|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | ||

Writing/Film Dear Aspiring Writers: The Worst Advice You'll Ever Read A Literary Look at I-State Lines Spirited Away: Decay and Renewal An American Poem (Robinson Jeffers) Taoist Chinese Poems The Nelson Touch "It's all about oil, isn't it?" Kurosawa's High and Low A Bountiful Mutiny Howl's Moving Castle Thailand's Iron Ladies Trois Colours: Red The Thin Man: Thoroughly Modern Movies Why My Book Is Better Than the DaVinci Code Iranian Films: The Mirror Piratical Nonsense A Real Pirate Movie: Captain Blood 9 more in archive Recommended Books American Identity American Identity Literary Contest Winners, 2006 (fiction and essays) Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Your Tattoo in 50 Years The American House and Frank Lloyd Wright Cultural Commentaries On Hatred and Anti-Americanism Anti-Americanism Part 2 Anti-Americanism Part 3 French-Bashing Germany: We All Have Problems, But... Kroika! Chronicles This Blog Sells Out Doom and Gloom Sells The Kroika Mascot-"Auspicious Pet" Wal-Mart and Kroika Kroika and Starsbuck Take a Hit Kroika Ad 1 Kroika Ad 2 Kroika Ad 3 Kroika Ad 4 Kroika Makes Bid for Oreo (April 1) Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Corruption and Avian Flu: China's Dynamic Duo Exporting the Real Estate Bubble to China Is the Bloom Off the China Rose? China Irony: Steel, Marx & Capital Curing The U.S. and China's Dysfunctional Relationship China and U.S. Inflation Trade with China: Making Out Like a Bandit Whither China? Will the Housing Bust Take Down China? China's Dependence on Exports to U.S.; Is China About to Pop? 8 more Battle for the Soul of America Katrina, Vietnam, Iraq: National Purpose, National Sacrifice Is This a Nation at War? A Nation in Denial Why Is This Such a Tepid Time? That Price Isn't Cheap, It's Subsidized The Most Hated Company in America U.S. Fascists Seek Ban on Cancer Vaccine The Truth About Christmas American Dream or American Nightmare? 2006 Sea Change Obesity and Debt Immigration Ironies U.S. Healthcare: Working Toward a Real Solution A Drug Industry Running Amok Where There Is Ruin 10 more Financial Meltdown Watch What This Country Needs Is a... Good Recession Are We Entering the Next Age of Turmoil? Why Inflation Appears Low Doubling Down on 5-Card No-See-Um A Rickety Global House of Cards Are Japan and Germany Truly on the Mend? Unprecedented Risk 2 Could One Rogue Trader Bring Down the Market? Worried about Inflation? Stop Measuring It Economy Great? Bah, Humbug Huge Deficits and Huge Profits: Coincidence? Who's The Largest Exporter? Three Snapshots of the U.S. Economy Loaded for Bear Comparing Nasdaq to Depression-Era Dow Who's Buying Treasury Bonds? And Why? Derivatives: Wall Street Fiddles, Rome Smolders Financial Chickens Coming Home to Roost Is the Stock Market on the Same Planet as the Economy? The Housing-Recession-Oil-Healthcare Connection Could We Have Deflation and Inflation At the Same Time? What We Know, What We Can Safely Predict Bankruptcy U.S.A.: Medicare, Greed and Collapse Sucker's Rally A Whiff of Apocalypse Where There Is Ruin II: Social Security 31 more Planetary Meltdown Watch The Immensity of Global Warming Sun Sets on Skeptics of Global Warming Housing Bubble Watch Charting Unaffordability A Monster of a Housing Bubble A Coup de Grace to the Economy Hidden Costs of the Housing Bubble Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Housing Market Slips Toward Cliff Housing Market Demographics Housing: Catching the Falling Knife Five Stages of the Housing Bubble Derailing the Property Tax Gravy Train Bubbling Property Taxes Have You Checked Your Property Taxes Recently? Housing Bubble: Where's the Bottom? Housing Bubble: Bottom II The Housing - Inflation Connection The Coming Foreclosure Nightmare 1 How Many Foreclosures Will Hit the Market? Housing Wealth Effect Shifts Into Reverse Housing Bubble Bust Will Take Down the Global Economy The New Road to Serfdom: A Negative-Equity Mortgage The Housing-Savings-Recession Connection After the Bubble: How Low Will It Go? After the Bubble: Rents and Housing Values Why Post-Bubble Rents Matter After the Bubble: How Low Will We Go, Part II Housing: 10% Decline May Trigger Financial Ruin How to Buy a $450K Home for $750K Inflation and Housing: Calculating the Bust The Growing Financial Risks of the Housing Bubble Construction Defects: The Flood to Come? Construction Defects Part II Who Gets Hammered in the 2007 Housing Bust Real Estate Bust: The Exhaustion of Debt What Happens When Housing Employment Plummets? One More Hole in the Housing Bubble: Insurance Financial Kryptonite in a "Super-Strength" Housing Market Three Secrets to Unloading Property Today Welcome to Fantasyland: Housing's "Soft Landing" Why Is the Median House Price Still Rising? Why Median Prices Appear to be Rising? The Root Cause of the Housing Bubble Housing Dominoes Fall Twilight for Exurbia? Phase Transitions, Symmetry and Post-Bubble Declines 10 more Oil/Energy Crises Whither Oil? How much Is a Gallon of Gas Worth? The End of Cheap Oil Natural Gas, Naturally High Arab Oil Money and U.S. Treasuries: Quid Pro Quo? The C.I.A., Oil and the Wisdom of Crowds The Flutter of a Butterfly's Wings? A One-Two Punch to a Glass Jaw Running Out Of Oil vs. Running Out of Cheap Oil 2 more Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds Geezer Rock Overload Paying for Web Content In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono Happiness for Sale: Jank Coffee Ten Guaranteed Predictions for 2010 Why My Book Is Better Than the DaVinci Code My Brand Management Stinks Design Follies The New Jank Coffee Shop Jank Coffee, Upscale Tropic Style One-Word Titles Complacency Nostalgia Lifespans Praxis Keys to Affordable Housing U.S. Conservation & China Steve Toma, Me & Skil 77s: 30 years of Labor Real Science in the Bolivian Forest Deforestation and Sustainable Forestry The Solar Economy (book) The Problem with Techno-Fixes I Love Technology, I Hate Technology How To Blow off Web Ads and More 2 more Health, Wealth & Demographics Beauty of the Augmented (Korean) Kind Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Is Obesity an Inflammatory Response? Demographics & National Bankruptcy The Decline of Europe: A Demographic Done Deal? Are the Risks of Obesity Overstated? Healthcare: Unaffordable Everywhere Medication Nation The New Disease We Just Know You've Got Can You Can Tell Which Pill Is Fake? Bankruptcy U.S.A.: Medicare, Greed and Collapse The 10 Secrets to Permanent Weight Loss 5 more Landscapes Selling the Landscape The Downside of Density Building Heights and Arboral Roots Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Waimea Canyon, Yosemite, Camping & Pancakes Nourishment The French Village Bakery Ideas What Is Happiness? Our Education System: a Factory Metaphor? Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi Splogs, Blogs and "News" "There is no alternative to being yourself" Is There a Cycle to War? Leisure, Time and Valentines Is the Web a Giant Copy Machine? Science Matters Anti-Missile Defense: Boost Phase Vulnerability History The Strolling Bones: Rock of Ages Bad Karma: Election Fraud 1960 Hiroshima: First Use All the Tea in China, All the Ginseng in America Friday Quiz Pet Obesity The Origins of Carbonara Organic Farms Oil and Renewable Energy Human Diseases Wine and Alzheimers Biggest Consumers of Chocolate 7 more Essential Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So Fewer: How the New Demography of Depopulation Will Shape Our Future The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal The Future of Life Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies The Solar Economy: Renewable Energy for a Sustainable Global Future The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Feeling Good: The New Mood Therapy Revised and Updated Recommended Books More book reviews Archives: weblog August 2006 weblog July 2006 weblog June 2006 weblog May 2006 weblog April 2006 weblog March 2006 weblog February 2006 weblog January 2006 weblog December 2005 weblog November 2005 weblog October 2005 weblog September 2005 weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

