|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | |

Writing/Film Don't Write for Readers, Just Write Grants Ernest Lehman, Screenwriter Central Casting, Dept. of Acceptable EVil American Identity Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Japan's Runaway Debt Train Will Avian Flu Trigger a Global Depression? China and India: Five Flies in the Ointment China & the U.S.: Circle of Self-Interest China Trade Surplus: Gusher Profits for U.S. Battle for the Soul of America The End of Empire is Real Simple A Degree of Success Why the Democrats Keep Losing American Chickenhawks: Your Congress Is This a Nation at War? A Nation in Denial Hawaii National Guard: An Unfair Deployment Planetary Meltdown Watch The Immensity of Global Warming Financial Meltdown Watch Are We Entering the Next Age of Turmoil? Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Meltdown in the E.U. Meltdown: U.S. - China Retirees: the New Elite? Boomers: Prepare to Fall on Your Swords The Real Federal Deficit How much Is a Gallon of Gas Worth? What This Country Needs Is a... Good Recession The End of Cheap Oil The Word of the Decade: Gold Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono One-Word Titles Complacency Nostalgia Praxis Keys to Affordable Housing U.S. Conservation & China Health, Wealth & Demographics Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Landscapes Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Nourishment The French Village Bakery Ideas Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi History Bad Karma: Election Fraud 1960 Hiroshima: First Use Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Archives: weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

Weblog and Wessays Welcome, readers, welcome. Please browse this month's weblogs and the wEssays listed in the sidebar. If you're in the mood for a short story, check out The Adventures of Daz and Alex: Stories of America. (They're all quick reads.) If nothing here strikes your fancy, skim through my recently published articles (generally in the San Francisco Chronicle). I would be honored if you linked any essay or story to your website, or printed a copy for your own use. And of course I appreciate your recommendations of this weblog and your comments: csmith@oftwominds.com. October 1, 2005 Read This Book The nation is racing off a financial cliff with no bottom. But don't take my word for it--read this detailed account by a Republican who served as Commerce secretary for President Nixon. You might think a rock-ribbed Republican would rise to the defense of Presidents Reagan, Bush and Bush II. He does not; rather, he excoriates them all--along with all the Democratic presidents, too--for being fiscally reckless, borrowing vast sums of money to bribe constituencies today and saddling future generations with the tab plus interest. Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It The author makes it clear it wasn't always like this; the Founding Fathers and plenty of subsequent leaders were rock-solid on the dangers of accumulating enormous public debt. Yet now we have Vice President Dick Cheney stating that "Reagan proved deficits don't matter." Read this book and then try to agree with Mr. Cheney. You can't. How much will the Federal government have to come up with, via taxes or borrowing or both, to pay for the retirement benefits and Medicare for the 77 million Baby Boomers who start retiring in 2008? Try $27 trillion--or $43 trillion. The numbers vary depending on who's doing the estimating, but the bottom line is obvious--the sum is more money than the nation could ever hope to raise. The entire Federal government consumes about $1.4 trillion annually at the moment, of which $400 billion is borrowed from the Chinese and Japanese central banks (and a few other foreign central banks). Do you have any idea how much interest we collectively pay on the $8 trillion in Federal debt we already have? $335 billion, and it goes up every year. Check the official U.S. Treasury website and see for yourself. And since we're borrowing $400 billion more every year, we're insuring that the interest expense will go up every year. And this is with interest rates at their lowest level in a generation. If that doesn't frighten you, you're in absolute denial. We are paying almost as much in interest as we are for the entire U.S. Military, and if interest rates shoot up--well, then the interest expense will be greater than the cost of the Armed Forces. That's an astonishingly large and permanent burden on future taxpayers. The author forces you to accept these numbers, for everyone who's ever looked at it, from the GAO to blue-ribbon panels from both parties, reaches the same conclusions. Certainly the current generation of retirees is the greediest on record, happily scarfing up huge benefits of which they paid only a fraction of the cost during their working years; so as I have noted here before, Boomers: Prepare to Fall on Your Swords, the Baby Boomers will have to accept benefits much more constrained than those their freeloading parents raked in. (Estimates suggest cutting benefits by half might just save the system from complete collapse--if we raise taxes enough to eliminate the deficit immediately.) But as the author notes, the Republicans are in the grip of a theology of tax cuts, and they really don't care about deficits because fiscal reality is not part of their religion. The Democrats, meanwhile, have never seen a social entitlement program they didn't want to increase, even if 80% of the recipients are doing just fine without the government handout (for instance, the new Medicare drug plan give-away). The road to ruin is paved with profligate public borrowing and entitlement spending without limits. Reality has a way of interceding on fantasy, so mark the years 2006-2015 as the decade the chickens come home to roost. The best we can hope for now is a quick collapse of the dollar and an end to foreign financing of our mad borrowing. As long as the Asian central banks continue to pour the drinks, then the debt addicts currently leading our nation will happily slosh another $400 billion or $500 billion a year onto future generatiions. But read the book and come to your own conclusions. September 30, 2005 Why are we in this handbasket? I saw a bumper sticker recently which captures all too well the zeitgeist of the times: "Why are we in this handbasket, and where are we going?" The reference, perhaps obscure to some, is to the old saying that "we're going to Hell in a handbasket."

