|

|

|

The Coming Destruction of U.S. Bonds (October 3, 2008) In the fantasy-world of market cheerleaders and "experts", interest rates will remain low indefinitely because the Fed will lower the Fed fund rate to near-zero. Nice, but the Fed doesn't control interest rates--the bond market does, and the bond market is set to reverse course, destroying the value of all existing bonds. Many observers, myself included, have long contended that all three asset classes--stocks, bonds and real estate--having risen in unison in the phony credit-bubble "prosperity" of the past decade, will also fall in unison. The housing bust has started--yes, only started--deflating the bubble-era valuations of both residential and commercial real estate, and global stock markets have already witnessed declines of between 20% and 65%. They are far from bottoming, too. Here is a chart which illustrates analyst Louise Yamada's view that the market is poised for a 50% decline along the lines of 1937's "echo bubble" collapse:

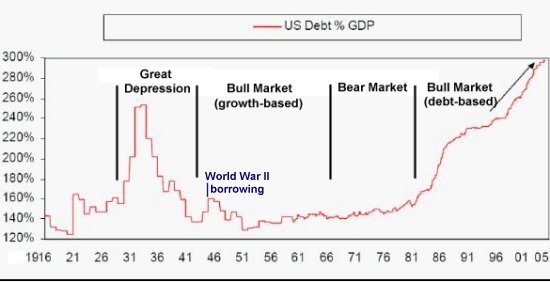

It will soon be bonds' turn to decline rapidly in value. Correspondents Craig M. and U. Doran have recommended the always-worthy Jesse's Cafe Americain's entry, The Mother Bubble: The US Long Bond. The charts reveal a 25-year long Bull market in bonds which appears to have double-topped: a sure indication that the top is in. To provide context for the coming destruction of bond values, here is a chart which illustrates the vast indebtedness of the U.S. economy:

In other words, even before this insane $850 billion bailout (counting the $800 billion the Fed has already thrown down other ratholes, it's more like $1.6 trillion and counting) we were already up to our eyeballs in debt. To refresh our memories of how bonds valuations work: picture a see-saw. When rates fall, a bond's price increases. When rates rise, a bond's price decreases. For example: if a $100 30-year bond has a yield of 5%, then if rates fall to 2.5% the market value of the bond will almost double to around $200 because the effective yield of the bond at $200 is 2.5%. That is basically what has happened since the bond yield topped in 1981: face values of all bonds has been rising as yields have fallen from 16% to 3%. If rates doubled from 5% to 10%, then the price of the bond would fall in half to $50, rendering the effective yield 10%. At the risk of boring longtime readers, here is my oft-published chart of the U.S. bond yield and the staggering rise in Chinese ownership of U.S. debt:

What this chart illustrates is that the only reason interest rates haven't skyrocketed along with rising U.S. debt is that China and other non-U.S. players with hundreds of billions of trade-surplus dollars have been soaking up that debt (bonds) with their dollars. This can be seen as manipulation for the benefit of oil exporters and Asian exporters equally anxious to prop up American consumers with low interest rates, or as intervention to keep their currencies lower than the dollar, or as a combination of manipulation/intervention and "safe haven" parking of stupendous hordes of dollars. Regardless of the perspective, one thing is clear: as soon as that foreign buying declines, U.S. interest rates will start rising. What could cause foreign entities to cut back on their purchases of U.S. debt? How about their flood of dollars suddenly drying up? As noted in Henry Paulson's recent essay in Foreign Affairs, The Right Way to Engage China, China has until recently generated astonishing surpluses of 11% of their entire GDP. Though I consider Mr. Paulson's bailout of Crony Capitalism unconscionable (including our Chinese "friends" in the circle of cronies to be saved was key), he does have a keen understanding of the dysfunctional c0-dependency of China and the U.S. and a remarkably objective view of China's challenges, strengths and weaknesses:

One of the most notable indications of China's imbalanced growth is its large current account surplus, which last year amounted to over 11 percent of the country's GDP. This reflects the fact that China spends much less than it produces and earns and that it has a high rate of national saving. Chinese household consumption was only 35 percent of GDP in 2007, down from roughly 50 percent 30 years ago, when Beijing started market reforms. (Household consumption is roughly 70 percent of GDP in the United States and 60 percent in India.)Here are the key take-aways: China has generated astounding surpluses of dollars via huge trade surpluses with the U.S., and very soon China will need to start investing whatever surpluses remain after a global Depression has gutted their exports in their own nation. (If you'd like some context for considering China's dilemmas, please read my 2005 report, China: An Interim Report: Its Economy, Ecology and Future . You can also scan dozens of entries on China in the archives links in the left column.) A few years ago I engaged in online debates with various smart people who were adamant that China had "decoupled" from the U.S. and would prosper on domestic demand/growth alone. Unfortunately, their case is about to be proven catastrophically incorrect. As Hank noted in his article (excerpt above), the Chinese people are keenly aware of their financial insecurity and therefore they are saving rather than spending; the domestic consumption share of their GDP has actually dropped. That basically removes the key prop in the "decoupling" position. As U.S. demand for Chinese exports plummets (along with demand for all exports and indeed, all goods), the primary driver of China's surplus--$250 billion trade surpluses with the U.S.-- will shrink rapidly. Simply put: China will no longer have the luxury of huge surpluses of dollars. It is astonishing how otherwise intelligent analysts make the basically unsound assumption that China will always have hundreds of billions of surplus dollars to park in U.S. debt. The global Depression will cut so deeply into Chinese manufacturing that China may well sink into a current-account (trade) deficit. In any event, China is already feeling growing domestic pressure to start spending its surpluses on domestic needs rather than on a now-hopeless propping up of U.S. consumer spending. The Chinese dilemma is this: if we stop propping up U.S. consumers via buying bonds to keep their interest rates low, then we risk losing half of our export economy. But if we keep pouring much of our surpluses into U.S. debt, if either the bonds or the dollar implode then we lose hundreds of billions of dollars.