|

September 30, 2006 Haiku Fun  Another good one is The Spring of My Life: And Selected Haiku (Issa) Since I studied Japanese language, geography, culture and literature at the University of Hawaii, and majored in Comparative Philosophy (which means classes in both Western and Eastern philosophy), I think I am qualified to state the obvious that the Japanese language is structurally dissimilar to English. Hence, all translation is a priori interpretive.  Sam Hamill: Don't kill that poor fly! He cowers, wringing his hands for mercy Robert Hass: Don't kill that fly! Look--it's wringing its hands, wringing its feet. And here's the original Japanese: Yare utsu na hae ga te wo suri ashi wo suru Here's several more wonderful little poems (talk about bite-sized; eat your hearts out, Longfellow and Tennyson!) Buson: I go, you stay; two autumns That snail-- one long horn, one short, what's on his mind? Issa: Don't worry, spiders I keep house casually Climb Mount Fuji, O snail, but slowly, slowly That gorgeous kite rising from the beggar's shack In spring rain a pretty girl yawning When I finally die, I hope you'll tend my grave, little grasshopper! The blossoming plum! Today all the fires of Hell remain empty Wonderful stuff, those last two; so few words, so full of wisdom. Just for laughs I composed this haiku about the stock market. Recall that the classic haiku structure is three lines, of 5-7-5 syllables. The Dow and Nasdaq plump birds, ripe for the kitchen what a meal they'll make! The best haiku from a reader this weekend wins a gloriously free copy of my novel I-State Lines. Could be fun, give it a try! September 29, 2006 Bonds and Gold: They Can't Both Be Right Bonds and gold are both rising, which is peculiar indeed. Why? Because they can't both be right. Bonds rise when inflation is low or declining and interest rates are declining, while gold rises when inflation rears its head. So which is it? Is inflation "under control" and bond rates set to drop? If so, why is gold rising?

Gold is also considered a hedge against a declining dollar, and it is no coincidence that the dollar declined in the period of stagflation, rising interest rates and plummeting bond values. In the "great Bull market" of 1982 - 2000, the dollar was strong while interest rates fell and inflation remained low, pushing gold down to multi-year lows well under $300 an ounce.  Those trumpeting a future of deflation or dropping prices anticipate the Fed cutting rates

and inflation dropping to zero or even below. If this is right, who would want to own gold?

No one. Gold is a non-productive asset, and in a deflationary environment then cash is

what is rising in value, not gold. So why is gold rising? Gold rises in the

expectation that inflation will rise and the dollar will weaken, both conditons which will

cause interest rates to rise and bonds to plummet in value.

Those trumpeting a future of deflation or dropping prices anticipate the Fed cutting rates

and inflation dropping to zero or even below. If this is right, who would want to own gold?

No one. Gold is a non-productive asset, and in a deflationary environment then cash is

what is rising in value, not gold. So why is gold rising? Gold rises in the

expectation that inflation will rise and the dollar will weaken, both conditons which will

cause interest rates to rise and bonds to plummet in value.

The cycles of bonds, stocks and gold are long indeed. Bond rates tend to rise and fall in

cycles of 16 - 22 years, so why would they suddenly reverse after a mere 3 years? As this

chart reveals, gold has been in a multi-year uptrend. If inflation is about to decline to

zero and bond rates set to drop, why would gold continue rising?

The cycles of bonds, stocks and gold are long indeed. Bond rates tend to rise and fall in

cycles of 16 - 22 years, so why would they suddenly reverse after a mere 3 years? As this

chart reveals, gold has been in a multi-year uptrend. If inflation is about to decline to

zero and bond rates set to drop, why would gold continue rising?

Both sides can't be right. Either interest and bond rates are in a new uptrend which will last for 12-20 more years, with gold rising as the face value (coupon value) of bonds drop, or the 20-year cycles are broken and bond yields will fall back to near zero as in Japan's "lost decade" of the 90s. In such a deflationary environment, gold will drop in value as demand for an inflation and dollar hedge dries up. Which scenario is right? I'll take history's cycles over a "low-interest rates forever" optimism, but take your pick. Bonds and gold are a see-saw--when one is rising the other is declining--and unless history is overthrown, they cannot sustain parallel uptrends for long. September 28, 2006 Cross Feedback Between the Stock and Housing Markets  In his classic text

Irrational Exuberance

In his classic text

Irrational Exuberance

Internationally, home price booms show some tendency to peak a couple of years after stock market booms. This raises the possibility that there is sometimes cross feedback, that is, feedback from one market to the other, between the stock market and the housing market.In other words, a stock market boom generates a "wealth effect" which crosses over to the housing market. Fair enough. But what about a boom which crashes back to earth, as the NASDAQ market did in 2000? Shiller's questionnaire-based research found that:

More than ten times as many (recent home buyers) said that the stock market encouraged them than said it discouraged them.  This cross feedback may seem blindingly obvious, but it does lead us to ask: what

cross feedback might occur if both the stock and housing market roll over? Might

the dropping of prices in both markets start feeding back to each other? Where will people

put their money as both their stock and housing investments falter? Could the recent rise

of the bond market presage a flight to the apparent safety of bonds?

This cross feedback may seem blindingly obvious, but it does lead us to ask: what

cross feedback might occur if both the stock and housing market roll over? Might

the dropping of prices in both markets start feeding back to each other? Where will people

put their money as both their stock and housing investments falter? Could the recent rise

of the bond market presage a flight to the apparent safety of bonds?

