|

|

|

|||||||||||||

|

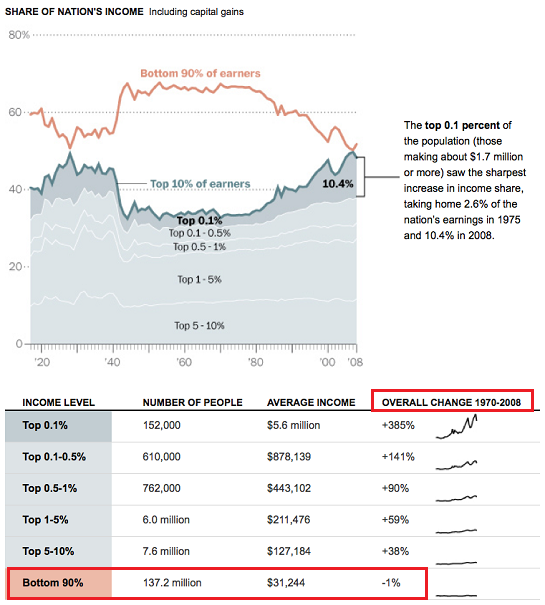

The Global Economy: It's All About Increasing Leverage (July 10, 2012) If the global State/finance Empire can't increase systemic leverage, it will implode. If we look at the global economy with unclouded eyes, we reach this conclusion: "This whole thing is about leverage." If leverage doesn't increase, the system implodes. But since collateral is disappearing from the global economy like sand castles in a rising tide, and disposable income has stagnated, there is no foundation for more leverage. As a result, the State/finance cartel has only one choice: increase leverage by whatever means are left. There are only two: 1. Allow banks to claim phantom assets as capital/reserves 2. Lower interest rates so stagnant income can leverage ever greater quantities of debt The State/finance Empire and its army of academic toadies (economists) must cloak this reliance on leverage from the citizenry, lest they grasp the precariousness of the entire financial system. As the economic Establishment is discredited by reality (that their sputtering reflation policies have come at an unbearable cost is now undeniable), their attempts to discredit their critics become increasingly comic: only PhD economists in the employ of the Empire are qualified to comment on the Empire's policies, etc. Most discussions of leverage focus on the role of capital or reserves as the basis for leverage. This is the basis of the fractional reserve banking system: $1 in capital (cash, reserves) can be leveraged into $15 of debt. The easiest way to "grow" is to increase leverage so more money/debt can be created. If a bank was constrained to only loaning the cash it held in deposits, that would severely limit the amount of money available in the system for purchasing villas in Spain, BMW autos manufactured in Germany, etc. If we magically enable 25-to-1 leverage, then every euro supports 25 euros in debt (mortgages, auto loans, etc.) The danger is obvious: if 1 of the 25 euros of debt goes bad, the lender has zero reserve. If 2 euros of debt go bad, the lender is insolvent. The only way to "save" an over-leveraged system is to increase leverage and lower interest rates. If we claim phantom assets as real and increase leverage from 25-to-1 to 50-to-1, we have enabled a doubling of loans. All that wonderful new money will flow into the economy as spending, fueling "growth." This explains why the State/finance Empire in Europe keeps lowering reserve requirements for its insolvent banks. If the reserve requirement is 10%, then you need 100 million euros on deposit in cash to support 1 billion euros in loans. If you lower the reserve requirement to 1 euro, then the contents of a child's piggy bank supports 1 billion euros in debt. The other game is to claim phantom assets have market values that justify their substitution of cash. Let's say a bank owns a villa in Spain since the mortgage went bust. The market value of the villa is 100,000 euros and the bank's mortgage was 300,000 euros. If the bank sold the villa, it would have to absorb a 200,000 euro loss. Yikes. Absorbing losses that exceed the net increase in reserves from profits would lead to the lender's insolvency being recognized. The "work-around" is to keep the villa on the books at 500,000 euros. Not only does the 200,000 euro loss go away, the bank now has 200,000 in capital to leverage into more debt. (500,000 in assets minus 300,000 in mortgage leaves 200,000 in phantom assets/capital.) Any loan is fundamentally a claim on future income. Interest and principal will be paid out of future income. The key to keeping the leverage-based system afloat is to lower interest rates. Let's say a household has $10,000 in disposable income to spend on housing. If mortgage interest rates are 15% (as they were in 1981), the household can only leverage that income into a $50,000 mortgage. That's all the debt that can be prudently leveraged from the $10,000 in income. That inhibits "growth," so let's drop the rate to 1%. Presto-magico, the household now "qualifies" for a $500,000 mortgage. Wasn't that easy? You see the problem here: once rates fall to near-zero, the leverage-income-into-more-debt machine runs off the cliff. Just in case you missed this chart from yesterday's entry Election Year 2012: two Landslides in the Making?, notice that the incomes of 90% of American households has gone nowhere for the past 40 years.

