.

The central banks of the major trading nations have thrown well over $20 trillion

(don't forget Chinese and Japanese "quantitative easing"/stimulus) of public funds into

their deleveraging, insolvent banking sectors, all in the vain hopes that the unwary

public will see spray-painted weeds as "green shoots" of organic economic recovery.

Have you noticed that every day the

market threatens to close lower, a sudden "rally" in the last 20 minutes gooses it higher

so that it once again closes within an unprecedented narrow band, day after day?

If that isn't manipulation, then why can you set your watch to the daily "rally"? That is

hardly a "random walk down Wall Street," is it?

OK, on to the main topic of the today: could the dollar be set to rise rather than fall?

Last week I posited in

The Dollar Conundrum: Poison or Cure? (June 11, 2009) that the dollar would

have to fall in half if not more just to correct unprecedented imbalances in trade

and capital flows.

Knowledgeable correspondent B.C. holds the opposite view, and he states the case for a much

stronger dollar very persuasively:

I am one of those rare birds who does not buy the US$ disaster scenario. Consider that

from the overvalued cyclical levels in '00-'02, the US$ fell ~53% in CPI-adjusted terms.

Adjusted for the price of gold, similarly adjusted for the US$ and CPI, the US$ fell 76%.

The US$ fell even more in the early '80s adjusted for CPI and gold. In effect, we've had

two colossal US$ crashes in less than 30 years. (emphasis added, CHS)

(While many would say that we have emerged

relatively unscathed from each episode to date, a closer examination of the underlying

productive structure of the economy, and what the Austrians refer to as the "pool of

funding", and the situation is much more dire than it appears on the surface.)

Then consider what would happen to the euro were the US$ Index to fall, say, another 50%

from ~80. The euro would effectively double to the 2.80s, plunging the European production

and export sectors further into a deeper hole than today. And the doubling or more of

commodities prices would very likely imply a further decline in global economic activity.

The value of the US$, as with all fiat, credit-money currencies, is determined by supply

and demand but also by the relative supply-demand and flows of "things" the fiat currencies

can buy. Note that commodities prices over the long term grow roughly at the rate of

overall GDP or population plus replacement and capital deepening and the incremental amount

of supply-demand inefficiencies or price signal distortions associated with gov't and

bankster mischief in the form of growth of bank loans and gov't deficit spending beyond

the economy's sustainable growth rate (again, at around replacement or population and the

capital required).

Adjusted for the changes in the fiat credit-money US$, commodities

prices as reflected by the CRB Index (overweighted by oil) are no higher than they were

34-35 years ago, including at or near the lows since the US$ was removed from gold.

One can infer from this currency-adjusted price profile that the supply-demand situation

for commodities is generally speaking at equilibrium.

The Chinese shifting some of their US$ reserves to hoarding commodities is prudent, one

might say given China's resource demands and runaway, unsustainable growth; but the action

creates distortions and artificially stronger short-term demand for commodities transacted

in US$'s, which in turn causes a feedback effect to the US$, requiring relatively more

US$'s to purchase a given amount of commodities at spot prices (or forward futures prices).

The Chinese hoarding thus causes incremental downward pressure on the US$ where there

otherwise would not be given the extent to which (1) US firms have been repatriating

US$'s from China-Asia as a result of reducing investment and thus being the proximate

cause of China's collapse in exports (which are really in large part goods being shipped

from US subsidiaries operating in China); and (2) the money multiplier and velocity

are plunging (and even more pronounced when adjusting GDP for total gov't spending),

which historically (and my inference) is not coincidentally bearish for the US$.

This sets up the increasing probability over time (perhaps very shortly hereafter) of

the price distortions reaching critical mass with China achieving the desired level of

hoarding of resources at current prices, setting up the potential thereafter for another

collapse in commodities prices (and corresponding firming and rally in the US$) when

slower trend global aggregate demand meets with the higher nominal commodities prices

and surplus capacity.

I expect just such a scenario to occur later this year and into early '10, including

the potential for another commodities and global stock price plunge and flight to the

US$ and Treasuries, suggesting that the US$ could more likely rally 25-30% than fall

25-50%. The emergence of sovereign debt and currency crises in the Baltic states, Eastern

Europe, and even Scandinavia, the UK, Ireland, and other countries in Europe suggest

that UK and European banks, and thus the euro, might be at more imminent risk at this

particular juncture than the US$.

I would also add that Mexico's deteriorating situation, including peak oil production

and revenues, collapse in remittances from the US, and increasing violence among drug

lords increase the risk of Mexico eventually becoming a failed state, which would also

create incremental demand for US$'s by wealthy Mexican nationals.

And as I have shared with you before, GDP PPP and flow equilibria among the three major

trading blocs, western, Japanese, and Chinese demographics, and long-term resource

constraints, i.e., Peak Oil and Peak Everything, going forward implies that, rather

than a US$ crash, the more likely outcome is all major fiat currencies will trend toward

or around par with one another, whereas nominal commodities prices sometime after the

early to mid-'10s begin an inexorable rise against ALL fiat currencies.