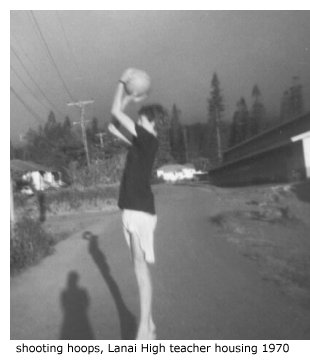

The handbasket seems to be picking up velocity recently, and as readers of this modest little blog know, I have been agape for a long time at the bizarre sense of denial and unreality which has enveloped the nation. Before I begin the laundry list of denials which appear to finally be crumbling in the face of various realities, take a look at this archival photo of me at the age of 16 shooting hoops at our old plantation house on "Teachers Row" on the island of Lanai, Hawaii. Lanai High and Elementary School is visible on the right; teacher housing (my stepfather taught chemistry and math) was conveniently located adjacent to the school. By good fortune our bungalow had a regulation basketball hoop in the driveway. For the long shots, we had to set up in the street. The Pine Lads (our school basketball team) had many outstanding players in those years, and we went to the state championships both in 1970 and in 1971 (I'd moved to Oahu by then). Alas, I added very little to the team except comic relief and a cheering bench warmer, but my jumpshot form looks pretty good here. Note also the shadow of my brother Craig as he snapped the shot of the shot, and the tall Norfolk pine trees which line the central quandrant of Lanai City. OK, here's the connection between "going to Hell in a handbasket" and a photo from 1970: we were going to Hell in a handbasket, then, too. Herewith are various fantasies currently crumbling as the basket gains momentum: On the other hand, in 1970 the Vietnam War was still raging and the American people were beginning to doubt the management and ultimate cost of that war. Although the analogies between Vietnam and Iraq are largely false (but that is another entry), the salient point here is whether the American people support the war or not. It has been apparent for some time that the post-war planning was inadequate, and that the leadership of this nation fired or suppressed anyone who questioned the adequacy of their plan--to mention but one example of many, General Eric Shinseki. Gen. Shinseki, a combat veteran of Vietnam who is missing part of a limb as a result of his service to the nation, was convinced that we needed 200,000 or more ground troops to secure post-war Iraq. He was quickly snubbed by the chicken-hawks (those who never served or weaseled their way out of service during Vietnam) and shuffled off to retirement. Their over-reaching arrogance is now coming to haunt them--as it should. The losers, unfortunately, are our citizen-soldiers. This is not an opinion on the nature of the war or the conduct of the war--that is too complicated for this entry-- but simply a statement of fact that the American people are beginning to question their leaders' handling of the war. At some point, Whether the war is "winnable" or not will no longer matter, for once the American people no longer support it, it's politically untenable. The parallels to 1970 should not be dismissed too lightly. If you don't see the parallels, well, you're not paying attention. But you will--you will. September 29, 2005 What a difference 27 years makes I came across a clipping of food columnist Susan Dart from June 14, 1978, detailing her trip to mainland China as one of the first journalists allowed to visit the newly opening nation. All I say is, wow: What a difference 27 years makes. (The following are excerpts from the column.) I have bolded those comments which most visibly highlight that bygone era.

"China is the most totally controlled place I have ever been. Everyone appears to be exactly like everyone else. To begin with, they all dress alike, even though it is not obligatory to do so.Interestingly, Dart's observations about food remain largely true, although meat consumption and junk food are on the rise. Her assumption that Chinese people don't care much about eating is of course patently absurd to anyone who knows anything about China, its history, culture and cuisine. It would be more accurate to say that we are obsessed with weight while the Chinese are obsessed with food preparation and gustatory enjoyment. Sadly, the health of the Chinese people is deteriorating as rapidly as their air and water quality. (Scroll down to the Sept. 22 entry for more.) Streets that were crowded with bicycles just five years ago, never mind 27 years ago, are now jammed with vehicles. As for the uniform clothing: no one who visited Shanghai in 1978 would recognize the chic, well-dressed masses of young people filling NanjingLu, the city's primary retail shopping street. With industrial-era consumer choice and production comes industrial-era pollution and disease. September 28, 2005 The Conundrum Effect Talk about macroeconomic conundrums. Poor Federal Reserve chief Greenspan has mentioned three himself. To paraphrase: One term the Chairman never uses is the "wealth effect." Why? To paraphrase again: "Wealth effect? Are you nuts? That's like saying there's a housing bubble. People will panic in the streets if I admit that the wealth effect works great when housing is going up--everyone feels so rich they spend like there's no tomorrow. But the same mechanism works on the way down, too, after the bubble pops. People feel poorer than they actually are, and so they stop spending. Economic activity goes into a tailspin and then we've got the big R, recession, or worse. The bigger the bubble, the bigger the pop and then the bigger the drop in the wealth effect. But for goodness sakes, don't let on we know that. I retire in a few months and want to get out while the getting's good, before the whole thing blows up." Think I made this up? Please read today's Wall Street Journal article entitled Greenspan Says Fed's Success May Inflate Bubbles. "In perhaps what must be the greatest irony of economic policy making, success at stabilization carries its own risks," Mr. Greenspan said in a speech via satellite to a conference of the National Association for Business Economics in Chicago Tuesday.In other words: Yikes! Look out below. September 27, 2005 When Empire Was Easy The Jule Vernes story Around the World in 80 Days

Phileas Fogg, the emotionless, neurotic epitome of an upper-crust Englishman (David Niven) does basically nothing, while his "gentleman's gentleman" valet, Passepartout, (Cantiflas) performs all the heroics. Niven spends most of the film checking his watch and regally enjoying his tea, rain or shine, while Cantiflas braves the rigors of the bull-fighting ring, clambers atop a speeding train beset by attacking Sioux (sadly lacking the firearms they most certainly possessed by the 1870s), and rescues a Princess in India from a blood-thirsty horde while the upper-class Englishmen watch from a safe distance--hmmm. The one moment of physical courage Fogg endures is a foolish, prideful duel with a cantankerous cliche of a Southern gentleman, a duel which is interrupted by a propitious attack on the train by "Red Indians." I haven't read the book since childhood, but I wonder if this isn't an American subtext of sorts--we did, after all, throw off the weight of the Empire at the cost of a seven-year war which was both a world war (recall that we won thanks to the French fleet blockading Cornwallis' army from re-supply or evacuation) and a civil war in which at least 40% of the populace either actively or passively considered themselves loyal British subjects. With our own "Empire" (not of territories so much as influence and alliances) girdling the globe as a result of being "last man standing" at the end of World War Two, this film reflects the American ambivalence to Empire. The British overlords are portrayed as supercilious, petty buffoons, confident in their right to rule but doing nothing for themselves, quite content to order their servants around. Yet the structure which enabled the Empire to work gets a favorable treatment; Fogg cannot be arrested in Cairo by the incompetent British detective tailing him because the warrant has not yet arrived from London, and the Imperial ships and trains all leave on schedule. The film offers a model of global reach which was admirable in its orderliness, functionality and rule of law. Of course the moral righteousness of the Empire is made clear: heathen "natives" are either burning the poor Princess (played by very pale Shirley McClaine) on a funeral pyre or trying to torch poor Cantiflas at the stake (during the hopelessly campy "Cowboys and Indians" sequence). The viewer cannot help but be struck by the leisurely pace of the film. Segments which would be cut to a few manic seconds in a modern version are allowed to unfold in real time: a Spanish dance, Cantiflas' fledging efforts as a bull fighter, scenes of the Indian countryside from the train window, etc. It's hard not to conclude that modern audiences suffer from attention-deficit syndrome and cannot bear to watch any scene in real time except intricately plotted "action" sequences. There are exceptions, of course, and these are often the better films of our era. I recommend the film not just for its cast and dialogue or as a snapshot of a bygone era in film-making, but for its fascinating array of subtexts. September 26, 2005 Doubling Down on 5-Card No-See-Um To use a poker analogy: the world's bankers are doubling down, but they have no clue what the cards hold for the world economy. We are in uncharted territory in five major ways: And the dealer's first visible card:  The net result is an unprecedented number of opaque risks which could bring the global expansion to a halt.