Unsurprisingly, the bottom 90% leveraged their stagnant incomes into mountains of debt to compensate for their declining purchasing power. The Federal Reserve (a key player in the global State/finance Empire) has been publicly fretting over the dreaded "debt divide," which is Orwellian econo-speak for the bottom 90% running out of leverage. Like Wiley E. Coyote, the bottom 90% has run off the cliff and is now in looking down at the air beneath them. (This chart shows the bottom 95% is in trouble.)

The same reliance on leverage has occurred in China, Japan, Europe and the U.S. The entire global economy's "growth" was based on increasing leverage. That machine has soared off the cliff, and now the Empire's global army of toadies is desperately attempting to mask this reality by substituting phantom assets for actual capital. They can't do anything about lowering interest rates, though; that mechanism has already been maxed out as rates approach zero. Longtime correspondent Harun I. recently described the leverage endgame in this deeply insightful commentary:

Much has been made over the Fed's efforts to "stimulate", however, IMHO the Fed's efforts are more concerned with preventing the sudden death of the monetary and banking systems. With private sector balance sheets hobbled, some entity must step in and create enough debt so that debts can be paid and, therefore, maintain the illusion that there is money (debt) in the system. At first this must seem contradictory. Remember there is no collateral, there is no asset. Therefore, the debt, which people will claim as an asset (at par (to what?)), is in reality an illusion.

Thank you, Harun. After four long years of protecting vested interests at the

expense of everyone else and playing "stimulus and backstop" games,

the State/finance Empire's Wily E. Coyote moment is finally approaching. Maybe they manage

a few more extend-and-pretend mind-tricks (because we all want to believe the magic trick

is real) and push the reckoning into 2013; we'll just have to see how long Wiley E.

Coyote can run in mid-air.

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

Resistance, Revolution, Liberation: A Model for Positive Change

(print $25)

(Kindle eBook $9.95) Read the Introduction (2,600 words) and Chapter One (7,600 words) for free.

We are like passengers on the Titanic ten minutes after its fatal encounter with the iceberg: though our financial system seems unsinkable, its reliance on debt and financialization has already doomed it.

If this recession strikes you as different from previous downturns, you might

be interested in my book

An Unconventional Guide to Investing in Troubled Times (print edition)

or

Kindle ebook format. You can read the ebook on any

computer, smart phone, iPad, etc. Click here for links to Kindle apps and Chapter One.

The solution in one word: Localism.

Of Two Minds Kindle edition: Of Two Minds blog-Kindle

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: gifts/contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Subscribers ($5/mo) and contributors of $50 or more this year will receive a weekly email of exclusive (though not necessarily coherent) musings and amusings. At readers' request, there is also a $10/month option. The "unsubscribe" link is for when you find the usual drivel here insufferable.

All content, HTML coding, format design, design elements and images copyright © 2012 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this essay to your site, or printed a copy for your own use.

Terms of Service:

|

Add oftwominds.com to your reader:

My Big Island Girl

Instrumentals by my friend

|

| Survival+ | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||