The chattering classes are nearly unanimous in their expectation of deflation and a round of Fed rate cuts. Nice, but what if they're wrong? What if the inflation in non-discretionary spending and taxes which I have often described here (as opposed to the deflation found in discretionary items like restaurant meals) is embedded in the economy, merely masked by phony-baloney statistics which trumpet "inflation is dead"? What if the chart above reflects a reality which has been discounted, i.e. inflation is in a multi-year uptrend regardless of discretionary spending deflation? In other words: what if the Fed can't cut rates, as universally anticipated? Then what happens to bonds? They drop like stocks and housing. This is the cross feedback trifecta no one anticipates--no place to hide except maybe--maybe--gold and silver. September 27, 2006 Facing Foreclosure? Consider "Wheel Estate"  Reader Jim Twamley sent me the following commentary on how RVs/mobile homes could be

an excellent housing choice for those who lose their homes to ARM re-sets or other

financial setbacks. I have already addressed how campers and small RVs are the housing

choice for many homeless people--

The Mobile Homeless. The entry contains a number of media stories which describe

people on limited incomes in the S.F. Bay Area who survive by living in campers.

Reader Jim Twamley sent me the following commentary on how RVs/mobile homes could be

an excellent housing choice for those who lose their homes to ARM re-sets or other

financial setbacks. I have already addressed how campers and small RVs are the housing

choice for many homeless people--

The Mobile Homeless. The entry contains a number of media stories which describe

people on limited incomes in the S.F. Bay Area who survive by living in campers.

Foreseeing the same exodus from unaffordable houses that Jim anticipates, I said: Cities would do well to begin setting aside properly maintained areas for the mobile homeless, whose numbers are sure to increase.While some families with children might home-school, as Jim suggests, others might prefer a semi-permanent home so their kids can attend a public school. If urban-core cities were willing to serve residents who were no longer homeowners, they would set up RV facilities with basic utilities, and charge monthly fees like private RV camps to provide security. Such fees would certainly be less than the rent on a one-bedroom apartment in the Bay Area, which is around $1,000. But enough of my municipal daydreams--on to Jim's essay: Wheel EstateThank you, Jim, for a thought-provoking description of a practical alternative to renting a house or apartment. The community which Jim so ably describes sure sounds like more fun than the average neighborhood in exurbia. Note: Sometime yesterday the 300,000th visitor of the year stopped by this humble outpost of the World Wide Web...thank you, one and all, for your readership. You are the source of so much of the information and commentary which finds expression here. September 26, 2006 What's Up (Down) with the Price of Oil? In the September 14 entry, "Could the Price of Oil Be Manipulated?" I made this comment: If I were in a position to manipulate the oil futures market (oh how I wish!), I would engineer the occasional free-fall in order to panic the herd into selling. As the price fell to absurd levels in the ensuing rush to the exits, I would buy futures on the cheap and then let actual demand drive the price back up, thereby reaping vast profits once the price returned to its "market" level.

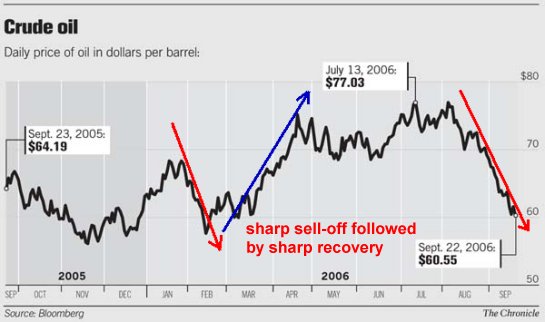

What's interesting about oil's near free-fall from $78 to $60 in a matter of weeks is: this is exactly how it would respond had a concerted effort been made to drive down the price. Now maybe this is just "market forces at work," but the first thing I would do to set up a free-fall is flood the media with stories about how the world is awash in oil, Peak Oil is bogus, we've got oil to last for 100 years, etc. etc. And here we have Exxon and Saudi Arabia both saying exactly that: Producers Move to Debunk Gloomy 'Peak Oil' Forecasts: Yesterday, Abdallah S. Jum'ah, chief executive of Saudi Arabian state-owned Saudi Aramco, the world's largest oil company by production, argued during a speech in Vienna that the world has more than a century's worth of crude left at current production rates. His talk followed similar remarks by a senior Exxon executive this week. Spokesmen for Exxon and Aramco said they aren't coordinating their remarks.To quote the Mogambo Guru: hahahahahahahahahaha! It's just coincidence that Exxon and Saudi Arabia are talking up the oil surplus at the same time. (Exxon's) Mr. Nolan cited a U.S. Geological Survey estimate of more than three trillion barrels of conventional recoverable oil resources, of which one trillion barrels has been produced. Conservative estimates of heavy-oil and shale-oil resources push the total to four trillion barrels, while a 10% increase in recoverability will deliver an extra 800 billion barrels, Mr. Nolan said.Nice, but the shills forgot to mention that the easy trillion--the stuff which flows out under pressure, the light sweet crude which costs $1 to get out of the ground--is nearly gone. The other 3 trillion are increasingly expensive to pump out: they're deep, sludgy, mixed with sand, etc. etc. It costs upwards of $40 a barrel to extract and refine this "limitless" oil. To reiterate a point made here repeatedly: oil isn't gone, but the cheap oil is. For a detailed debunking of the Saudi claims of unlimited reserves, please read  Twilight in the Desert: The Coming Saudi Oil Shock and the World Economy As for burning up that next trillion barrels in a decade or two, plus a veritable mountain of high-sulfur coal--well, maybe when our Leadership stops "debunking" global warming and starts building a seawall around Manhattan and Washington D.C., then they'll finally "get it" that even if the next trillion barrels will be cheap (it won't), we can't burn it anyway without creating a runaway warming cycle without precedent. Now that we've created a media stupor of "oil surplus," next we sell off futures, triggering a stampede in the hedge funds. They're skittish little beggars, those hedgies, because they need to get in and get out very quick-like to make their enormous fees and still produce some gains for their very rich and very greedy clients. OK, done. The stampede has exited oil, and now we plant stories in the media about how all the "smart money" is exiting energy and entering tech. (You've noticed those stories, haven't you? That's what good PR is all about.) Here's one report on the "exit, stage right" by speculators: Oil's slippery slope: Moves by monied speculators bear heavily on prices The movement of all that speculative cash isn't the only reason energy commodities are tumbling. But analysts say the behavior of big market speculators has amplified and speeded up the drop. The Commodity Futures Trading Commission keeps track of whether traders are buying or selling futures, betting that prices will rise or fall. Among speculative investors, the number of bets on rising prices has dropped by more than 50 percent since mid-August, said David Kirsch, an oil analyst at the PFC Energy consulting firm.Voila. Now that we've engineered a free-fall to $60, we load up on now-cheap futures for December or beyond. Futures which we will sell to the hedgies for enormous profits when oil "somehow" becomes scarce again and the price rises back to $70 and above. It's like shooting fish in a barrel, isn't it? Now let's look at a chart of an oil ETF (exchange traded fund), the XLE, which is a collection of oil stocks:

Oil Bears would point to the "double top" and the apparent break in the long uptrend as evidence oil has "topped out" in the big picture, and is on its way to $50 or lower. Maybe. But it can also be argued that oil has just dropped back to a level of massive support before it makes another run at breaking through resistance. The technical indicators of MACD and the stochastic are both bottoming, suggesting that this free-fall has run its course and the oil market is setting up for a rebound--which as the first chart shows, tend to form a mirror-image of the drop. In other words, a big sharp decline is followed by a big sharp recovery. That's how the big money is made, Ladies and Gentlemen. So watch the media for stories of "risks to oil supply" and the like. (What happened to the oil glut? Huh? What oil glut?) Those scary stories of possible shortages will "magically" be followed by actual declines in supply which will trigger "market forces" (so benign sounding!) and the price of oil will jump as rapidly as it declined. So no, the oil market isn't manipulated. Ignore the man behind the curtain. Move along, we'll keep you posted on how much you should pay for gasoline. The price will rise, gosh, right after the elections. Guess I shouldn't have revealed that, huh? September 25, 2006 The Rot at the Corporate Center, Part II Friday's entry on the book Bait And Switch I have been a design engineer for about 15 years, I believe that I am a pretty good engineer. In 2000 I decided to change jobs. Since then, I was laid off and almost laid off. I know a platoon of engineers that have been forced to look for work since 2000 for the sake of corporate profits and shareholder value.Since we have many friends in Japan, China, Korea and Thailand, I can report that working conditions are far from ideal in much of Asia; employees are expected to work what are fundamentally inhuman hours (sometimes until midnight, with work starting early the next morning, etc.) and rewards such as stock options and huge bonuses simply don't exist. On the other hand, the Korean and Japanese global companies do maintain a very long-term perspective, and they have (and will) sacrifice profits for years in order to take market share or establish dominance in a field (tiny motors, robots, etc. etc.) If you lay off employees with little regard for the morale of the survivors, or for the depth of the talent pool you have just thrown away, then perhaps you have also weakened your long-term competitiveness or even survival as a global company. I think it is also fair to say that the "shareholders" of the top U.S. corporations are no longer stakeholders in the companies' long-term success. They are massive investment and hedge funds whuch may hold shares of a company for a matter of hours, days or weeks. The rising turnover rate of the major stock exchanges suggests that on average "shareholders" only hold shares of a company for a few months. What these speculators (let's be honest, they are not investors) demand of management is not dominance in a field or superior R&D with an eye on profits five or ten years' hence but a catalyst which will drive the stock up 15% by next quarter so they can sell out and move their billions into some new quick-turnover deal. This "shareholder" adds absolutely nothing to the company nor to its customers, employees or indeed, profitability in the long run. For another view of Ehrenreich's work, we turn to correspondent Michael Goodfellow: It's been years since I read Nickel and Dimed, but I remember thinking that her whole problem was not salary or working conditions, but the rent she pays. Without that high rent, her budget would have been fine (except for health insurance, which is another issue.)Thank you, M.P. and Michael, for your comments on this critically important topic. September 23, 2006 The Rot at the Center, Middle Kingdom-Style The rot at the center is not limited to the U.S., as this Shanghai-based blog reveals.

We Filled Our Lives But Lost Our Souls: First off, lemme just say it's damn hard to keep one's soul in contemporary China. Everytime I went back to Shanghai, it felt very different to me. In recent years, increasingly, I felt an overwhelming sense of materialism. Adding to that is tremendous peer pressure and the need to 'keep up with the Jonese.' What others have I have to have it, too. What others do I have to do it better. That's painful. By going with the flow we essentially give up our own choices, ideals, and individuality. Or, in other words, our souls.  This is not to say that life isn't exciting and rewarding in China. But the

financial pressures sound eerily like those in the U.S. cities like New York and

San Francisco. Here is an excellent entry on wages and condominium costs in Shanghai:

Going Back to China?. The entry is a response to a Chinese-born

person wondering if he/she should return to China from the U.S. Here are a few data

points from the post:

This is not to say that life isn't exciting and rewarding in China. But the

financial pressures sound eerily like those in the U.S. cities like New York and

San Francisco. Here is an excellent entry on wages and condominium costs in Shanghai:

Going Back to China?. The entry is a response to a Chinese-born

person wondering if he/she should return to China from the U.S. Here are a few data

points from the post:

In IT industry, undergraduate students have to work hard to earn 36,000 RMB per year.RMB denotes the Chinese currency, the renminbi, unofficially known as the yuan. It is currently pegged to the U.S. dollar at about 8 to 1, so one yuan is worth about 12 cents. Thus the average white-collar worker's annual salary of 36-38,000 RMB is about $4,000. One square meter is roughly 10 square feet, so a 100 sq. meter apartment is about 1,000 square feet. Using the numbers given above, a 1,000 square foot flat in Shanghai is about 700,000 to 1,000,000 RMB, or roughly 20 times the average white-collar annual salary. Here in the Bay Area, that's roughly analogous to a wage of $40,000 a year and a flat which costs $800,000--in other words, San Francisco or Manhattan. (Note: an IT professional in San Francisco might earn $80,000, of course, reducing the salary-to-house ratio to a mere 10 to 1. In the recent past, the average in the U.S. was 4 to 1.) So an IT professional in Shanghai earns about $4,000 a year, and a decent condo costs $100,000 or more. (Non-professional workers earn a mere third of the professional's pay.) Note that these prices are from a few years ago, and with the property bubble very much in play, the current costs of a flat in Shanghai may well be 10%-20% higher than those stated here. Is there any doubt that housing is unaffordable in China's biggest cities? When an flat costs 20 times a high-end IT professionals' salary, it seems obvious that China is also in the midst of a stunningly inflated property bubble. To summarize: first you lose your soul trying to earn enough to buy a home, and then when the bubble bursts you lose the home, too. What happens to those who've mortgaged their souls along with their property? The home can be replaced at some point down the line, but the soul... perhaps not so easily. September 22, 2006 The Rot at the Corporate Center  Just as Ms. Ehrenreich gained first-hand experience of low-wage services jobs in America by seeking employment in that sector, as recounted in her book Nickel and Dimed: On (Not) Getting By in America Given her education and experience, and the fact that she devoted herself entirely to the job search, she had every expectation of landing a job in a few months. The results were not what she expected. The book documents her complete failure, and that of the other unemployed white-collar types who she spent months networking with in an endless string of "executive" seminars, "networking" mixers, church "networking" functions, etc. Not one of her wide circle of contacts scored a job equivalent to the one which they'd lost. The net result, Ehrenreich concludes, is that as Corporate America downsizes--partly due to the extreme pressures ccreated by rising medical costs for their employees--the millions of people off-loaded at the unemployment office end up taking low-wage jobs in the service sector or taking a chance on starting their own businesses. She believes one of the fixes is--no surprise here for readers of this blog--a national healthcare plan which relieves companies from the burden of paying the ever-spiraling skyward costs of employees' healthcare. OK, cue the chorus of "sour grapes;" everyone she met in six months was a loser, right? It's their own fault, etc. Believe that old-time religion if you want, but you might want to read the book before forming an opinion. Consider this factoid quoted in the book's afterword: New research suggests that 17 percent of jobs that do not require a college degree are currently filled by college graduates, for a total of about seven million under-employed people. According to the Bureau of Labor Statistics, of the 25 fastest growing jobs for 2006, only five required a college degree at all.