Let's start with hedge funds, secretive, poorly regulated and now larger than most corporations or mutual funds.

Check out this

BusinessWeek expose on Cerberus, a hedge fund which started out with $10 million in 1992 and is now larger

than McDonald's, 3M or Coke. Would you like to know something about the company's inner workings? Sorry, that's

privileged, not public information like you get from a publicly traded company. Might Cerberus be

holding a trillion dollars in risky derivatives? Maybe. We'll never know until it's too late.

The net result is an unprecedented number of opaque risks which could bring the global expansion to a halt.

Let's start with hedge funds, secretive, poorly regulated and now larger than most corporations or mutual funds.

Check out this

BusinessWeek expose on Cerberus, a hedge fund which started out with $10 million in 1992 and is now larger

than McDonald's, 3M or Coke. Would you like to know something about the company's inner workings? Sorry, that's

privileged, not public information like you get from a publicly traded company. Might Cerberus be

holding a trillion dollars in risky derivatives? Maybe. We'll never know until it's too late.

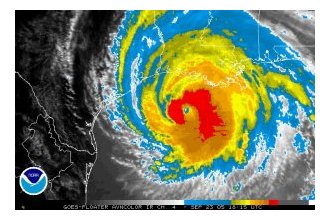

Risk factor: unprecendented. Trillions of dollars are sloshing around, completely unregulated. While the markets are cheering that oil is "only" $63 a barrel today--stock markets around the world are roaring up in euphoria--the bottom line is still that supply is capped and demand continues to rise. Yes, giant new fields may be discovered, but it would take 10 years to start getting gasoline from them (that's if any are found, which is doubtful). And yes, the Saudis want to build a couple of refineries to process their heavy sulfur-laden crude oil, but that's at least a 7-year process. So there are no near-term solutions except to cut demand, and so far there are few indications that China's economy will need less oil or Americans will do more than trim the edges off their 23 million-barrel a day habits. Risk factor: unprecendented. Never before has total global supply of oil been unable to meet demand. As the new book End of the Line: The Rise and Coming Fall of the Global Corporation Risk factor: unprecendented. Interdependency and "just-in-time" component systems are now acutely vulnerable to local crises which could disrupt the entire chain. To assess the risks posed by trillions of dollars in exotic financial derivatives, scroll down to my September 16 entry for a chart showing the explosive growth of these "financial instruments." "Instruments" doesn't sound too scary, does it? Risk factor: unprecendented. No one knows how these trillions of dollars of inter-connected derivatives will unravel in a financial crisis. Such crises have not been outlawed--they are an integral part of the system. The chart above vividly shows the U.S. trade deficit is now so enormous that it is offsets the entire surplus created by the exporting nations. At 7% of GDP, our trade deficit is truly unprecedented. Historically, economies collapse on themselves at 5% of GDP trade deficits. Risk factor: unprecendented. No one knows how long the U.S. trade deficits can keep rising without triggering a reversal. Never mind the prospect that some terrorist cell will figure out that economic terrorism (blowing up a refinery, for instance) is the strategy to follow if you really want to bring the U.S. down. Let's just stick with the risks that are visible. As the global financial institutions continue to double-down their bets that these imbalances can continue expanding more or less forever, it has finally dawned on me that they have no clue what they're doing. Fearing any change might bring the system down, they continue doubling down the bet that the game can go on with the cards never being called, that is, turned up. Are they really holding four aces, and all these unprecedented risks are vanishingly small, or are they actually bluffing a hand of a pair of two's, a four, a nine and Jack? Go over the list again and decide for yourself. September 24, 2005 A One-Two Punch to a Glass Jaw: the Knockdown of Recession Take a look at the false-color image below from the NOAA Storm Tracker site on Friday, tearing through oil platforms on its way to the coast. Now tell me this one-two punch to the delicate glass jaw of the region's oil refining and natural gas complex is no big deal and the U.S. economy will barely notice it. Unbelievable, but that malarky is the official Wall Street line. I have personally witnessed two well-publicized natural disasters, the Loma Prieta Earthquake of 1989 and the Oakland Hills Fire of 1991 which destroyed 3,000 homes. Although the loss of life and property was tragic, these two events were chump change compared to the damage wrought by these hurricanes. More importantly, these S.F. Bay Area disasters had virtually no effect on the rest of the nation. Their influence was entirely local. Contrast that with the destruction wreaked on the nation's oil and natural gas complex by Katrina and Rita. The scale of damage and the expense of repairing the damage are beyond ready measure; everyone is relying on back-of-the-envelope estimates which aren't even close because the full damage hasn't even been totalled. Nobody can say how prices of gasoline and natural gas will be affected next month, never mind next April, because no one can say whether foreign refineries can compensate quickly enough to suppress prices. We already import 1 million barrels of refined fossil fuels every day, and it simply isn't possible to ramp that up overnight by another million barrels. But don't take my word on it; read a blog written by industry insiders. Katrina and Rita will disrupt essential refining capacity and the delivery of natural gas for many months; the facilities, tankers and pipelines to carry enough product to minimize that impact simply do not exist. Put another way: the recession of 2006 just started. September 23, 2005 The Flutter of a Butterfly's Wings?  The cliche is that the flutter of a butterfly's wings may spawn a hurricane. Perhaps, but then

The cliche is that the flutter of a butterfly's wings may spawn a hurricane. Perhaps, but then what does a hurricane spawn? The cliche is based on chaos theory, in which changing the initial state of a system by a small amount can cause enormous changes in the eventual outcome. So who can say with certainty what the outcome of Katrina and Rita will be in six months? No one, of course, but we can look at the initial state of the system, in this case, the U.S. economy, and draw some conclusions from its current precariousness. The Economist has assembled an in-depth look at the growing imbalances in the global economy. To quote from one of the essays:

