|

|

|

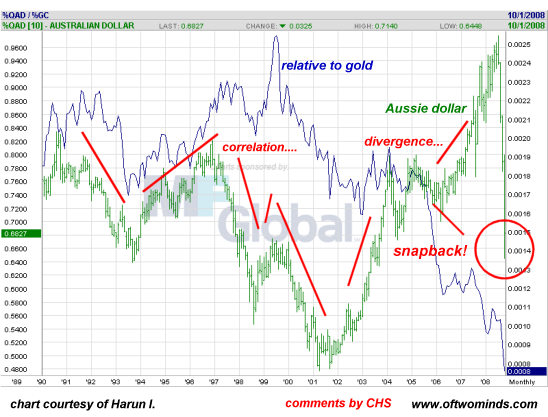

Snapback! (October 9, 2008) Frequent contributor Harun I. recently introduced me to a concept he terms "snapback": the sharp, sudden reversal of divergences or unsustainable markets back to historic correlations. (SInce Harun coined this phrase, I hope he gets credit in all future references.) Why is this something worth pondering? Many smart, experienced market commentators are now suggesting that the "bottom" in the stock market is close at hand, citing various extremes in valuation and sentiment. Yes, the usual indicators (oversold, etc.) can be interpreted to support the notion that the markets are near a bottom--if these were typical times. But these are not typical times. There are a number of correlations between various markets, and Harun provided the Australian dollar as an example.

Notice how the Aussie dollar maintained a correlation of trend relative to gold until 2006, when the currency rose sharply and its value relative to gold moved in the opposite direction, i.e. declined. The sudden re-convergence to historic correlations is "snapback". Harun provided another potential setup for "snapback": the Yankee dollar and its correlation to its relative value in gold. The two have risen and fallen in near-perfect unison for years. Now we see the dollar has moved up sharply as its relative value to gold has stayed flat. Harun's comment: "This bounce in nominal price (i.e. the dollar) has not been followed by real value (gold). Should they stay divergent, the rally in the USD will wane."

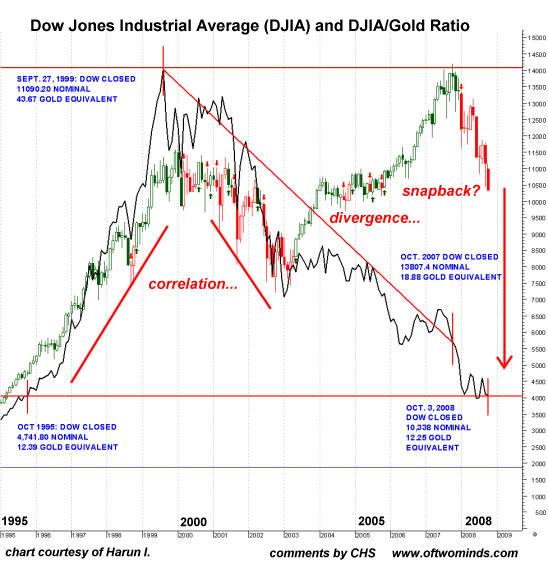

If markets are due for a "snapback" then the bottom could be farther away than most suspect possible. For instance: by at least one measure, the ratio of the Dow Jones Industrial Average (DJIA) to gold, the Dow Jones Industrial Average's historical "snapback" would take it to around 5,500-- fully 4,000 points below the "bottom" so many are seeing in the present. A decline to even 4,000 is certainly possible if you gaze at this chart:

Harun also made these comments about yesterday's entry:

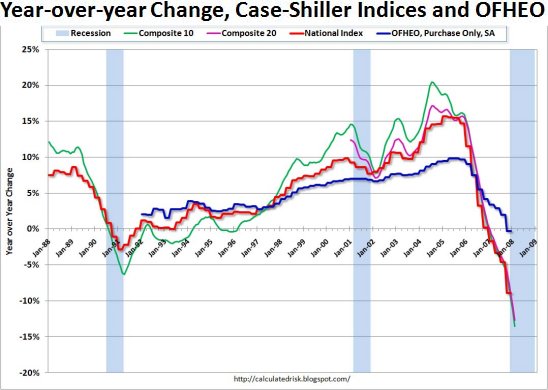

"The thesis stated again and again in the mainstream media (MSM) is that the U.S. economy can't get back on its feet until housing "recovers"--which makes the question "when will housing recover?" of paramount importance." (From Why Housing Is Far from Bottoming: Depression, Demographics, Defaults and Dumps (Part III) (October 8, 2008)So how does Harun's analysis of the systemic problems relate to "snapback"? Just this: perhaps the system of massively leveraged credit is about to "snapback" to much lower levels, effectively eviscerating the global economy and all asset values other than gold. Here's an example of "snapback": housing prices falling rapidly toward a historical correlation to rent and income. Note the drop is not even halfway finished; prices will have to return to pre-bubble levels. As the global economy tumbles into the abyss of Depression, then incomes will fall and credit costs will rise, precipitating a fruther decline in housing as it maintains its correlations to incomes and mortgage rates/availability.

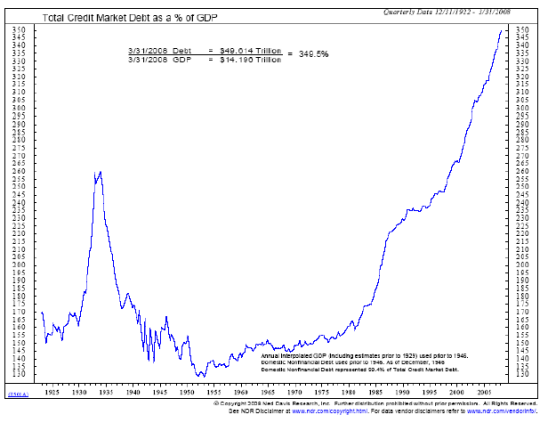

And here we have an extreme of leveraged credit which appears to be a surefire candidate for "snapback":

As correspondent/contributor Riley T. recently pointed out, this is a ratio of credit and GDP; thus the sharp peak in the Great Depression reflects not credit expansion but GDP contraction. Thus even as leveraged credit contracts with ferocious force in our current economy, this ratio may stay high as the GDP will be contracting with equal ferocity. So how does all this connect to this week's theme: how long will the Depression last? Here's how: this ratio of credit to GDP has to drop all the way back down to historic correlations. Put another way: credit will have to fall even faster and farther than GDP. Since our entire "consumer economy" is based on cheap, easy credit, the contraction of credit will cause a massive contraction in GDP, thus strengthening the contractions in a feedback loop. How long will it take to rebuild savings and capital, i.e. wean ourselves from a leveraged-credit dependency? A long time; and even longer if we follow Japan's path and try to sweep the insolvency of the system under the carpet and act like everything's just peachy. That will guarantee decades of stagnation and Depression.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Tom S. ($50), for your outrageously steadfast

and outrageously generous donations

to this site.

I am greatly honored by your support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||