Meanwhile, corporate profits have reached postwar highs both in real dollars and as a percentage of GDP: When do workers get their share? by the Economic Policy Institute: Most of this growth in total labor compensation has been accounted for by rising non-wage payments, like health care and pension benefits. Rapidly rising health care costs and pension funding requirements imply that these higher benefit payments are not translating into increased living standards for workers, but are rather just covering the higher costs of health care and pension funding. Growth in total wage and salary income, the primary source of take-home pay for workers, has actually been negative for private-sector workers: -0.6%, versus the 7.2% gain that is the average increase in private wage and salary income at this point in a recovery.Forget Mideast: Profits Are the Problem (from the Wall Street Journal) Standard & Poor's also expects earnings to continue growing at a double-digit pace in the second half of the year. If those forecasts hold, it would make for the longest stretch of double-digit earnings gains since 1950, surpassing a long string of gains in the early 1990s.From 2001 to the fourth quarter of 2005, corporate profits as a percentage of United States G.D.P. rose significantly, to 11.6 percent from about 7 percent (New York Times)  Notes on the Latest Federal Budget Estimates:

Notes on the Latest Federal Budget Estimates:

In the first quarter of calendar 2006, corporate profits hit a post World War II high of 12.7 percent of the GDP. The administration projects that profits will be 12.2 percent of GDP for the full year.I would also like to share a more personal report from reader Steve S. who recently sent in the following comments in response to a chart I'd posted here which showed that only 20% of Americans 60 and older were working. Steve highlighted some possible reasons for this low number, and I want to reprint his comments in light of the above data points on corporate profits: My wife and I have been fiscally conservative, but politically, environmentally, educationally ... liberal. I see absolutely no conflict. Environmental health, challenging and open minds, Culture, our children's interest in life, etc. are important. Driving a BMW or SUV, living in a McMansion, eating out every night at a chain restaurant, dressing in GAP, Old Navy, etc. do not add anything to the appreciation of what was the variety of the world. We have both recently quit our jobs. We are part of your statistics - older people not working past 60. We ARE NOT living off HEW. (Federal Dept. of Health Education and Welfare, now known as the Department of Health and Human Services--HHS).Well-said, Steve. Thank you for your account of your own experience, and how these conditions may be fueling the exodus of 60-and-over workers. September 21, 2006 Second Home Madness

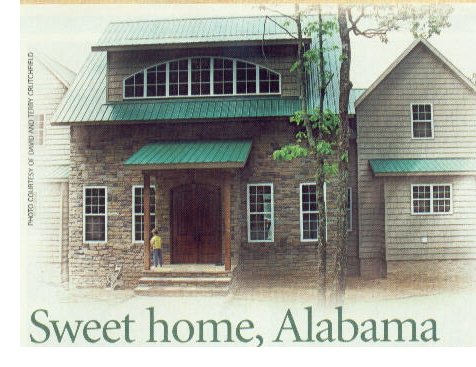

Consider this new vacation home in Smith Lake, Alabama, which was featured in the latest edition of the Costco Connection magazine. It has seven bedrooms. From Costco's point of view, this is a wonderful opportunity to fill a gigantic house with cheaply made furniture and "home entertainment" electronics from Costco. What can we divine from such a second home as this? 1) What is the difference between this "vacation/second" home and a primary residence? None. Gone, it seems, are the days when a second home on the lake meant a small, inexpensive cabin; now, it is a full-blown McMansion with 7 bedrooms and Lord only knows how many bathrooms (Five? Six? Eight?). 2) The housing bubble/boom is not limited to "hot spots" like Florida, San Francisco, Phoenix or Boston. Pundits claim that there is no national real estate market, but what does a 7-bedroom second home in Alabama say about real estate locally and nationally? It would be rather absurd to claim this kind of home is unique to Alabama. Perhaps the truth is the housing boom/bubble is national in scope, as evidenced by 7-bedroom second homes being built in supposedly non-bubble states like Alabama. 3) What might the carrying costs of this second home be? How much is the mortgage? What are the property taxes of such a large and obviously expensive home? How much will it cost to heat and cool such a vast interior expanse? A small cabin was inexpensive to maintain, and low in value; the same cannot be said of this monstrosity. A small cabin bespoke a modest getaway; a 7-bedroom manse communicates a pretension to opulence and prestige even away from home. 4) While this McMansion might be well-built with quality materials, it might also be a typical McMansion constructed largely of wood chips, glue, various veneers and drywall. Lest you think I exaggerate, go visit the construction site of a standard bloated McMansion like this: the subfloor, wall and roof sheathing are all OSB (oriented strandboard) or equivalent "engineered wood product"; the siding is vinyl (PVC), painted pressed-wood, or laminate (a thin veneer of real wood over wood chips and glue); the "hardwood" flooring is a veneer; the cabinetry is particle board with "hardwood" doors, the "stone" is either colored cement or glued-on veneer, and so on. This house of glue and wood chips is then finished off with granite counters and a few other ersatz "luxury touches" to provide a sheen of quality over the particle board and drywall. Might the ersatz nature of McMansions' actual quality be a metaphor for the "quality" of the entire housing boom/bubble? The "glue" which holds the entire shoddy structure together is cheap and easy money, and as long as that spigot flows freely, then 7-bedroom "vacation homes" will continue to be built (and filled with cheap imported furniture). But if--and it is a big if, for perhaps the Fed and the bond market can manage to keep money cheap and easy for decades to come--if the money spigot should ever close, then owners of 7-bedroom McMansions throughout the country may find their real estate wealth has the same durability of particle board left exposed to the weather. September 20, 2006 The Travails of an Unknown Author  One of my favorite scenes in the film

