|

|

|

|||||

|

De Facto Socialism, 20 Million Vacant Houses and Squattertown, USA (June 30, 2009) Combine rising foreclosures and unemployment with de facto Federal ownership of millions of homes and you eventually get de facto socialized housing. Correspondent Richard Metzger and I have been discussing the consequences of rising foreclosures/unemployment and the de facto government ownership of millions of U.S. houses via Fannie Mae/Freddie Mac and direct ownership/control of banks. There are a lot of threads to pull together on this topic, so please bear with me as we set up the contexts. The party line on the housing bust is that "the market" will solve everything. Millions of foreclosed homes and apartment buildings will be sold to millions of buyers, who will fix them up and rent them out for tidy profits. One little problem with that rosy scenario: how can unemployed households pay rent? Like all the other "green shoots" scenarios, this one depends on semi-full employment to pan out. But rather than semi-full employment, we're facing a tidal wave of job losses which is far from being spent. Back in January, I posted this analysis which concluded job losses won't stop at today's 6.7 million but proceed on to 21 million or even 30 million: The End of (Paying) Work . Meanwhile, house prices continue their relentless decline. Home Prices Continued Their Decline in March (New York Times)

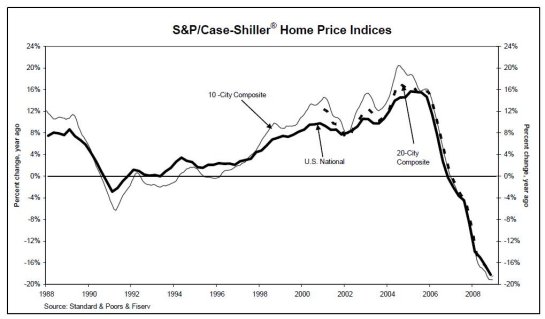

The S&P/Case-Shiller U.S. National Home Price Index which covers all nine U.S. census divisions recorded a 19.1% decline in the 1st quarter of 2009 versus the 1st quarter of 2008, the largest decline in the series 21-year history. The 10-City and 20-City Composites recorded annual declines of 18.6% and 18.7%, respectively. These are slight improvements from their returns reported for February. (from the report link in the NY Times story) Dumping properties has worked so far because the quantity dribbled onto the market by lenders has been modest and a pool of anxious-to-catch-the-bottom buyers had gathered. But once this shallow pool has been soaked up, then there is no long-term source of buyers.

Indeed, buyers bidding up prices now will regret their impatience in a year as prices continue their inexorable slide downward. Richard also sent me this story on shrinking Rust Belt cities bulldozing suburbs: US cities may have to be bulldozed in order to survive: Dozens of US cities may have entire neighbourhoods bulldozed as part of drastic "shrink to survive" proposals being considered by the Obama administration to tackle economic decline. While this is a somewhat sensationalist headline, it does raise a number of complex issues. 1. If an old house has been stripped or left vacant for long periods of time in locales with extreme summers and winters, then it may well be not worth fixing up. Its only value will be for scrap lumber, etc. 2. If a house is still habitable, but outside the shrinking radius of city services, does that matter to someone unable to pay rent on a nicer, more central house? Perhaps not. 3. If such free housing (abandoned, foreclosed and unsold, etc.) outside the shrinking city jurisdiction is occupied by informal residents, i.e. squatters, then what authority (if any) is in place? I have covered many troubling aspects of the housing bubble's inevitable deflation for years. Just for context, let's glance as the key points in the following stories: Can 4% of Homeowners Sink the Entire Market? (February 21, 2007)

If 4% of all American homeowners fall into foreclosure, could that "small number" cause a collapse in the entire housing market? The Pareto principle says: yes. How 4% of Mortgages Have Brought Down the Entire Market (August 21, 2007)

Back on February 21, 2007, I invoked The Pareto principle to suggest that a mere 4% of U.S. mortgages going bad could bring down the entire U.S. housing and mortgage markets. Seven months later, that call appears to be playing out in spades. Will Delinquencies Trigger a New American Revolution? (April 7, 2008)

Two years ago I predicted we'd soon see 5 million foreclosed/distressed homes, 5 million REO/investment/2nd homes languishing on the market and lender/thrift losses of $500 billion. I seem to have undershot the losses... Feedback Loop of Recession: Housing Bust, Debt and Layoffs (March 10, 2008) Could 50% of All Homes End Up in Foreclosure? (June 3, 2008)

Just how bad could the housing bust get? How about half of all urban homes being in foreclosure? As stunning or unbelievable as that may sound, it already happened once in the U.S., in the Great Depression, as documented in this report: Lessons from the Great Depression (St. Louis Federal Reserve). The Great Fall: How Suburbs De-gentrify to Ghettos (November 20, 2007)

A disturbing number of mainstream media stories are documenting the appearance of inner-city plagues such as gangs, drugs and graffiti in what were recently middle-class suburbs. The Company Store, Debt and Serfdom (October 24, 2008)

