|

|

|

||||||||

|

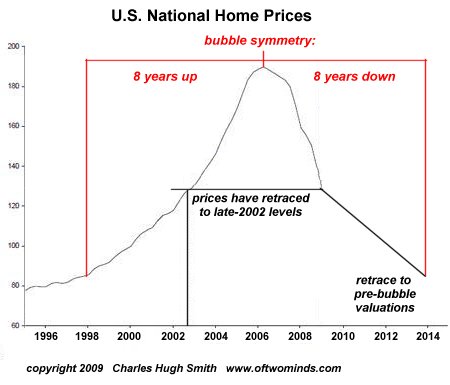

Housing: Round Trip to Pre-Bubble Prices Underway (October 26, 2009) Popped speculative bubbles tend to retrace to their pre-bubble prices. Housing has already retraced 75% of the bubble--only 25% still to go. When it comes to post-bubble retraces, the fundamental reasons may not matter as much as the technical case for a full reversion to pre-bubble prices. We all know the fundamental reasons why housing shot up--a credit bubble of epic proportions plus securitization, fraud and low interest rates, to name but a few factors--and why housing has plummeted: foreclosures and inventory are rising, tightening of credit standards by private lenders, etc. But the ultimate predictor of price is technical: speculative bubbles retrace to their pre-bubble prices, or in many cases even crash below those levels. Those arguing the fundamentals are always grasping at various straws to support the case that prices won't drop all the way back to pre-bubble levels, and they're always wrong. Thus when the NASDAQ dot-com bubble topped above 5,000 in 2000 and then sank to 3,000, the fundamental analysts piled on reasons why 3,000 was "the bottom." Indeed, the market did recover the 4,000 level briefly--at which point it reversed and drifted all the way down to 1,100, it's pre-bubble level. In other words, regardless of the fundamental reasons offered (they're not making any more land, inventory is drying up, foreclosure rates are dropping, etc.), markets tend to fully revert to pre-bubble prices. Here is a chart of the national median prices which have already reverted to 2002 levels. The future full retrace has been added as a projection:

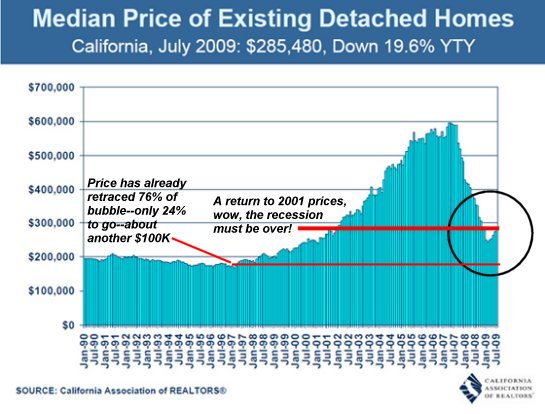

While there is no absolute way to project the final bottom, many bubbles exhibit a symmetry in their rise and fall. Thus if a bubble took eight years to reach its apex, there is some history to suggest that it will bottom out in roughly the same time span. That would put the final bottom in the 2013-2014 time frame. The truly bubblicious markets have already reverted fully 75% of the bubble. Take a look at this chart of median prices in California. Median rices have already dropped to 2001 levels--a staggering 55% decline and a 76% retrace of the entire bubble rise from $180,000 to $600,000. "Only" $100,000 more to drop for a full reversion to the starting point of $180,000.

There is no law which states that prices have to stop at 1998 levels. Given that this is median price, then high-priced homes tend to keep the median price above the average price. If high-priced homes fall precipitously in value then that would drop the median price substantially. What is not visible in purely nominal median home prices is the catastrophic retrace of homeowners' equity to levels not seen since the 1970s. What is noteworthy in this chart is that homeowners' equity has already fallen below pre-bubble levels. In other words, the average American homeowner has less equity than before the bubble tripled prices in "hot" areas.

We can surmise that equity extraction via HELOCs (home equity lines of credit) and re-financing might be the cause of this horrific loss of equity: when values shot up, American extracted some $5 trillion in equity. Now that values have dropped, equity for about one-third of homeowners has essentially vanished, along with the ability to borrow money against their homes. The consequences of a further retrace in valuations to 1998 levels are clearly dire for household wealth. If the median price of housing nationally falls another $40 -$50,000, as will occur in a full reversion, then all that decline will come straight out of remaining equity. In California, the same can be said of the expected $100,000 decline in median valuations. Some analysts have already gone on record that they expect fully 50% of all homeowners with mortgages to be underwater by 2011--that is, owing more than their equity. Half Of All U.S. Mortgages 'Underwater' By 2011: Deutsche Bank. As household equity (wealth) declines, the "reverse wealth effect" kicks in with a vengeance. Once we feel poorer, we start acting poorer--even if we don't count on our equity for living expenses. What does the reverse wealth effect mean in an economy of which 70% is private consumption/consumer spending? It means people do not feel wealthy enough to spend money they don't have, and it means people will not be able or willing to tap whatever equity does remain in their homes.

If we ponder these charts, it's difficult to conclude the consumer can recover

his/her free-spending ways and thus difficult to expect the economy to grow

on the backs of renewed consumer spending.

"Your book is truly a revolutionary act." Kenneth R.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright © 2009 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

|

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||