|

|

|

Re-Set (November 7, 2008) Thank you, readers, for your many emails and financial contributions over the past few days. I will respond to each one as I catch up. Metaphor and analogy are key constituents of human cognition. The right metaphor can "make sense" of what was disparate and apparently unrelated experiences and data. The most apt metaphor for the coming decade may well be "re-set." We're all familiar with electronic devices' reset buttons which return the device to its factory or default settings. In a similar fashion, a gigantic re-set button has been pushed which is returning the global economy to its pre-credit-bubble/pre-housing bubble settings. Since health and therapy metaphors are extremely popular nowadays, here's another way to think about the re-set. Take a male athlete's pulse and you get a rate of around 50 heartbeats per minute; a female athlete's will generally be somewhat higher. Now drive the athlete's nervous system haywire with crank, meth, uppers and every destructive stimulant you can lay your hands on. Now their pulse is erratic and pushing 90, even when they're sitting on the sofa fidgeting as they watch TV. That crazy destructive stimulant was the credit bubble, and the crazed, erratic hyped-up pulse was the global economy's velocity of money and ramped-up leverage. Take the poor athletes off the insane stimulants and the come-down is vicious. They feel like crap and are ill for some time. That's the global economy now. Well-meaning and/or desperate trainers then try to "make them feel better" with a hasty mix of supposedly safe stimulants, vitamin injections and all kinds of never-been-tested, seat-of-the-pants "treatments" which alas, only lengthen the athlete's wretchedness and recovery. That's the government interventions, bailouts, saves, rescue plans, loans, giveaways, etc. OK, back to the re-set metaphor. What exactly is being re-set to pre-credit-bubble settings/ranges? 1. Housing is re-setting to historic relationships with rents, wages and mortgage rates. Lower incomes and higher rates mean much lower housing prices, period, regardless of governmental "bailouts" and other fake/worthless stimulants being injected willy-nilly into the comatose patient. 2. Mortgage and borrowing costs are re-setting to higher, historically average rates. A mortgage at 9% was once considered cheap. The 3% teaser rates of the credit bubble are gone, as are the 5.25% fixed-rate mortgages of that era. The Fed can lower the Fed Funds rate to zero and mortgages will re-set to historic averages, as the forces of re-set are far more powerful than the twinkie little "Fed Funds rate" lever. The cliche during the credit-bubble boom (what I have long called Bogus Prosperity) was "don't fight the Fed." The re-set has erased that haywire garble and the global credit markets will raise rates regardless of the Fed's flailing and hyping and injecting (and perhaps praying). The interest-rate tide is rising at long last to levels which will reward savers and those holding capital and apply historic average costs on borrowers. Here's the dynamic effect of higher rates on asset values such as houses:

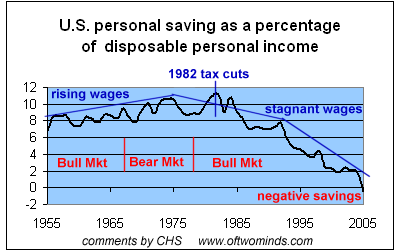

3. Savings rates will re-set to historic averages of 6-8%, rising from the negative savings rates of the credit bubble era. Without HELOC (home equity lines of credit) to inject "free money" stimulants, U.S. homeowners and former homeowners will have to revert to saving for future consumption and retirement.

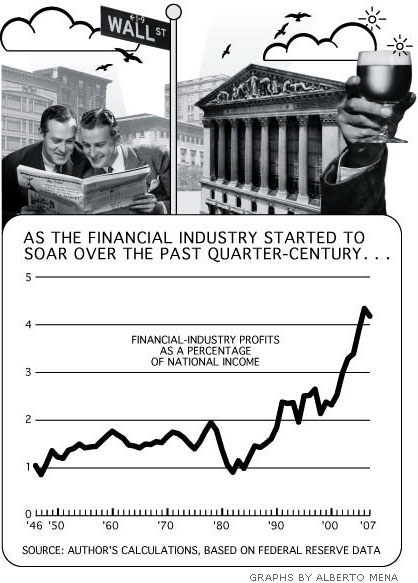

4. Taxes will re-set to historic percentages and ranges. I have documented this before, but the U.S. tax structure has become skewed in favor of corporations, super-high income elites and lower/middle-income households, many of whom pay no income taxes. Corporate taxes were a much higher percentage of total taxes in the 1950s and 1960s; any bump up in effective corporate taxes would simply be returning to historic norms. A restructured "minimum tax" (the infamous AMT) on the super-wealthy would also be a mere re-set to historic norms, not "new taxes on productive wealth." If the lower-middle class pays no income taxes, then the tax they do pay--the FICA (Social Security) tax will have to be bumped up as compensation. 5. The current account deficit (trade deficit) will re-set from -7% of GDP to a historic range of -1/-2% of GDP. Stupendous trade deficits were just one other crazed result of credit-bubble stimulants and low interest rates. 6. Public pensions will re-set from 80%/90% of highest salary to much lower historic ranges. Government promised pensions which were as bloated and unsustainable as the rest of the credit-bubble economy; regardless of public union protests and the promises made, pensions will come down by whatever means are forced: by negotiations if union leaders are wise and thoughtful, by municipal and state bankruptcy if they are strident and unwise. 7. Private consumption will fall from credit-bubble era 70% of GDP to much lower levels of 50%-60% of GDP. The free-spending, free-borrowing private consumption boom is over; private spending will re-set to levels trillions of dollars per year lower. Businesses which expanded off that excess/unsustainable spending will wither. 8. The FIRE economy (finance, insurance, real estate) will re-set to much lower historic ranges of profit and share of of the overall economy. Rather naturally, the industries which benefitted the most from the credit bubble will suffer the largest re-sets back to historic averages.

Not everything has a default setting; sectors of the economy like energy and "healthcare" have dynamics without precedent, and those dynamics will be the most politically volatile and most difficult to understand and manage. But those are topics for another day. Here's the key takeaway of "re-set": before we whine about higher taxes, higher borrowing costs, lower spending and lower asset values, let's look carefully at historic rates and ranges. What we'll find is a return/reversion to historic ranges. In the classic cognitive error of extrapolating a brief spike into a permanent trend, we have collectively extrapolated a stupendously imbalanced and unsustainable credit-bubble into "this is normal." It was not normal, or healthy, and the re-set is both inevitable and healthy.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, DemiVox Records ($25) for your very generous donation

to this site.

I am greatly honored by your support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||