The Snows of Kilimanjaro

One of my favorite scenes in the film

The Snows of KilimanjaroIn the real world--more like the overdue utility bill. Yes, some books sell 4 million copies or something, but for most of us unknown authors, the sales are a few hundred at best. The answer, we're told, is to load the trunk of our car with books and hit the road, stopping at every bookstore and/or college campus to hawk our product, much like the snake-oil salesman of old. (Or "Juice of the cactii," take your pick.) Alas, not all of us have the iron (or is it titanium?) disposition needed to sell snake-oil or novels from the back of a beaten-down Impala with no rear shocks (books weigh a lot). And there is no guarantee that anyone will show up for your reading or book signing, either. My own experience was this: five people showed, plus the owners' two dogs (sleeping under the desk). Several of the human attendees were friends of the owners, and though we sold five books, I suspect pity for the poor wretched author was the primary motivation. Let's face it --even I wouldn't show up for my own reading. People understandably want celebrity and glamour at book readings, and (see photo above left) they're not gonna get either at my readings. And so the unknown author is straddled on the horns of an uncomfortable dilemma--how do you become well-known enough that folks want to show up for your readings? Doing readings to empty chairs is not the answer. My publisher suggested aligning myself romantically with Paris Hilton or Jennifer Lopez. Great idea, but if I could swing that, I wouldn't need to sell any copies of the book--I could just collect the loose money in their sofa cushions and retire in style. In other words, one might as well hope that Steven Spielberg happens upon one's forlornly unknown novel and snaps up the film rights for a cool half-million. In other words--dream on, Baby! The math is not promising. Five thousand new novels published every year, thousands of PR people shoving out reams of promo material to every bookstore and newspaper editor in the nation, and the 5,000 Harry Streets all hoping for love, cash and redemption from the sale of their precious novel. It's a shopworn premise, starving unknown strikes it big, but it happens just often enough to inspire the 100,000 novelists who get whittled down to 5,000 a year. I speak as one, and I concur with my publisher, a wise old author of many books, when he told me, "It's God's will, or destiny, call it what you want." In other words, sorta like the lottery or striking it rich in the stock market. If this made you smile, so will the book. If you feel some amusement, or generosity, or some stray emotion which loosens your purse strings, then by all means buy my novel I-State Lines from The Kaleidoscope or from Amazon.com September 19, 2006 Huzzah for Iowa  I just returned from a book reading (for my novel

I just returned from a book reading (for my novel I-State Lines In northern Iowa, and I had a great time. As I am still working in film, I don't have any photos of my own to post just yet (this one is a USDA stock photo of cornfields in Spring). Now, the corn and soybeans are withered and dry, and will soon be harvested. It's not just happenstance that I went to Iowa for a book signing, for Iowa plays an essential role in my novel. The second paragraph reads: Take our bus ride from Kansas City. It should have been the snooziest cruise in the universe to get to Alex's uncle's farm in Liberty. But no, everyone else on the bus makes it to Iowa except us. Why? Alex.In the book, Iowa represents all that is authentic in America--after all, growing food is the one endeavor we literally cannot live without--reflecting my character Daz's appreciation of physical labor, authenticity and agricultural landscapes. Like any clear-sighted, idealistic youth, he has only scorn for the phoniness of status symbols and pretension, the seen-at-the-right-party facelift Mercedes namebrand media-marketed America which dominates our sadly pathetic culture. So while it is chance that a bookseller in Northern Iowa is a big fan of the novel (The Kaleidoscope in Hampton, Iowa), it is not chance that Daz and Alex end up in Iowa. Although Iowa doesn't often appear on any "must-see" tourist destination lists, a leisurely drive through the state offers the rich rewards of camera-ready landscapes and small town charms, and a very friendly population. I made friends with a variety of folks in just a few days, and was welcomed in a way which I suspect is practically forgotten in most of urban and suburban America--where far too many people don't even know their neighbors. Iowa has 99 counties, and each one has a county seat--in most rural areas, usually the largest town in the county. Many of these hold a variety of charms for any visitor: a nobly designed and built courthouse, Victorian-era homes, small colleges, and in the case of Hampton, a viable, walkable and fun downtown. Lest I sound like an enamoured city dweller--I visited in a very pleasant time of year. The locals told me that winters are brutal, as the wind--which always blows regardless of season-- cuts right to the bone. Summers are the usual Midwest serving of hot and muggy, with occasional helpings of unbearable. As for small towns--yes, there are limitations which I know well, having spent many years in small towns in both California and Hawaii. I should also mention that when my Dad was working as a regional sales manager for Monkey Wards back in the late 60s, my brother and I accompanied him every summer as he criss-crossed the midwest and west visiting Ward's stores (or Weird's, as he called them. Yeah, corporate America sucked even then, and of course it's deteriorated since to levels of degradation and insecurity which were unimaginable just a few decades ago. But that's another entry). As a result, the midwest is not unknown territory to me. But for an urban dweller, it's nice not to worry about being shot by accident (or on purpose, take your pick, we have hundreds of victims in each category), and for suburban commuters, it's a pleasant change to actually know your fellow residents in some other context that complaints from the gated-community watchdogs or faceless, nameless encounters with people who live a stone's throw away but whom you've never actually met. There are hundreds of wonderful, charming small towns in the U.S., and here are two to visit in northern Iowa: Hampton Forest City And a site on one of the two products growing virtually everywhere: Iowa Corn facts. If you get a chance, go to Iowa and see the countryside for yourself. It is not "fly-over country," it's "get off the interstate and drive through country." September 15, 2006 The American Identity Literary Contest Awards for 2006 and Two Tales of Personal Risk Assessment. . . and a motorcycle story  Sensing a lack of literary focus on multicultural/multi-ethnic college-age writers,

I launched the American Identity Literary Contest this year, and received numerous wonderful

entries from all over the nation. Here are the winning entries in fiction and non-fiction.

To read all the winning entries, please visit

American Identity Literary Contest Winners, 2006.

Sensing a lack of literary focus on multicultural/multi-ethnic college-age writers,

I launched the American Identity Literary Contest this year, and received numerous wonderful

entries from all over the nation. Here are the winning entries in fiction and non-fiction.

To read all the winning entries, please visit

American Identity Literary Contest Winners, 2006.

(A note on the photos: these scenes of the great American landscape seem appropriate to both the honoring of talented young American writers and the recognition that Nature can be dangerous to the unprepared or over-confident.) First prize in Fiction: Graduation, 2006

First prize in Non-Fiction/Essay: BlendingCheck out American Identity Literary Contest Winners, 2006 to read the other six stories and essays which earned prizes. I received a number of responses to the September 12 entry "On Personal Risk Assessment;" here are two I want to share with you: From Reader H.I.: I have a story of my own that shows even those of us who are extremely confident in the water sometimes fall prey to false confidence.  From a U.K. reader:

From a U.K. reader:

At the age of 50 or so I found myself climbing a small mountain in damp, slightly misty weather. It is made of large slabs of slate, which had a hint of silpperiness. I had not taken this particular route before. It goes along a sharp ridge, with a drop on one side to a little lake a thousand or so feet down, and a drop of a similar sort into a gully. The top of the ridge is probably 20 yards wide, but its much wider on the approach. The views are magnificent.Reader A.L. recommended this account of motorcycle racing, which is fun for any motorbike fan but also extremely sad when it gets to the list of all the author's buddies who have been killed: Scenes From Behind The Bamboo Screen Take Two: Learning to Go Fast by Nick Voge. Thank you, readers, for sharing these sobering accounts. As I will be doing a book reading or two for my novel this weekend, there won't be a Saturday or Monday entry. September 14, 2006 Could The Price of Oil Be Manipulated? Reader Don H. recently posed a question which should be of interest to all of us who pull into gas stations and purchase the fine product sold there: I want to thank you for all of the information you assemble on your site. Your writings make me delve back into my old textbooks and writings in search of more information on personal economics, business, and consumer trends.Excellent question, Don. For some insight into that possibility, I turned to erudite correspondent Harun I., who has often contributed his insights to this forum. He provided two charts which are displayed below; to view each in full size, click on the chart. The notes below explain exactly what is being displayed.