"It is commonly argued in America that if the housing bubble were to burst, and falling house prices threatened to choke consumer spending, the Fed would slash interest rates to prop up the economy, as it did after the stockmarket bubble popped in 2001-02. But then inflation was falling. Today, with inflation rising, the Fed would no longer have that option. If the economy hits trouble, investors and homebuyers should not expect to be bailed out again."Take a look at the chart, and note how our nation's household savings rate has fallen below zero (the lefthand scale) even as our net worth (righthand scale) has climbed along with housing values. The trap is all too visible here: household net worth dropped precipitously after the 2000 dot-com stock market meltdown, but then shot back up as housing prices skyrocketed. Now that peak has topped out and net worth is starting to decline as Americans pull vast amounts of cash from what they now consider their "savings account," their house.  Lest you reckon I am exaggerating, then feast your eyes on the next chart, which reveals our household debt

payments are rising to unsustainable levels.

As the quote suggests, the Federal Reserve will not be able to pump up housing values next time

around because now we have

inflation to worry about.

Lest you reckon I am exaggerating, then feast your eyes on the next chart, which reveals our household debt

payments are rising to unsustainable levels.

As the quote suggests, the Federal Reserve will not be able to pump up housing values next time

around because now we have

inflation to worry about.

As a result, we can safely predict three effects of Katrina and Rita: inflation caused by rising transportation and energy costs will filter through the supply chain, raising prices of everything, gasoline-pinched consumers will have a harder time paying their debts or acquiring new debt, and interest rates will have to rise, not drop, to combat the hydra-headed monster of inflation. Put more simply: the cash machine called the American house will jam, interest rates will rise, making debt ever more costly, and inflation and energy will take a bigger piece of Americans' dwindling paychecks. If you consider the charts and reports objectively, there are no other possible conclusions. Thus do the butterfly wings flutter. September 22, 2005 Air Pollution and China's Future  A new epidemiological study reported in

Scientific American Online this week highlights the long-term dangers of air pollution.

A new epidemiological study reported in

Scientific American Online this week highlights the long-term dangers of air pollution.

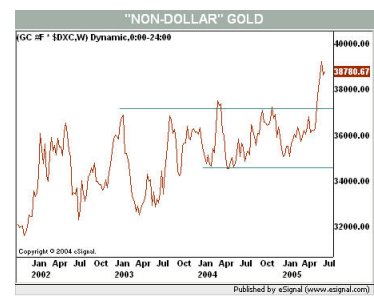

"They found that as the number of fine particles less than 2.5 microns in diameter increased, so, too, did the risk of dying: each jump of 10 micrograms per cubic meter corresponded to a 11 to 17 percent increase in the risk of dying from any cause."Particulates are generally measured as either PM-10 or PM-2.5, indicating concentrations per cubic meter of particles either 10 microns or less in size or 2.5 or smaller. The Average Annual Mean for PM-10 in central Los Angeles is around 44. By comparison, some cities in China have levels ten times higher. Consider this excerpt from report from the U.S. Embassy in China: "The average concentration of total suspended particulates (TSP) in the city in 1998 was nearly 600 micrograms per cubic meter, according to the World Resources Institute. Local health experts say about 80 percent of Taiyuan�s suspended particles are "respirable" (less than 10 microns in diameter). This would imply the average concentration of lung-damaging PM10 is more than 450 micrograms per cubic meter � nine times the U.S. standard for annual exposure. Add in high levels of SO2 and nitrogen oxides (NOx) and Taiyuan�s composite air pollution index regularly tops the list among China�s 42 major cities."So let's do the math. If a rise of only 10 PM-2.5 causes a 10 to 15% increase in mortality, what would a concentration of 100 to 200 PM-2.5 do to a population's health? It would obviously drive a significant percentage of residents to an early grave, and indeed, anecdotal evidence suggests many urban Chinese are dying in their 50s and 60s from the very lung and heart diseases exacerbated by severe air pollution. When you consider the total urban population in China is 515 million people, the terrible human toll of this air pollution becomes clear. For a summary of China's horrendous pollution problems, read this September 2004 report from the Washington Post and my own essay China: An Interim Report. By all accounts, the Chinese government is aware of the dangers and is moving to reduce air pollution; but the policy changes are obviously not deep enough or fast enough to significantly improve public health in urban China. For an overview of global urban air quality, take a look at this World Bank chart of air quality of major cities around the world. It appears to seriously under-report particulates in China's cities, as Taiyuan's particulates per cubic meter is listed as 105, while the U.S. Embassy report states it's nearly 600 PM. Though that difference suggests gross under-reporting of actual concentrations, the chart still provides a comparison of global cities' air quality. For a list of the U.S. cities' rankings in air quality, check out American Lung Association Chart of the 25 U.S. Cities with the Worst Air Pollution And lest you think it's a localized urban risk, think again; it's a global problem September 21, 2005 Is Obesity an Inflammatory Response? I came across this fascinating bit of medical research into the links between sleep deprivation, obesity and inflammation. The study suggests that the less sleep you get, the more obese you are likely to be. This is interesting in itself, as Americans are notoriously short of sleep. Perhaps the rising rates of obesity are causally linked to this lack of sleep. Even more interesting is this quote from the paper: Leptin promotes inflammation. The hormone provides an interesting link between obesity and pathophysiological processes such as insulin resistance and atherosclerosis, and disorders such as autoimmune and cardiovascular diseases and the metabolic syndrome. Increased serum leptin levels in obesity and metabolic syndrome support the view that these disorders are in fact low-grade systemic inflammatory diseases, characterized by increased concentrations of proinflammatory cytokines like interleukin-6, tumor necrosis factor and leptin. Leptin's proinflammatory role suggests that it may link energy homeostasis to the immune system.In other words, obesity--the result of inactivity and sleep deprivation--may trigger an immune response to low-level inflammation which ends up causing diabetes (insulin resistance) and heart disease (atherosclerosis), as well as other autoimmune/inflammatory diseases such as arthritis. As for why Americans don't sleep enough, many people point to overwork and busy lifestyles. My own experience is that while these conditions do inhibit sleep, the countermeasure which leads to long, blissful sleep is exercise--not necessarily a punishing run, just a good fast walk or bike ride. So we can see the outlines of a negative feedback loop: less exercise causes less sleep, and the two together stimulate obesity, which triggers an immune response to chronic inflammation which leads to diabetes, heart disease and a host of other auto-immune ailments. September 20, 2005 Gold! My entry of July 11, 2005 called attention to the break-out in non-dollar-denominated gold, alerting readers to its future rise. Voila! Dollar-denominated gold has recently risen to 17-year highs, with no signs of abating long-term. As a result, I am reprinting the July 11 entry, for it still holds true in my view. This is not to say that gold won't pull back from it's recent high, perhaps sharply. But that will provide those of us who see it as a hedge against inflation another opportunity to buy. * * * If you had to choose the most important word for the balance of this decade, what would it be? Wie, as in Michelle? Terrorism? Petroleum? My vote goes to gold--not as jewlery, but as a financial hedge against all the bad things which could start unfolding next year.  The belief in the inherent value of gold has been dismissed for 25 years as the rantings of "gold bugs,"