From the Wall Street Journal:

Financial Troubles Humble U.S.

Frequent contributor Michael Goodfellow pinpointed an apt analogy to China's dilemma via a recent film:

From the WSJ article above:Thank you, Michael. So the endgame is already visible: either way, China loses big. Even if the central bankers wanted to keep propping up U.S. bonds, they will very soon find their gusher of export-generated dollars has dried to a trickle. The other prop under the U.S. debt market has been Saudi Arabia and the other Oil Exporters. As oil plummets to half its recent price, they too will find their gusher of dollars has suddenly gone dry. For quite some time I have contended that a global Depression would cause demand for oil to drop so severely that Peak Oil's influence over oil prices would temporarily by cut in a "head fake":

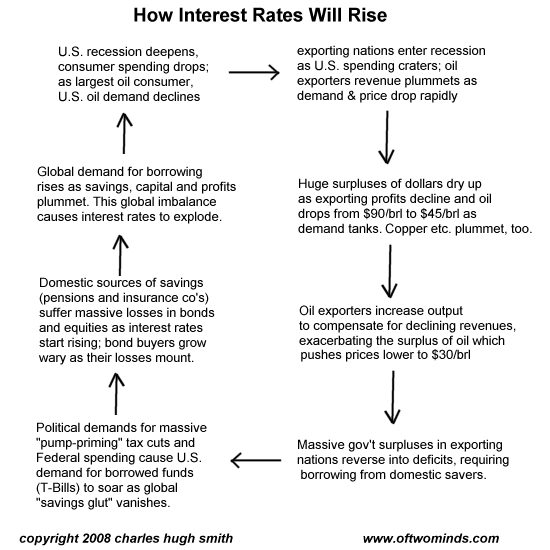

Exacerbating the supply/demand imbalance: the exporters' desperation to keep funding their bloated welfare state and energy subsidies to their own populace. The political elites' legitimacy in oil-based welfare states like Venezuela and Iran depends on providing their restive citizenry with subsidized food and oil. Once their incomes are cut in half as oil plummets, they have an unsavory choice: either cut production in an attempt to prop up oil prices, thereby cutting their own throats by reducing incomes, or pump as much as possible to compensate for the lower prices. They really have no choice but to pump as much as possible, which will only drive prices even lower. Thus we can expect massive social and political turmoil in the exporting nations as their income is halved. Here is a chart of the dynamic:

Lastly, there is a gaping, unprecedented divergence between the 10-year bond and gold, as shown here on a chart courtesy of Harun I:

This divergence could be resolved by gold plummeting, but with currencies all declining against gold, the more likely rebalancing will be a rise in bond yields (interest rates).

So place your bets: on gold and silver either rising or at least maintaining their

value, and the bond plummeting, or on bonds holding their value and gold dropping.

I personally will bet on gold and against bonds, for all the reasons outlined above.

I have been struggling with the name of the bailout, somehow TARP doesn't seem to cover the occasion. So last night I woke up at 4 a.m. and came up with the appropriate name: Congressional Rotten Assets Ponzi Scheme, or CRAPS for short. (Emphasis added: CHS) And of course when the treasury buys these bundles of mortgages/securities they will be known as Congressional Rotten Assets Packages, or CRAP for short. Helps to understand the game and the stakes. Let the dice roll. Bob Z.

The Depression is not just baked in. It is already here, though few realize it just yet. Here is some evidence that my friends in academia would dismiss as "anecdotal," but it is compelling. Riley T.

I love National Geographic TV. John G.L.

Thanks for posting my comment on the bail out. The megabubble has now absorbed so many asset classes and so much of the investment universe that it has reached critical mass...nothing can stop it now as the bubble investment is not just financial but psychological. (Emphasis added: CHS) People are still not prepared to let go. The bubble has absorbed 'private' enterprise, the media, and our elected officials...and, most importantly, people's minds. Harun I.

The divergence I speak of is the nominal price versus the real price as set by gold. Gold is saying the Dow is only worth about 5500 while the nominal price is saying its worth over 10,000. Personally I think gold and commodities have got it right. I also think that this divergence exists because of the "hockey stick" growth of credit money (debt) but I cannot prove it. The snapback I speak of is when market participants finally realize equities and bonds are extremely overvalued and nominal price goes down to real price. I do not believe this will be orderly but I could be wrong. Reader Essays:

I have been mulling over the proposed bailout bill (which I have decided should be called the No Banker Left Behind Bill). I have the feeling that no matter what they do, something big this way is coming. I just dont know what form it will take. There Is Ultimately No Gaming the System: When the Micro Crash Reflects the Macro Crash (Zeus Y., September 29, 2008) The proposed 700 billion dollar bailout cannot really work from a system level. I know its real intention is to cover the butts of Wall Street investors, but you have the same problem in macro that homeowners have in micro. Nobody knows what homes are worth right now, so buyers are sitting it out. It isnt about restricted credit (even though that is a factor). It isnt about being too cash strapped to make a down payment (though that too is a factor). Its about not wanting to be suckered into buying something that may still be overpriced.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Philip H. ($25), for your much-appreciated generous donation

to this site, and for your contributions of topics and ideas.

I am greatly honored by your ongoing support and readership.

Your readership is greatly appreciated with or without a donation. For more on this subject and a wide array of other topics, please visit my weblog. All content, HTML coding, format design, design elements and images copyright © 2008 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||