EXPLANATORY NOTES:

Here are Harun's comments: Attached are charts that hopefully will help to answer how the largest market participants are positioned (what they have been doing with their money). The legend for the charts with indicators that seem to resemble DMI is Large traders=blue, commercial=red.Thank you, Harun, for the charts and commentary. Here, then, is another set of players: hedge funds gambling with their billions of cash, seeking quickie returns to justify their fat fees.  A quick glance at the charts from an inexpert eye (mine) suggests that the price of oil has

stayed in a strong uptrend regardless of traders' positions. If I were in a position to

manipulate the oil futures market (oh how I wish!), I would engineer the occasional free-fall

in order to panic the herd into selling. As the price fell to absurd levels in the ensuing

rush to the exits, I would buy futures on the cheap and then let actual demand drive

the price back up, thereby reaping vast profits once the price returned to its "market" level.

A quick glance at the charts from an inexpert eye (mine) suggests that the price of oil has

stayed in a strong uptrend regardless of traders' positions. If I were in a position to

manipulate the oil futures market (oh how I wish!), I would engineer the occasional free-fall

in order to panic the herd into selling. As the price fell to absurd levels in the ensuing

rush to the exits, I would buy futures on the cheap and then let actual demand drive

the price back up, thereby reaping vast profits once the price returned to its "market" level.

The fact that the price hasn't plummeted in such sharp spikes below the trendline suggests that if some group is keeping the price of oil up, they're not very sharp traders.... alas, we may actually have a market which is high simply due to demand matching supply. Or, perhaps the manipulators are using supply or refining bottlenecks to achieve their goals rather than the futures market. Consider a few statistics: the U.S. uses 23 million barrels a day, or almost 700 million barrels per month, or 8 billion barrels a year. The available inventory "in country" of crude oil is around 320 million barrels, or about two weeks' supply of oil. That's really not much, is it? Then there's the Strategic Reserve of about 700 million barrels, which works out to about a month's supply. Whoopie. That super-giant 3 billion-barrel field everyone's raving about that was recently discovered in the Gulf of Mexico? Nice, but 3 billion barrels--assuming that much can actually be extracted--works out to about 4 months' supply for the nation. You think four months is a long time? Excuse my skepticism about how the world is awash in oil. Perhaps the oil industry is struggling just to keep the 84 million barrels the world burns every day flowing. Which is not to say the market isn't being manipulated, only that the forces at work--demand and supply, which can be constricted for political or financial reasons by exporters and/or refiners--may even exceed the grasp of those desiring to manipulate the price via futures trading. September 13, 2006 The Winning Trifecta: Save the U.S. Auto Industry, Provide Healthcare, and Stop Importing Oil  Here is a bold, practical plan to solve three severe crises

facing the nation: the decline of the U.S. auto industry, the unaffordable-Medicare/Medicaid,

46-million-with-no-health-insurance mess and the "addiction to foreign oil" than our

President so recently pinpointed as a problem. I call it "The Winning Trifecta."

Here is a bold, practical plan to solve three severe crises

facing the nation: the decline of the U.S. auto industry, the unaffordable-Medicare/Medicaid,

46-million-with-no-health-insurance mess and the "addiction to foreign oil" than our

President so recently pinpointed as a problem. I call it "The Winning Trifecta."

Win #1. Save the U.S. auto industry by re-tooling to build super-efficient "cool" vehicles. In the current issue of Scientific American (which I recommended here a week ago), Energy's Future, the article "The Rise of Renewable Energy," contains a sidebar entitled "Plugging Hybrids" which states: "If the entire U.S. vehicle fleet were replaced overnight with plug-in hybrid electric vehicles (PHEVs), the nation's oil consumption would decrease by 70% or more, completely eliminating the need for petroleum imports.What's not to like? I know, I know, Americans demand "sporty" acceleration. My pal Arrol Gellner has the answer: electric drives beat the heck out of gasoline engines. It's true: electric motors have instant torque. There's no waiting around for RPMs to climb. You get instant acceleration. Sure, you need a big enough motor to accelerate the car/truck, but cutting vehicle weight is the other side of the equation: less mass requires less energy. Bottom line: a savvy car company could market a PHEV as the hottest sport vehicle on the road. The "cool" factor would be immense. Not only can you beat an "old" gas truck off the line, you also get outrageously great mileage and cut carbon emissions to near zero. What exactly is a PHEV? It's simply a gasoline/electric hybrid with a good-sized battery. You plug the car in at night (when the draw on the power grid is lowest) to charge the battery, and then go the next morning. If/when the battery is drained, or when certain conditions apply (like a steep hill), the gas engine (running 10% ethanol, why not?) starts up and boosts the power output. People are already making their own PHEVs by tossing a couple batteries in their Toyota or Honda hybrid cars.  According to the current issue of Scientific American (Sept. 2006), Volkswagen has come up with a lightweight two-passenger

prototype "city car" which gets 240 miles per gallon. (See the article

"Fueling our Transportation Future". You can find the issue at your library.)

OK, so it's not for the freeways;

Americans have two or three vehicles anyway, so why not make one of them super-efficient

for short trips?

According to the current issue of Scientific American (Sept. 2006), Volkswagen has come up with a lightweight two-passenger

prototype "city car" which gets 240 miles per gallon. (See the article

"Fueling our Transportation Future". You can find the issue at your library.)

OK, so it's not for the freeways;

Americans have two or three vehicles anyway, so why not make one of them super-efficient

for short trips?

So we have the product and the marketing campaign. Now we get rid of the albatross which threatens to bankrupt GM and Ford: healthcare costs. "Each more than 100 years old, Ford and GM are victims of being successful for too long. GM has 476,000 retirees. Ford provides health insurance for 590,000 people at an annual cost of $3.5 billion. Both Ford and GM have health insurance costs of about $1,100 per vehicle. Neither Asian nor European producers are burdened by such costs."Win #2. Institute a limited and therefore affordable national healthcare plan which covers all Americans, enabling U.S. corporations to compete on a level playing field with foreign companies whose employees are all covered by government-provided healthcare insurance. Referring to the auto industry's healthcare liabilities, knowledgeable reader John B. made this comment: I know some people go crazy about national health care but it is the only way out. I believe corporate America is also starting to like the idea. Then they will not have to pay the cost themselves. Just think -- all of GM and Ford's health care problems will disappear.  Win #3. Drastically reduce and then eliminate foreign oil imports by mandating PHEVs

in government fleets and then in all vehicles. The changeover will take a decade or two,

but look at the enormous benefits in air quality, carbon reduction/global warming, and in the politics

of oil. How to keep the Oil Industry happy? let them make $100 billion in solar panels,

as BP and other oil giants already do. How to create 50% of the nation's electricity with

solar panels to feed the PHEVs? It's actually brain-dead easy: put panels on all existing

building roofs, and

tie them into the existing electrical grid. After all, they're already all connected; how

hard can it be to place a meter for electricity flowing out as well as in? Such a system

is already mandated by California's Million Solar Roofs campaign.