but take a look at this chart (courtesy of Barrons and eSignal) which tracks gold in non-Dollar currencies.

It shows what chartists call a "break-out," meaning that gold has broken out of a trading range and is reaching

new highs--highs which are cloaked to us in the U.S. by the current strength of the dollar.

The belief in the inherent value of gold has been dismissed for 25 years as the rantings of "gold bugs,"

but take a look at this chart (courtesy of Barrons and eSignal) which tracks gold in non-Dollar currencies.

It shows what chartists call a "break-out," meaning that gold has broken out of a trading range and is reaching

new highs--highs which are cloaked to us in the U.S. by the current strength of the dollar.

Gold is an interesting placeholder of value because you can buy the actual metal in coins, or gold mining stocks, or an exchange-traded fund (ETF) which holds physical gold. The Establishment (such a 60s word) or the Standard Economic Model (to paraphrase physics) has no use for gold. Everything is absolutely hunky-dory as is--low inflation, rising real estate values, low unemployment--this is the best of all possible economic worlds, and there is little Establishment doubt that any disruption would be short-term and modest in effect. Uh-huh. Still, I'm sticking with Gold as the key word for the next five years. It's something the "little guy" can buy to protect whatever assets he/she has accumulated--something which cannot be said for perquisites of the wealthy such as hedge funds. September 19, 2005 Monday Morning Grab-Bag Here's a piece from the Washington Post outlining exactly what I'd described in my Sept. 2 entry--that all the New orleans houses that were flooded, even just a few inches above the floor, will have to undergo major work that may well match the expense of building a new house when all is said and done. In an unrelated bit of questionable timing, minimum credit card payments will begin rising for many consumers as early as October, which just coincidentally is when the new bankruptcy law kicks in, making it more difficult to blow off all that credit card debt we've collectively been accumulating. Then there's the little matter of natural gas rising 40% as a result of Katrina-caused shortages and a potential 31% rise in the cost of heating oil. But really, everything's wonderful, so go back to spending like crazy. Interest rates are still low (for now), people have jobs (except for all those people wiped out by Katrina), and crude oil is dropping all the way back to $63 (wasn't everyone freaking a year ago when it hit $50?) now that this Katrina thing is blowing over. That's the official Wall Street word. So never mind those 40% and 30% energy cost increases this winter, or the higher credit card payments. Foreign stock exchanges are hitting four-year highs everywhere from Britain to Japan, so obviously the future's so bright we gotta wear shades. Pardon me if my skepticism is showing. September 17-18, 2005 Adios, O Bogus Prosperity

Fondly do we hope, fervently do we pray, that this mighty scourge of war may speedily pass away. Yet, if God wills that it continue until all the wealth piled by the bondsman's two hundred and fifty years of unrequited toil shall be sunk, and until every drop of blood drawn with the lash shall be paid by another drawn with the sword, as was said three thousand years ago, so still it must be said "the judgments of the Lord are true and righteous altogether."For those who didn't grow up in a deeply Christian household, allow me to translate: slavery was a terrible sin, and the massive slaughter of the War was payment in kind for this sin. If God wills it, then the cost of redemption may be the entire wealth of the nation and a measure of blood equal to the suffering of those millions the nation enslaved. Although the sins of greed, self-absorption and wanton excess are much less than those of slavery, I wonder if there won't yet be a cost to our nation's mindless denial of fiscal, social and environmental realities. Not a happy thought, perhaps, but perhaps it's time to face the gathering storm head-on. September 14, 2005 Deforestation and Sustainable Forestry  The difficulty in saving the Amazon is people--the ever-growing number of usually impoverished people

trying to eke out a living in what is fundamentally a fragile, easily degraded habitat with poor soil.

The difficulty in saving the Amazon is people--the ever-growing number of usually impoverished people

trying to eke out a living in what is fundamentally a fragile, easily degraded habitat with poor soil.

This map, and the accompanying article on NASA's Earth Observatory website show that fire, both intentionally set slash-and-burn agricultural fires and those started accidentally, is fast consuming the entire Amazon. The authors' studies, conducted over a 20-year period, reveal that the damage caused by fires extends far beyond the land that has been cleared by logging and slash-and-burn agriculture; any fire opens an exposed area of land which, as it dries out in the Amazon's dry months, becomes increasingly vulnerable to more fires.

As a result, previous estimates of deforestation have radically under-reported the actual amount of forest which has been damaged, perhaps fatally. There are a host of other inter-related problems eroding the Amazon. Roads cut by logging companies are pernicious in several ways: they enable slash-and-burn farmers to extend deeper into heretofore virgin forests, and they balkanize the forest into areas which are too small to support full-spectrum habitats. (E.O. Wilson states that reducing an area by a third may destroy half of the creatures and plants who once thrived in the larger parcel.) Since people, and their governments, already occupy the Amazon, the only way forward is to foster rules and plans which make their livelihoods sustainable, so that the remaining forest can be preserved. One essential step in many to reach this goal is to gather reliable data on natural reforestation of previously logged parcels--just what Ashton's team accomplished. The complexities of sustainable forestry will require another entry; not all trees in the forest are economically harvestable, and not all have commercial value. Each species has a different minimum "footprint" and a different number of "parent trees" required for re-propagation. Such research as depicted below is the necessary pre-condition to establishing truly sustainable logging in the Amazon. The solution is to utilize the land which has already been cleared or disturbed--such as the previously logged land Ashton's team studied. Nurturing the land which has already been degraded with sustainable practises means that the inhabitants have less need to destroy virgin lands to make their living. September 13, 2005 Real Science  Many of the knottiest problems in the world today cannot be fixed by white-coated lab techs

in nice clean business parks--they require real data, collected in some of the globe's harshest terrains

and habitats.

