|

|

|

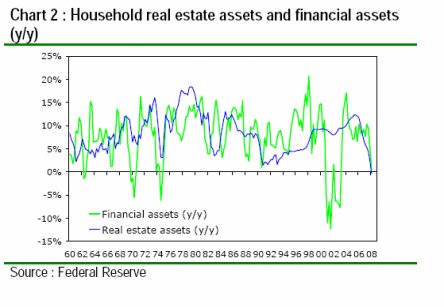

Why Housing Is Far from Bottoming: Depression, Demographics, Defaults and Dumps (October 8, 2008) The thesis stated again and again in the mainstream media (MSM) is that the U.S. economy can't get back on its feet until housing "recovers"--which makes the question "when will housing recover?" of paramount importance. The reasoning is simple: for the vast majority of middle-class households, the equity in their residence represents a major chunk of their wealth. When housing was skyrocketing in value, homeowners felt wealthier and thus they spent freely, even if they doidn't extract the equity via HELOCs (home equity line of credit). That's called the "wealth effect." Now we have the "reverse wealth effect." As equity has declined--in millions of cases, to negative net worth--homeowners feel poorer and thus they are spending less. Since equity extraction, which once flooded the economy with hundreds of billions of "free money" year after year, has now shrunk to near-zero, they also have less money to spend. As we can see in the chart, household real estate wealth is set to decline for the first time in 50 years. Financial wealth is also set to go negative, an unprecedented (in post-WW2 era) double-whammy to household wealth.

Construction, remodeling, home furnishings, real estate financing and sales together make up a big percentage of the U.S. economy. As each of these components shrinks, the toll on the U.S. is huge. OK, so isn't housing set to "rebound" next year, or in 2010 at the latest? No. For as correspondent Pangolin notes, while mortgages may just be paper, the paper is based on real physical houses and neighborhoods. the "paper losses" are hitting the real houses and neighborhoods hard in four ways: Depression, Demographics, Defaults and Dumps. Here are Pangolin's incisive comments:

Is it me or we all ignoring a fifth elephant in the financial living room? All of this debt is secured by assets, houses, on land, that were built with the presumption that well-employed people would live in them at about the ratio of 2.6 people per 2500 sq. feet. (sources: U.S. Census 2006, Square Footage Measurements and Comparisons Energy Information Administration)Thank you, Pangolin, for raising/addressing profound trends. I have previously addressed the demographics of U.S. housing, following the same line Pangolin traces: Housing's Headwinds: Demographics, Rising Rates, Peak Oil and Oversupply (July 23, 2008). What we have right now: Depression (falling employment and household wealth), Demographics (falling number of households), and Defaults (foreclosures, walk-aways, etc.) reflected in the following: 1. massive oversupply of housing 2. falling "residents per household" in the U.S. is reversing 3. a tidal wave of housing-mortgage-related lawsuits which is already threatening to swamp U.S. courts Let's start by recalling that there are 18.6 million vacant homes in the U.S.--a staggeringly large number. Here is the Census report: CENSUS BUREAU REPORTS ON RESIDENTIAL VACANCIES AND HOMEOWNERSHIP

There were an estimated 129.4 million housing units in the United States in the first quarter 2008. Approximately 110.8 million housing units were occupied: 75.1 million by owners and 35.7 million by renters.There are a number of interesting facts presented here. Only 4.7 million of the vacant dwellings were "seasonal," i.e. second-homes/cabins; 14 million homes are available right now for occupancy. A million new units sit empty, and only 20% are for sale. We can presume the builders/developers/lenders are hanging on to the other 800,000 empty new homes, hoping and praying that some miraculous turn-around in the housing market will enable them to sell a million vacant homes in the near future. Even as the "downturn" worsens, over a million new dwellings will be constructed and added to the inventory this year. So let's just round up and say there are (or soon will be) 20 million vacant residences in the U.S. With an average household size of about 2.6 people, we have room for 50 million more citizens without building a single additional home. If we subtract the 5 million vacation homes, that leaves 15 million vacant dwellings, and I think it is safe to say that is a massive oversupply of housing. Household size has been dropping for 100 years: Census: U.S. household size shrinking Wealth, looser social restrictions contributing to trend, experts say. But as the "wealth effect" reverses, this trend is reversing, too. How many elderly and not-so-elderly people live alone in a big house? A lot. How many couples bounce around a big house, now that the offspring have left? Take the humongous national wealth reduction we are just starting to experience and add in 60 million retiring Baby Boomers, and what do you get? It seems to me you get a lot of reasons for household size to increase. Kids move back home, creaky retirees open up the house for a live-in assistant, and unable-to-retire folks start renting out all those empty rooms for extra income. And if household size even edges up slightly, that will greatly reduce the number of dwellings the nation needs for actually housing people as opposed to investment/gambling schemes. An increase in household size would radically increase inventory of unwanted/unsold/unrented dwellings. Last but not least, let's ponder the consequences of lawsuits: against the builders of shoddy/defective homes, against fraudulent lenders, predatory lenders, investment banks which packaged high-risk mortgages and sold then as low-risk "investments," and on and on. When tottering builders are pushed into liquidation by lawsuits, their inventory (those 800,000 empty new homes) will not be allowed to sit around waiting for better times; they will be auctioned off and the proceeds given to the bondholders and lienholders. What happens to a shaky market when hundreds of thousands of houses get auctioned off, no-minimum bid? It drops. What happens when insolvent lenders who have been hoarding and hiding hundreds of thousands of foreclosed/distressed properties are finally forced into liquidation? All those distressed properties get sold off, too. More inventory, more auctions, and prices which will be dropping to near-zero in many markets. Pangolin points to a number of serious downsides to the last trend: Dumps, as in abandoned/vacant dwellings. Nothing saps value as quickly as eyesores appearing in a neighborhood. Invoking (as we so often do) the Pareto Principle (a.k.a. the 80/20 rule), we can anticipate that when a mere 4% of the homes in an area are vandalized/stripped/occupied by undesirables, then 64% of the homes' values will be negatively affected. And should the number of abandoned residences hit the threshold of 20%, then we can anticipate a severe decline in the values of fully 80% of all housing in the vicinity. This also works within highrise condos, as once 20% of the units are not just vacant but essentially unowned, then the common-area expenses will rise for the remaining 80% of the owners. As Pangolin insightfully observes, we can anticipate a rising political furor as homeowners demand that government "do something." Local government's typical response is a toothless "warning" to owners of abandoned properties to maintain the dwelling. But recently, some cities have taken a much tougher stand, especially against bank-owned foreclosed homes (so called REOs, 'real estate owned'). Empty Homes Spur Cities' Suits (law.com)