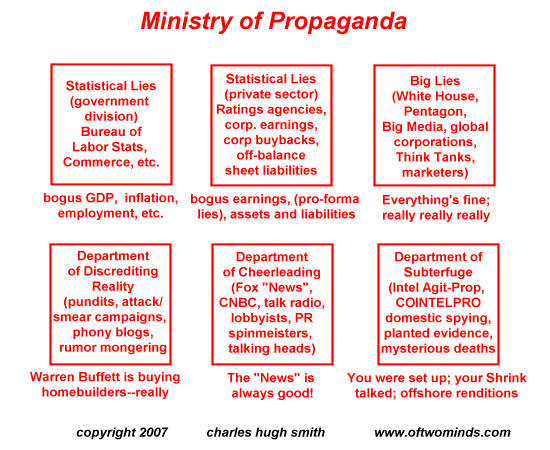

Most astonishingly, the Ministry of Propaganda has succeeded in diverting the nation's attention from the Company store/debt-serf realities to a bogus "debate" over "socialism" and "capitalism." As Michael Hudson has pointed out, the rentier class which owns the mortgages, loans and credit card debt is not capitalist at all; it is essentially medieval in structure. It takes no risks, creates no innovations, invests no capital in new enterprises or indeed, performs any classical capitalist functions at all.

It simply indebts the serfs, convinces them via doublespeak, propaganda and phony statistics that they are still gloriously "middle class" (that is, obscuring or reifying their true nature as mere miserable debt serfs) and then sits back and collects the interest and profits which the debt serfs will be struggling to pay until their last breath. This is the real context: a growing army of millions of unemployed, declining housing values and equity, a banking sector bloated with foreclosed/distressed houses which cannot be sold en masse and a Ministry of Propaganda in full-court press on reality. Unfortunately for Team Propaganda, Reality keeps sneaking through the full-court press and scoring easy dunks. (Shameless basketball analogy.) Let's return to the key issue of no jobs=no income=no ability to pay rent or mortgage. The entire U.S. system of unemployment insurance is based on the premise that no recession can last longer than six months--thus unemployment runs out after 26 weeks. Now, as dark storm clouds gather, this is being extended to 39 weeks--nine months. But few observers are pondering what happens next year when that nine months' of income expires and millions more lose their jobs. This raises a fundamental question which Richard poses thusly:

With the news of California's impending financial implosion, and the buzz about cutting off welfare, etc., in the state, I wonder where are they going to expect the tsunami of future homeless families to go? Under a bridge? Their front yards? The curb? It seems inevitable to me that as jobs vanish and incomes drop, rents will decline and vacancies will rise. This will trigger a wave of foreclosures of landlords who bought rental properties based on full occupancy and high (full employment) rents. As noted here before, that raise all sorts of other "interesting" issues; readers have recalled living in foreclosed apartment buildings during the late 1980s savings & loan bust and not knowing who even owned the building. There was thus no one to pay rent to. One key feature of the present is completely unprecedented in American history: the Federal government essentially owns millions of dwellings via its takeover of the GSEs Fannie Mae and Freddie Mac. These two lenders were once quasi-governmentally owned; now the quasi has been dropped. Fannie and Freddie own $5 trillion in mortgages; so when the owner walks away or defaults, guess who ends up owning the house? You and me: the taxpayers. Add in trillions of dollars of FHA and VA loans which are in default/distressed--also government guaranteed and thus ultimately government-owned--and direct Federal ownership of shares in major banks (which absorbed mortgage lenders like Countrywide, WAMU and Wachovia in Federally overseen shotgun marriages) and you end up with Federal ownership of a significant portion of the entire U.S. mortgage/housing stock. (Fannie and Freddie alone account for half of all outstanding mortgages.) Back to Richard's question: so exactly what will the U.S. do with 10 or even 20 million unemployed/no-income households? As noted above, there are already 20 million vacant dwellings. Even bulldozing 2 million of them won't change the big picture, and it certainly won't address the core issue of housing and feeding 10 million households with essentially zero prospects for formal employment in an economy burdened by staggering debt, losses and interest payments and a FIRE (finance, real estate and insurance) economy which has imploded, never to come back. The Ministry of Propaganda has an ironic task before it: it must continue its relentless cheerleading and its relentless attacks on "socialism" (whatever that means) even as the Federal government must somehow prepare to deal with 10 or 20 million homeless, broke households on a long-term basis. Even more ironically, that same Federal government now owns, via Federally backed mortgages, some 20 million dwellings. Now put all this together. Either we face up to 20 million households living in Squattertown, U.S.A. or the Federal government faces up to the obligations it now carries as reluctant owner of 20 million foreclosed/distressed/defaulted dwellings.

Is providing low-cost housing for 20 million homeless people "socialist"? If so, bring it

on, Ministry of Propaganda be damned.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, David Z. ($25), for your most-welcome generous contribution to this

site.

I am greatly honored by your support and readership.

Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright © 2009 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

|

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||