Many of the knottiest problems in the world today cannot be fixed by white-coated lab techs

in nice clean business parks--they require real data, collected in some of the globe's harshest terrains

and habitats.

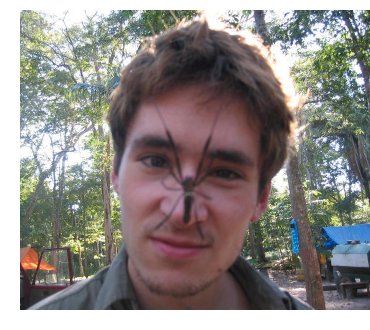

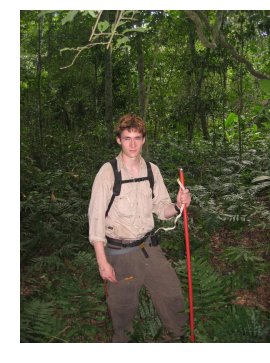

Consider, for instance, the Amazonian rain forests in Bolivia, just east of the Andes. Here is a typical insect you might encounter there while collecting data, along with a host of much less impressive but much more dangerous biting insects which are vectors for a variety of compellingly nasty diseases. The young man sporting the facial spider is Ashton Erler, a very adventuresome and dedicated friend of mine. He recently returned from leading an expedition into this section of the Amazon basin to study the regrowth of previously logged forests. Planning and funding the two-month expedition took the better part of a year, and required surmounting entire ranges of logistical and bureaucratic obstacles.  A political crisis erupted as the research group gathered, injecting a further element of volatility in an already

precarious knitting of governmental support (guides, etc.) and access to protected lands.

A political crisis erupted as the research group gathered, injecting a further element of volatility in an already

precarious knitting of governmental support (guides, etc.) and access to protected lands.

Despite these difficulties, Ashton's team of youthful academics and seasoned guides proceeded into the jungle and conducted two months of data acquisition under trying conditions. The work was essentially transecting quandrants of the forest which had been logged decades earlier, charting the type and size of the trees which had grown in the ensuing years. Photographs of the canopy were also taken which will provide accurate data about the composition and density of the new growth. This data is important on many levels, but the primary goal will be to help the Bolivian government lay out a logging plan for the area which is sustainable over the long term. This is a complicated subject which I will write more on tomorrow. For now, let us be grateful that dedicated people, both in government and academia, are devoting themselves to collecting the data without which no sustainable progress can be made. September 8, 2005 (Note: I will be out of town 9/9 - 9/12; next post 9/13/05) A Financial Meltdown in the Making  Here is a Tale of Two Charts. The first one reveals how deeply banks have jumped into the over-extended

and increasingly risky home mortgage market, while the second chart shows rather vividly how bank reserves against

bad debt--i.e., defaulted mortgages and the like--have sunk to 19-year lows.

Here is a Tale of Two Charts. The first one reveals how deeply banks have jumped into the over-extended

and increasingly risky home mortgage market, while the second chart shows rather vividly how bank reserves against

bad debt--i.e., defaulted mortgages and the like--have sunk to 19-year lows.

In other words, right when they're assuming huge piles of risk, they're also cutting their bulwarks against risk to the bone. If this isn't the definition of pure folly, then what else do you call it? Fiscal prudence?  If you set out to create a financial crisis, you couldn't do better than this: right at the top of an unprecedented

financial bubble (scroll down to the Sept. 3 post, and also check the three "Housing Bubble" essays in the sidebar

on the left) in housing, then concentrate your assets to an unparalleled degree in the very asset class which is riding at

the top of the bubble.

If you set out to create a financial crisis, you couldn't do better than this: right at the top of an unprecedented

financial bubble (scroll down to the Sept. 3 post, and also check the three "Housing Bubble" essays in the sidebar

on the left) in housing, then concentrate your assets to an unparalleled degree in the very asset class which is riding at

the top of the bubble.

Buying mortgages today is the equivalent of buying the Internet stocks in February, 2000, when the Nasdaq was days away from its high of 5300. (It's 2100 today.) Then reduce your reserves against any potential losses to the absolute lowest level in a generation. The recipe for an unfolding crisis is complete; now lower to simmer and hope for some external shock--say, an era of rising energy costs--which will push heretofore boundlessly optimistic consumer confidence over the inflection point to doubt. Once housing prices stop rising--and that moment seems to have arrived--then an era of defaults and losses begins which will erode away all that risky debt lenders have been falling over themselves to create. Ah, but I forgot--this time it's different. September 7, 2005 Welcome to 1935 As an aperitif for today's substantial offering, click on these two websites: Bureau of Labor Statistics Bureau of the Public Debt On the BLS website, select the "inflation calculator" link in the upper left column titled "Inflation & Consumer Spending." Now select the year "1987" in the calculator and plug in $100. Click the button and voila, you find it takes $172 today to buy what $100 bought in 1987. Okay, now go to the Bureau of Public Debt and note that as of September 30, 1987, the Federal Deficit was $2.35 trillion. Next, note that the debt as of today is $7.94 trillion. Now multiply the 1987 debt ($2.35 trillion) by 1.72 to adjust the debt into current dollars: voila, $4 trillion. In other words, if the debt had risen only with inflation, it should be around $4 trillion, not $8 trillion. Doesn't the fact that our government has borrowed $4 trillion over and above inflation in the past "low-inflation" 18 years strike you as somewhat troubling? After all, one trillion here, one trillion there, and pretty soon you're talking real money. Now for the main course: a chart comparing the Dow Jones Industrial Average and the Nasdaq from their respective pre-collapse highs in 1929 and 2000. To avoid a confusion of dates, the timeline is measured in days from the peak rather than years. The vertical axis measures the two stock indices' decline from their highs by percentage. Thus we see that by some uncanny coincidence both the Dow and the Nasdaq rose to about 45% of their pre-collapse highs at the same time--2000 days after the highs, right about now for us in 2005 and right about April 1935 for the previous generation of "investors."