Cities now dealing with scores of abandoned, foreclosed homes have started suing banks and mortgage companies to recoup their costs, while other cities are hauling lenders before code enforcement boards and county courts to force them to maintain abandoned properties.Thanks to HADD - Homeowners Against Deficient Dwellings, we can also track the many legal actions being taken again builders of shoddy/deficient new dwellings. Just as cities are under increasing pressure to address vacant/vandalized housing, their property tax revenues are plummeting along with valuations. This puts cities which are trying to "do the right thing" on the horns of a dilemma: enforcement and lawsuits cost money, just as revenues are dropping. Do you reckon cities will be fighting tooth and nail for banks and lenders to pay "their fair share"? As lenders go through various shotgun marriages, the lawsuits will simply shift from WAMU (Washington Mutual) to JP Morgan, just as the suits against Countrywide shifted to Bank of America, which just reached an $8 billion settlement with various municipalities and government agencies. Those Bulls who are salivating over all those fat future profits flowing to banks might want to reconsider their faith in future profits. No one can know how much money will be bled from banks by lawsuits of every type and size, but we can anticipate the amounts will be huge and the filings will fly for years to come. The law is also politically influenced. As public rage builds, juries and judges will not be immune; we can anticipate the surviving banks being hit with staggering punitive judgments. One issue which is virtually ignored by the MSM: how much will it cost the surviving banks to maintain and pay the property taxes on these millions of foreclosed properties? As if tightening credit and systemic distrust/opacity weren't bad enough, now the surviving banks are being saddled (and rightly so) with enormous carrying costs. So what happens to these millions of empty, vandalized, unmaintained or stripped dwellings? Pangolin suggests that political pressure from remaining homeowners will power a "use it or lose it" movement in which eminent domain will be wielded by local authorities to acquire homes and then auction them off with the caveat that the buyer must occupy the residence. Another possibility is that the Federal government, via its Fannie Mae and Freddie Mac divisions, will become a massive owner-of-last-resort of U.S. real estate. Frequent contributor Harun I. recently sent in a link to an account of Home Owners' Loan Corporation (Wikipedia), a New Deal agency established in 1933 to refinance homes to prevent foreclosure. Harun's comment: "The HOLC did not prevent the Great Depression even though it was created as early as 1933." A telling point; and I would add that the agency didn't finish its mandated business until 1951: fully 18 years after it was formed to "resolve the crisis. If history is any guide at all, we can thus anticipate all these "rescue" operations currently being thrown into place lasting until 2026. Here is another take on the HOLC from the Washington Post of 3/14/08: A 1930s Loan Rescue Lesson:

Today's economic situation, while serious, is minor compared with the financial collapse of 1933. That year, about half of mortgage debt was in default. On Dec. 31, 2007, serious delinquencies in the United States were 3.62 percent of all mortgages. In 1933, the unemployment rate had reached about 25 percent (compared with 4.8 percent today). Thousands of banks and savings and loans had failed. The amount of annual mortgage lending had dropped about 80 percent, as had private residential construction. States were enacting moratoriums on foreclosures. The average borrower that the HOLC eventually refinanced was two years' delinquent on the original mortgage and about three years behind on property taxes.Since that article was written a few months ago, unemployment has shot to 6% and the number of foreclosures has increased. How high unemployment and foreclosures will rise is unknown, but the trend is definitely up for both--way up. Fannie and Freddie already own about half of all residential mortgages in the country. (Roughly $5 trillion of the total $10 trillion in residential mortgages.) It's not too difficult to foresee the Federal government owning outright (and thus playing landlord/auctioneer for) hundreds of thousands, if not millions, of residences. We may yet become a nation of renters again, as we were in the Great Depression, when home ownership was around 44% compared to today's 64%.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, David L. ($30), for your extremely generous donation

to this site.

I am greatly honored by your ongoing support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||