Moreover, in this context, I expect that the Anglo-American (and marginally German and

Dutch) Power Elite's goal of a global petro-currency or commodities-based proxy in the

form of a basket of major currencies is the likely outcome in the long run.

As a bit of an aside, the negative wealth effect from falling real estate and stock

prices has resulted in a GDP growth gap of ~25% from potential, which implies that US

real private GDP growth is likely to be 0% for the next 4-5 to 8-9 years. Little or no

growth further implies little growth bank lending, private investment, profits, and

payrolls, suggesting that any "growth" we see in the US economy in the next 5-10 years

will occur as a result of low-multiplier and low-velocity borrowing and spending by

the federal gov't in excess of the extent to which the private sector continues to

contract as a result of the growth gap.

In this no-growth context, consider that the S&P 500 trailing '09 P/E is now 136

(!!!) for reported earnings, and the '09 and '10 P/E versus earnings estimates is

27 and 38, whereas the dividend payout is again below 3%, now at ~2.3% or 150 bps

below the 10-year Treasury yield. Moreover, the P/E on the basis of the Aaa- and

Baa-rate corporate bond yields and spreads to Treasury yields is implied to be no

higher than ~13.

Thus, based on the reported '09 and '10 earnings estimates, the implicit "fair value"

(perpetually elusive in real time) for the S&P 500 is in the 300s-400s (US$ constant).

Valuations are again arguably back to the delusional "dot-con" levels of the late '90s

and at the most recent "echo-bubble" levels in '06-'07, setting up yet another potential

for a crash hereafter.

As for QE and deficit spending, the effects will depend in large part on how much of

the central bank credit-money reserves actually end up as bank loans/deposits versus

in bank holdings of gov't paper to fund deficit spending, and then to what extent the

net spending results in a deceleration or increase in the multiplier and velocity.

Japan's BOJ from '96-'97 expanded the monetary base by 12-20% per

annum through '03, but real and nominal private GDP did not grow much at all; bank landing

was flat to negative; Japanese banks and the BOJ became the lender of last result to the

Japanese gov't; outright price deflation persisted after '97; M2+ grow at only roughly

the average rate of net incremental gov't borrowing and spending related to social

service transfers; and the money multiplier and velocity plunged.

(BTW, most observers, analysts, and pundits are not aware that Japan did not experience

persistent price deflation until after '97, the point at which their peak demographic

drag effects on housing, consumption, and asset drawdown took hold, as ours is occurring

in the US today.)

With our money multiplier and velocity similarly plunging as occurred in Japan in the

late '90s to date, with total industry capacity utilization below 70%, and nominal

commodities prices firming and again set to bear down on business input and householders'

prices and thus profits and spending, price deflation and its drag effect on nominal

GDP growth will likely mean persistent deflation remains the likely outcome for the US,

Eurozone, and eventually China-Asia.

Goldman Sachs, Morgan Stanley, and JP Morgan going long commodities and index futures

(and doing so with funds received from debt and equity issuances, permitted by the

respite via TARP) by way of their trading desks and associated sponsored offshore hedge

funds, including their leveraged hot money flows to emerging markets, risks raising

struggling businesses' and indebted householders' costs, clipping the "green shoots"

before they reach ankle height.

Allow me to end by again stating that you have among the most well-written, insightful,

and informed Web sites I read on a daily basis. I don't know how you manage to keep it

consistently timely and compelling from week to week. I greatly admire your breadth

of knowledge, depth of intellect, writing skills, and tireless efforts.

Thank you, B.C. for the kind words and for sharing a persuasive contrarian analysis.

Correspondent Michael Surkan, author of the excellent

The case for deflation (PDF and podcast), also offered a dollar-positive

view:

After reading your piece on the "dollar conundrum," I just had to point out that not

everyone believes the dollar is set for significant near-term devaluation. In fact, a few

folks (such as myself), hold to the idea that dollar-denominated debt-deflation has barely

even started, and that we will see the dollar appreciate massively against all assets,

and other currencies, in the next few years.

By the way, this is not just bullish wishful thinking. If deflation really takes hold,

as I think it might, then the economy will be reeling from the collapse in asset values,

and spiraling numbers of loan defaults.

It is my belief that the recent weakness we have seen in the dollar of recent months is

simply a part of the broader bear market rally which is lifting stock, and asset, prices.

Sometime later this year, or in 2010, I expect this rally to peter out, and deflation

to once again grip the worlds economy (and America in particular) in a vice.

There you have it: the case for deflation and thus a stronger dollar. As I often

note: if it were easy to predict the future, we'd all be millionaires.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

--Walt Howard, commenting about CHS on another blog.

NOTE: contributions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

Thank you, Elizabeth R. ($50), for your stunningly generous contribution to this

site.

I am greatly honored by your support and readership.

Or send him coins, stamps or quatloos via mail--please

request P.O. Box address.

Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright ©

2009 Charles Hugh Smith, All rights

reserved in all media, unless otherwise credited or noted.

I would be honored if you linked this wEssay to your site, or printed a copy for your own use.