|

|

|

America's Financial Joyride (September 4, 2008) We all know what a joyride is--some irresponsible teenagers pile into a car and drive it with carefree zest until the gas runs out--then they abandon it on the roadside. The U.S. economy's joyride is ending.

Who piled into the debt-fueled car for the wild spin? Let's see:

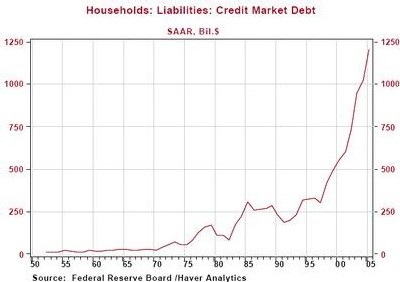

Did anyone checks the brakes on the debt-mobile? Nope. Did anyone ask how much gas was in the tank, or where it came from? Nope. Did anyone ask how the next tank of debt-fuel would be paid? Nope. So what exactly is the difference between a bunch of irresponsible adolescents and those in charge of the world's largest economy? Nothing, except the "leaders" have done trillions of dollars worth of damage during their joyride. Now that the ride is over and the U.S. economy is laying upside down in a ditch, then guess who gets the call to "rescue" the dumb, foolish adolescents, oops I mean "leaders" and banks? The U.S. taxpayer, presuming a few are still making enough money to pay taxes. And if we can't nail taxpayers, hey, we'll just borrow another couple trillion from our foreign "friends." They never seem to run out money or the willingness to loan trillions more to us for pathetic returns and a high risk of default. Is this what is called "financial rationalism"? That if someone is dumb enough to loan you unimaginably large sums, no questions asked, for absurdly low rates of return, then why not just take the money and run? That's what any adolescent would do, of course. But once you enter adulthood, then you're supposed to develop maturity and judgment. Too bad the U.S. is a nation of adolescents. Don't make me exercise, I hate it, Just pay for my new hips, knees, heart valves, etc. Don't tell me junk food is bad for me, I can do what I want. Don't tell me I have to save up to buy a house, I want it right now and I hate saving. Don't tell me my house isn't my retirement, I want it to be my retirement so I don't have to put off buying everything I want, right now! (Cue teenage tantrum.) Lest you think I exaggerate: consider Exhibit One:

Exhibit Two:

Exhibit Three:

Think "the worst is over? Ha. Check Exhibit Four:

Astute reader I.M. recently posed the critical question thusly:

Since you're on the subject of national fiscal psychology this week, do you have thoughts about why it is that we as a nation can convince ourselves that our situation is not as dire as it really is? The official debt is more than $50K per worker. The unofficial debt including future social welfare outlays is much higher, perhaps closing in on half a million per worker. How can we as a society continue to think that our current situation is sustainable?Maybe our debts have finally reached the critical mass of instability/insolvency. Knowledgeable correspondent C.V. sent in this article which describes how the illiquidity and losses in "agency paper" i.e. Fannie Mae and Freddie Mac, are infecting foreign bankers' ability to raise dollars to "adjust" their own currencies: South Korea heads for black September with won problems American investments threaten currency

The deepening woes at Fannie Mae and Freddie Mac, badly stretched central bank reserves and a losing battle to support the won are pushing South Korea towards a full-blown currency crisis this month, analysts have said.C.V. added this comment, which has mind-boggling potential repercussions:

Maybe we're seeing a 'flight' to the US$ right now. The fannies and freddies will gain value when converted back to the host currencies, or even sell them back to the US Treasury at fire sale prices in a bailout. The Fed will buy any and all Treasuries if necessary which is commonly referred to as "monetizing the debt" which is what foreign CBs (central banks) have done by issuing their own currencies (inflationary) by buying Treasuries in the first place.In essence (as I understand it), as foreign central banks try to sell non-Treasury securities to raise dollars, then they will be forced to sell Fannie Mae and other agency paper back to the U.S. Treasury at whatever rate the Treasury deems "fair." If central banks start dumping their vast hordes of U.S. Treasuries, then the Treasury will buy all of that, too. But where will the Treasury get all the money to buy all this debt? What effect will that have the dollar's value? I don't have an answer, but I do know the charts posted above have already sealed the fate of the U.S. economy. Plummeting housing values means the money spigot of borrowed money based on real estate assets is closed for good. And with that spigot closed, and with consumer and government debt already at unprededented levels, consumer spending--69% of the economy-- is shriveling, and will continue to shrivel in a self-reinforcing feedback loop of lower asset values, less borrowing, less spending, less profits and fewer jobs--which all lead to lower spending. The joyride's over, folks; unfortunately, the car is a total loss. Maybe "the kids" learned something. Too bad it will take a generation to repair the damage done by the 1996-2006 joyride. Thank you, C.N.F., for suggesting the excellent analogy of a joyride.

Readers' comments: Chuck D.

Just a comment on part of your entry for today. You wrote:Michael S.

"As I see it, the benefit that we get by operating in a fiat money world (where central banks and fractional reserve banking allows financiers to create money out of thin air) is that we get a rapidly expanding economy, so that in the span of a human lifetime, we see 'progress.'" Mark P.

To add to your example of real time monitoring of the cost of driving, how about taxes? If people had to write a check four (or more) times a year rather than having taxes deducted automatically, I expect we all, regardless of political beliefs, would be clamoring for greater spending control and efficiency.

New Book Notes: My new "little book of big ideas," Weblogs & New Media: Marketing in Crisis

"Charles Hugh Smith's Weblogs & New Media: Marketing in Crisis is one of the most important business analyses I have ever read. It is the first to squarely face converging global crises from a business perspective: peak oil, climate change, resource depletion, and the junction of key social cycles will radically alter the business landscape in coming decades...." An excerpt from For My Daughter

I believe she stayed with me out of kindness, and my admiration for her grew. For kindness is everything piety is not; where piety is all appearance, a brittle play-acting well-loved by treachery, kindness is spontaneous and true. Piety is easily falsified, so evil never tires of exalting it, while kindness cannot be feigned, and so evil rejects it. Piety serves self-pride, while kindness serves another.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Ian M. ($10), for your surprising and gratifying donation

to this site.

I am greatly honored by your support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||