The present status of the Nasdaq is roughly analogous to April 1935, when, we note, the Dow took a major cliff-dive. Chartists have long observed that the stock market tends to form patterns which repeat over the years, decades and even centuries; they do not see coincidence in the close correlation of these two lines but repetition of an underlying pattern: a mania bubble which bursts dramatically, setting up a more leisurely "echo" of the bubble--where we are today--which is followed by a collapse of the "echo" boom. The overlay rather persuasively suggests that the deflation of the echo boom is close at hand. For an explanation for why the Nasdaq recovered more quickly than the Dow, look no further that the extraordinary dumping of low-interest cash into the economy which began in 2001. The Fed poured trillions of new dollars into the money supply in the past four years, something which did not occur in the early 30s. Despite this largesse, we find ourselves at exactly the same point 5.5 years out from the peak--on the edge of a secondary cliff. Okay, so you don't believe overlaying charts has any predictive value. Well, how about the statistic that bull runs historically average about 30 months in duration? We are now at month 35 in the current run up from the low set in October 2002. If that doesn't give you pause, then allow me to usher you to the Permanent Bulls Table over in the corner, where the banter today is all about how resilient the U.S. economy is in the face of fearsome energy cost increases. The table is thronged with excited traders today, but check back in December; the crowd--and its ebullience--may have noticeably thinned by then. September 6, 2005 Tinseltown Tags Titles from Bard I was watching the classic film version of Hamlet To Be Or Not to Be Outrageous Fortune What Dreams May Come The Undiscovered Country (Star Trek V) Here are the lines Tinseltown tagged: "To be or not to be, that is the question." "The slings and arrows of outrageous fortune" "For in that dream of death what dreams may come" "The undiscovered country from whose bourn" (boundary) I took two semesters of Shakespeare in my years at the University of Hawaii, and yet I do not recall our very learned professor pointing out how shamelessly Hollywood (as well as various authors, e.g. "The Sound and the Fury," etc.) mined the Bard for titles. The Laurence Olivier version of Hamlet, in glorious black and white, is unparalleled in both the lighting (stark at times, fog-strewn in others), setting (the largely vacant, cold castle and wild landscape beyond, all worthy of Jean Cocteau at his finest) and in the delivery of secondary parts; I most especially recommend the scenes featuring the ghost of Hamlet's father. September 5, 2005 Labor Day: Thirty Years and Counting  Here's a shot of me and my friend Steve Toma, proving that a Skil 77 (the big worm drive power saws) and two

50-year old guys make a righteous production team. We met on a jobsite back in late May 1973, and are

still going strong (unretouched photo from a rainy jobsite in Honoka'a, Hawaii, 2004). The Skil 77 is the

professional carpenter's choice; it weighs 16 pounds (feels like 25 lbs. late in the day) and has to be handled

with one hand except for above-the-head or other tricky cuts. A normal (i.e. sedentary) person unused to actual physical labor would

have trouble lifting it with both hands, never mind lifting it with one hand to cut a 2X12 board.

Here's a shot of me and my friend Steve Toma, proving that a Skil 77 (the big worm drive power saws) and two

50-year old guys make a righteous production team. We met on a jobsite back in late May 1973, and are

still going strong (unretouched photo from a rainy jobsite in Honoka'a, Hawaii, 2004). The Skil 77 is the

professional carpenter's choice; it weighs 16 pounds (feels like 25 lbs. late in the day) and has to be handled

with one hand except for above-the-head or other tricky cuts. A normal (i.e. sedentary) person unused to actual physical labor would

have trouble lifting it with both hands, never mind lifting it with one hand to cut a 2X12 board.

Those 2X12 rafters laying on the slab in front of us were "pond-dried," i.e. completely waterlogged, and each one must have weighed over 100 lbs. The fact we framed this huge garage and hefted all of the rafters up in two rain-plagued days without getting hurt is a testament to the way experience teaches you to lift and cut safely.

There is no substitute for the physical skills of building, gardening and mechanics; no amount of "work" talking on the phone or staring at a computer screen gives you the same appreciation for food and water, for the joys of exertion, for the visible nature of the day's accomplishment, for the turns of weather, for the pleasures of hand-skills which come unbidden and without thought, or for the accumulation of decades of physical experience. The usual Labor Day bromides count the blessings bestowed on American workers by the labor unions' bitter struggles early in the 20th century to obtain better working conditions and wages for industrialized laborers. Not to take away from those enormous achievements, but what I think of on Labor Day is how much we've lost in becoming an overwhelmingly skill-deprived, physically inept (can't cook, can't fix anything, etc.) society of unhealthy service workers who have largely lost the keenly felt benefits and rewards of physical labor, both skilled and unskilled. September 4, 2005 Read This Book: Boiling Point If you want to understand why rising carbon dioxide levels from burning fossil fuels and the subsequent global warming is a big deal, read Boiling Point. As I have noted before (The Immensity of Global Warming), the magnitude of this warming is difficult to grasp--unless the ground is literally melting, as it is in parts of previously permafrost Alaska. Yes, there is an ongoing scientific debate about whether global warming is spawning super-storms like Katrina, but read the book before making up your mind. (It's a short and easy read.) One point is well beyond debate: Nature didn't add 100 ppm of carbon dioxide to the planet's atmosphere, humanity did. And that count continues to rise as we burn mountains of coal and 83 million barrels of oil each and every day. September 3, 2005 Catalyzing the Great Unraveling  One of high school chemistry's most visual experiments may provide an analogy to Katrina's effect on

the U.S. and world economies. First, salt is dissolved in warm water

to the point of saturation. As the water cools, a point is reached where a sharp tap on the beaker causes the

salt to instantly crystallize.

One of high school chemistry's most visual experiments may provide an analogy to Katrina's effect on

the U.S. and world economies. First, salt is dissolved in warm water

to the point of saturation. As the water cools, a point is reached where a sharp tap on the beaker causes the

salt to instantly crystallize.

