|

|

|

This Week's Theme: Trends That Will Stick Even If Credit's Available, Who's Qualified to Take On More Debt? (November 17, 2008)This week's theme is "trends that will stick"--that is, trends which will not be reversing for quite some time. Why is this important? Simply put: investment and life decisions which are aligned with major trends are more likely to be successful than decisions and investments which run against the current of profound trends. One cognitive error humanity is especially prone to is assuming a short-term trend can be extrapolated into the future. In the grip of a bubble mentality, we are easy converts to notions such as "real estate only goes up," even when the historical record has demonstrably proven such an extrapolation to be false. In a similar fashion, low volatility and low interest rates were assumed to be permanent features of the "new" global financial world. Alas, it is now painfully visible that super-low interest rates and super-low volatility/risk were short-term artifacts, not semi-permanent trends. So how can we tell the difference between a short-term trend and a long one? Start with the fundamentals: supply, demand, demographics, historical averages, etc. Today's "trend that will stick": regardless of the amount of credit available, few are qualified to add to their existing debt burden. And of those who are qualified, many are allergic to debt; regardless of the blandishments offered to take on debt, they're not interested. Credit card balances, mortgages and auto loans--all are absolute anathema to this slice of citizenry. It's ironic, isn't it: Credit's Available, But Who's Qualified to Take On More Debt? Only those who don't want to borrow. Let's run a list of those who, if subjected to an old-fashioned (i.e. from 1999) prudent assessment of creditworthiness, would not qualify: 1. Most banks and lenders. Balance sheets loaded with toxic "assets," off-balance sheet toxic "assets" which if brought over to the balance sheet would immediately render the firm insolvent, "assets" which are still marked to fantasy rather than real-world realities--the list of reasons why banks themselves are poor credit risks is nearly endless. 2. Most consumers. The percentages of "debt owners" whose mortgages exceeds the value of their home is about 25% now, but this was as of September; one wonders what the number will be by next September: From Lots of homes 'underwater' on mortgages in U.S.:

Over 7.5 million mortgages or 18% of all properties with a mortgage were in a negative equity position as of the end of September 2008. There are an additional 2.1 million mortgages that are approaching negative equity. These are defined as mortgages within 5% of being in a negative equity position. Negative-equity and near-negative equity mortgages combined account for over 23% of all properties with a mortgage.Mark Zandi pegs the current number at 12 million and next year's total at 14.6 million: from Underwater mortgages inundate US:

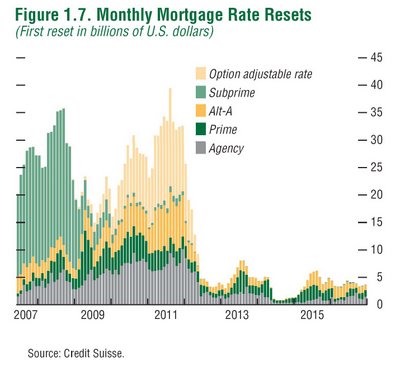

About 12 million US homeowners owed more than their homes were worth, compared with 6.6 million at the end of last year and slightly more than 3 million at the close of 2006, Mark Zandi, the chief economist at Moody's Economy.com, said this week.Even this astounding number sounds optimistic for a number of reasons. Job losses have yet to really kick in, and so the causal connection between forced sales and declining prices has yet to run its course. If 7 million people lose their jobs ( 5% of the total U.S. workforce) and about 65% own homes (the national average), then about 4.5 million may have to sell their house once their income drops and their savings (if any) are depleted. Then there's the ugly mortgage re-set chart which suggests re-sets of interest-only and adjustable-rate mortgages will continue forcing sales for years to come:

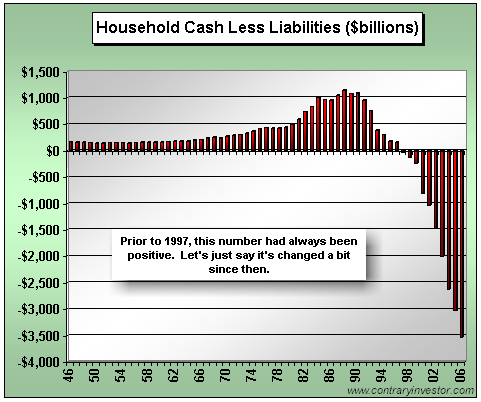

And let's not forget this sobering chart of household liabilities, which have rcoketed to unprecedented levels of indebtedness:

Most households have few other assets to fall back on. As noted here many times before, the vast majority of productive assets in the U.S. are owned by the top 5% of the populace:

Can we trust the data? Why should we? Who defines who's mortgage is "underwater" or "distressed"? All sorts of shenanigans are being pulled to keep distressed/defaulting mortgages off the "overdue" ledgers. For instance, banks have magically decreased the number of distressed mortgages by raising the trigger from 90 days overdue to 120 days overdue. Is skepticism is order that the "underwater" numbers have been massaged wherever possible to minimize the number? Yes. What evidence is there that housing is about to reverse and start appreciating in value? Basically, there is none. Basic supply and demand suggests additional steep declines lie ahead for at least the next 4-5 years. HELOCs? Toast. Equity extraction via refinancing? Toast. How many homeowners still have equity in excess of 20%? How many will still have equity in excess of 20% next year, or in 2010 or 2011? Since the transaction costs of selling a house are about 7% of the sales price, then even 10% equity is in practical terms about 3% net equity after escrow closing, and 20% is really only 13%. Not much to hang your hat on in terms of assets you can borrow against. And what lender is willing to bet your 30% equity today won't shrink to 20% by next year? That's a risky bet in anyone's book. Here's the reality: Our economy is awash in debt: mortgages, credit cards, auto loans, home equity lines of credit, you name it. This chart says it all:

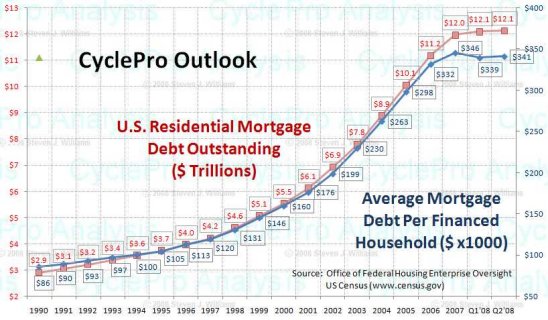

That is a trend which is not going to be reversed next month or next year. Simply put, this depicts an economy burdened with crushing debts that will either have to be written off as uncollectable (otherwise known as losses), severely depreciated (sold for 10 cents on the dollar, etc.) or paid down slowly out of earnings. None are rapid processes which can magically be reversed. Holders of distressed assets will resist taking writedowns with every fiber of their beings, and consumers saddled with astounding debts will have to work through a painfully long bankruptcy process before being freed to borrow stupendous sums of money again. The debt wagon lost a wheel, folks, and the mule ran off. You can try pulling the load yourself, but the slope gets mighty steep up ahead. Just look at the tremendous rise in the nation's total mortgage burden:

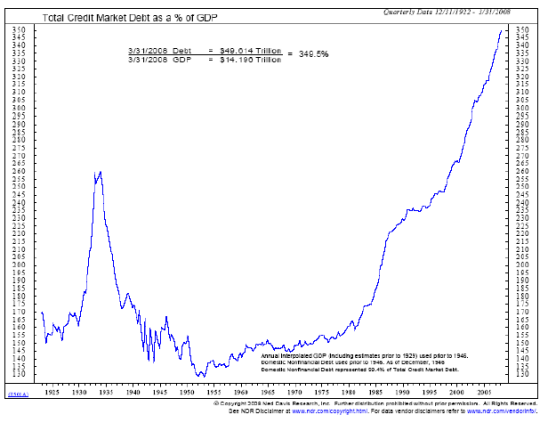

3. Corporations and commercial real estate. If you're wondering why the stock of once-mighty corporations like General Electric has been crushed recently, look no further than their debt load and/or exposure to rapidly depreciating debt of all flavors. Think anyone wants to lend big bucks to develop another empty mall or office tower? Here's a "big picture" snapshot of our economy's debt in relation to our GDP:

Adjectives such as "unprecedented" don't quite do this chart justice. Clearly, an enormous amount of this debt will have to be repudiated/written down or written off, and a large percentage of corporate and consumer income will be allotted to pay down debt for years to come. 4. Nations. By any prudent underwriting standards, entire nations are increasingly as risk of defaulting on their sovereign debt. So go ahead and crank out trillions of dollars in new Treasury debt, Ben and Hank, and then pump hundreds of billions into the lending machine: by prudent underwriting standards, few who are willing to borrow are qualified to borrow. And many of those few who are qualified have zero interest (bad pun intended) in taking on debt.

That's a trend that will stick for years to come.

David W.

Let me tell you a story. About 8 or 9 years ago, when I lived in Manhattan's Upper East Side, I was waiting for the subway and there was a man playing the violin in the station. The music was BEAUTIFUL, especially with the acoustics of the subway station and tunnel, until the subway came, of course. It really made my morning. But, the Upper East Side stations being what they were, very hot and very crowded and uncomfortable, I didn't want to stay there one extra millisecond, so I got on the 1st train that arrived. John K.

I enjoyed that post and the very good responses to the Bell experiment post, especially Erics response. I dont like classical music either. It just doesnt affect me in the way it should, I guess. Id be more apt to stop and watch an alternative rock/pop band like Cake or Cracker or any band with a more upbeat sound. I dont think its an elitist/non-elitist thing. However, I do doubt your premise that the masses back in the 1700s all liked what we now call classical music. I very much doubt it was ever popular in the way rock n roll is now, or perhaps some kind of folk was back then. Classical had the benefit that it was written down. Other music in the same era likely wasnt written down, or if it was, wasnt reproduced as effectively for whatever reasons. Im certainly no historian, but Im pretty sure that varieties of folk (Celtic, etc) were far more popular and more likely to draw a crowd away from their everyday worries and tedious jobs than was classical. Classical isnt music geared to be listened to on ones hectic commute. It takes a more pensive environment to appreciate. Not a subway. Ruthann

An invigorating topic, the Bell experiment. My mind was "spirited away" by Eric's response and your re-response; both absolutely brilliant. You each played notes, chords, yes even a few measures of familiar music; as well as inspiring this composition. Bill Murath

I went to the Denver Symphony last week on a school field trip. This was the 5th time, since my kids play the violin. This one just melted my mind. They featured Gustav Holst's the Planets. The movements were other worldly. It was actually the day you put up the piece about how blinded we are to beauty. I came away with such a postive outlook on the human race. It doesn't matter if we nuke most of ourselves to kingdom come. The finest achievements in all of mankind's history are the instruments created during the Middle Ages. Since these were built with hand tools I see hope eternal. To me the Violin and Piano are much greater accomplishments of man than a rocket, Ipod or cell phone. The only thing that comes close is a surfboard :-) Chris S.

Eric A wrote: "I live in spaces designed by soulless theory and not visceral joy, and every day I interact with the frightened and shell-shocked, who have each chained up their childish joy in a hidden closet for their own protectionwhich is simply to say, I'm your average American." Additional reader commentaries on Joshua Bell plays the subway: Readers Respond to "Bell Plays the Subway".

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Evelyn L. ($75) for your astonishingly generous

donation to this site.

I am greatly honored by your support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||