The point is not that Katrina's aftermath may prove to be the proximate cause of the great unraveling, but that the global financial situation is so precarious that any shock would have been an equally effective catalyst. Consider two apparently unrelated items from the August 22 edition of the Wall Street Journal, one on U.S. bank's dwindling reserves to offset future bad loans, and the other on the growing power of an obscure Chinese banking agency which now owns half of the biggest Chinese banks: In the U.S.:So let's see if we have this straight. Just as risky interest-only mortgages are increasingly the bread-and-butter of the U.S. banking system, then these same banks are lowering their reserves for bad debts in order to appear profitable. At the same time, total U.S. debt has skyrocketed (see chart above). Can you say "disaster in the making?" At the same time, a politically byzantine, utterly opaque quasi-governmental agency of the Chinese Central Government has "saved" China's largest banks from insolvency by pumping $60 billion into the biggest three and untold tens of billions more into smaller rivals--all in the hopes of enticing Western capital to flow in and save them the trouble of throwing more money down the bottomless rathole of the Chinese banks' bad debt. Do these stories paint a picture of a robust, transparent, low-risk global financial system? On the contrary, they reveal a system poised on the precipice of collapse. September 2, 2005 Off the Scale Misery  Anyone who thinks the aftermath of Hurricane Katrina will be short-lived or benign is in fantasyland. We have 500,000

homeless people, maybe closer to a million, people with no way to return home for months on end. Note that most major

cities consider 10,000 homeless people an enormous challenge. Also note that those who fled are the ones with

the means to do so--those with cash, cars, nearby relatives, and so on. Those who remained behind did so because they

had no place else to go, and no money for a few weeks in a Houston hotel. They are effectively

homeless people, with no place to go and insufficient assets to move or purchase other housing.

Anyone who thinks the aftermath of Hurricane Katrina will be short-lived or benign is in fantasyland. We have 500,000

homeless people, maybe closer to a million, people with no way to return home for months on end. Note that most major

cities consider 10,000 homeless people an enormous challenge. Also note that those who fled are the ones with

the means to do so--those with cash, cars, nearby relatives, and so on. Those who remained behind did so because they

had no place else to go, and no money for a few weeks in a Houston hotel. They are effectively

homeless people, with no place to go and insufficient assets to move or purchase other housing.

When residents do finally return to their houses--those left standing--they will find the walls filled with bacteria, mold and Lord knows what else. That means to make the house habitable again, the flooring will have to be removed, the drywall will have to be torn down to the studs and the electrical wiring replaced--and this is a minimum. Given the termite damage that is prevalent in the area, the initial reconstruction may include most of the major framing, or at least those parts which were blown off with the roof. Meanwhile, nobody has a job to go to, either, because the city is basically uninhabitable. What are people going to live on? Unemployment? Emergency funds? For how long? Some optimists see all this construction work as a boon for the economy, but what about the people who will be displaced for months while they wrangle with FEMA loans to fund the rebuilding of their home, and then the difficulties of finding someone reputable to do the work? This isn't building 50,000 houses in a production setting, with economies of scale--this will be rebuilding each house, one at a time, with financing and other conditions unique to each dwelling. Just lining up the money, the crews, the materials and the infrastructure (power, water, housing for the workers, roadways, etc.) will take months. As for the oil industry--listen to all the experts talking about the fact there's no strategic reserve for natural gas. In other words, the shortage of natural gas will not be alleviated by tapping the crude oil Strategic Reserve. Meanwhile the pundits are cutting GDP for the Q4 by a tenth of a point. Who are they kidding? With nine refineries out of production, there will be a shortage of gasoline unless people begin conserving. But the behavior we're seeing is the opposite of conservation--people are "topping off" their gas tanks, sparking a negative feedback loop of a shortage created by fear of a shortage. As the Wall Street JOurnal noted on August 31: "If the U.S. auto fleet of 220 million vehicles went up to three-quarters of a tank -- or, say, 10 gallons more --it would be an additional 2.2 billion gallons of demand."Panicked drivers are already topping off their tanks and using credit cards to do so, suggesting the piper will be paid down the line. Meanwhile, the nation's savings rate sunk to its lowest ever last month, -0.6%, suggesting a consumer class that's finally tapped out. But wait, the pundits shout--the Fed will start lowering interest rates again, sparking another wave of mortgage re-financing, putting another hundred billion dollars of free money in people's pockets. But suppose inflation rises with higher fuel costs, as it is wont to do. Then the Fed won't be able to lower interest rates; rather, they'll have to keep raising rates to control inflation. And further suppose that the predictions calling for more hurricanes this year than last turn out to be true. Maybe this isn't the last hurricane to sweep over the Gulf Coast Oil Patch. Then what? We haven't seen the worst of this yet. September 1, 2005 The C.I.A., Threat Assessment and Oil: The Wisdom of Crowds? An article in the August 19, 2005 edition of the Wall Street Journal--well before Hurricane Katrina devastated Gulf Coast oil facilities--was titled Bets Emerge on $100-a-Barrel Oil: Open Call Options Reflect A Drastic Shift in Views On Outlook for Crude Prices. For those not familiar with options trading, "call options" are bets made that a commodity or stock will rise by some future date of your choice--it could be days, weeks, months or even years out. Alternatively, "put options" are bets that a commodity or stock will decline by a future date. What makes this article interesting is that it suggests some amoung the great unwashed masses of options traders-- typically a more savvy crowd than average stock market players--seem to sense that oil will continue rising: 'Investors are plunking down serious money on bets that oil prices will top $70 and $80 before the year is out. Those bets could point to higher prices. Adam Seiminski, an analyst at Deutsche Bank in New York, said the options market sees a one-in-three chance of oil prices moving above $75 before December, compared with a one-in-20 chance for the same scenario at the start of the year. "With the likelihood of a strong pickup in demand during the fourth quarter and geopolitical risks and weather events lingering, the chances of a move above $75 continue to be upgraded,' he wrote in a recent note." This is eerily reminiscent of the C.I.A.'s much-ridiculed "threat-matrix assessment" stock market program, Policy Analysis Market, which was cancelled in 2003 after much media ballyhoo. Here is a succinct description from nationmaster.com: "The Policy Analysis Market (PAM) was a proposed futures exchange developed by the United States' Defense Advanced Research Projects Agency and based on an idea first proposed by Net Exchange, a San Diego research firm specializing in the development of online markets.The ability of transparent, open markets or independent, decentralized groups of people to accurately assess threats, shortages and prices has been widely documented, most recently in the book The Wisdom of Crowds The sharp increase in oil futures call options suggests that $70 per barrel of crude oil is not the top price we will see this year. wessay noun, combination of 'web' and 'essay,' denoting a short essay which exploits the hyperlinks, interfaces and interactive capabilities of the World Wide Web; coined by Charles Hugh Smith on May 1, 2005, in Berkeley California. copyright © 2005 Charles Hugh Smith. All rights reserved in all media. |

||

|

|

home |