Win #3. Drastically reduce and then eliminate foreign oil imports by mandating PHEVs

in government fleets and then in all vehicles. The changeover will take a decade or two,

but look at the enormous benefits in air quality, carbon reduction/global warming, and in the politics

of oil. How to keep the Oil Industry happy? let them make $100 billion in solar panels,

as BP and other oil giants already do. How to create 50% of the nation's electricity with

solar panels to feed the PHEVs? It's actually brain-dead easy: put panels on all existing

building roofs, and

tie them into the existing electrical grid. After all, they're already all connected; how

hard can it be to place a meter for electricity flowing out as well as in? Such a system

is already mandated by California's Million Solar Roofs campaign.

If this seems implausible, then read

The Solar Economy: Renewable Energy for a Sustainable Global Future

If this seems implausible, then read

The Solar Economy: Renewable Energy for a Sustainable Global FutureSeptember 12, 2006 On Personal Risk Assessment The family and friends of Steve Ng witnessed his burial in Colma, Calif., on August 17. Readers may recall that Steve drowned in the Salmon River in late July under unknown circumstances. He was young and fit, and his accidental death shocked and saddened us. (My account of his death, False Confidence, ran August 12.)

Reader Bill N. sent in his own account of dangerous waters, a story which reminds me that sometimes it's not what we do which saves us, but what we don't do: This tragic story reminds me of something I experienced several years ago.While I'm not familiar with that particular spot, I can well imagine the shorebreak at such a beach. Excellent judgment call, Bill, and an excellent reminder to us all to listen to that little voice of intuition which often tells us something isn't quite right with the water, with the people, with the scene or with the machine. Steve was American through and through, independent to the point of eccentricity, but he was also Chinese-American, and his family honored him with a full traditional Chinese (Hong Kong) funeral. It was our honor to attend the somber rite of passage, and to offer our last respects. September 11, 2006 Why I am Not a Pundit, or, I Could Be Wrong The media will be filled with commentaries on this memory-seared day, and as a result it's a good time to remember something else: nobody knows what the future will bring. Pundits of all stripes, red, blue, green, well-paid, free, snide or serious, lay claim to some insight into events which, by extension, is a prediction of future events. Not many (let's just be brash and say none) mention the uncomfortable reality that no one can accurately predict the future. If someone is so confident of their crystal ball, then I invite them to pony up $100,000 and buy some options to back up their prediction. If they're right, their $100K will turn into a million bucks. Yes, it's pretty easy to leverage a 10-bagger in options if you buy out of the money calls or puts. (Ditto for futures.) You just have to be right. What? Not as confident as we readers imagined? Suddenly there's caveats? If you aren't sure enough to put down your own money in serious amounts, then perhaps one shouldn't put on such confident airs. I have no idea what will happen to the value of oil or the dollar, where interest rates, or any other metric of finance or economics, will be. I do know, however, that the risks of various imbalances are at historic or unprecedented highs. Maybe nothing will happen in the next year or two, and everything will remain pretty much as it is today. That's certainly what's happened for the past two years. But just to mention some potential risks which have been covered here before:  1. The U.S. government is running a large deficit, and must sell hundreds of billions in

bonds each and every year. There is no Plan B. (Cut the deficit? Are you nuts?) The

bonds must be sold to re-finance $6 trillion in old debt and

all new debt ($300-$400 billion a year, depending on which numbers you believe).

Foreign governments and institutions have supported this debt binge by buying

significant amounts of this debt. If for whatever reason they decide buying U.S. debt no

longer serves their best interests, then U.S. bond rates will have to rise high enough to

bring other buyers out of the woodwork.

1. The U.S. government is running a large deficit, and must sell hundreds of billions in

bonds each and every year. There is no Plan B. (Cut the deficit? Are you nuts?) The

bonds must be sold to re-finance $6 trillion in old debt and

all new debt ($300-$400 billion a year, depending on which numbers you believe).

Foreign governments and institutions have supported this debt binge by buying

significant amounts of this debt. If for whatever reason they decide buying U.S. debt no

longer serves their best interests, then U.S. bond rates will have to rise high enough to

bring other buyers out of the woodwork.

It's worth remembering: interest rates aren't set by the Fed, they're set by the buyers and sellers in the bond market. The Fed could lower interest rates to 1% again, inflation could fall to zero, and interest rates could still rise to 13%. If that's what it takes to scare up some buyers, then that's what the rate will be. Is that likely? Perhaps not. But is it impossible? No--because we are beholden to foreign buyers, whose interests may diverge from those of our government.  2. As measured by the VIX and other metrics, risk has apparently been banished from

global markets. Thanks to the rise of derivatives, in their uncounted trillions of

dollars of exposure, every possible scenario has been hedged with an option or future.

Risk has been sliced and diced and hedged to the point that it simply doesn't exist any more.

Market drops? No problem, our puts will cover the loss. And so on, in every market and

every commodity.

2. As measured by the VIX and other metrics, risk has apparently been banished from

global markets. Thanks to the rise of derivatives, in their uncounted trillions of

dollars of exposure, every possible scenario has been hedged with an option or future.

Risk has been sliced and diced and hedged to the point that it simply doesn't exist any more.

Market drops? No problem, our puts will cover the loss. And so on, in every market and

every commodity.

Nice, but mathematical models suggest risk can never be squeezed down to near zero. What if, just to play Devil's Advocate, risk hasn't been banished but merely cloaked? Put another way--what if some macro-event occurs which has not been sufficiently hedged? What if hedged positions start unraveling faster than risk models predict? No one knows the answer, because the global financial markets have never been so leveraged, so hedged, or so liquid. For more, please read The Misbehavior of Markets

3. The demand for and supply of oil are precariously balanced at 84 million barrels a day.

This is unprecedented. Prior to the growth of China, there was always a significant

margin of supply above and beyond any demand. While supply could be artificially lowered

by voluntary caps or political embargoes, the actual supply always exceeded demand. No longer.

Simply put, a precarious balance is more vulnerable than one of untapped surplus.

The Saudis always claim they can pump another couple million barrels a day, but they rarely mention that it's heavy sulfur-laden oil which few refineries can refine. So the bottleneck remains. All the pie-in-the-sky fantasies of shale oil and the like--well, they're years away from production in quantities that matter--and may have physical limits on daily production which cannot be overcome. (The U.S. uses 23 million barrels a day, and the entire Canadian shale oil fields will produce 3 milion barrels at full production. And China has spoken for at least 1 million barrels per day, so it's actually 2 M at best.)  4. The trade imbalance (as noted last week) exceeds 6% of U.S. GDP, a rate which

historically has not been sustainable. Does that mean we can't keep up the buying binge

of overseas goods? I have no idea, but it's certainly not a guaranteed bet that there will

never be any unhappy consequence of current account deficits on the order of $1 trillion/year.

4. The trade imbalance (as noted last week) exceeds 6% of U.S. GDP, a rate which

historically has not been sustainable. Does that mean we can't keep up the buying binge

of overseas goods? I have no idea, but it's certainly not a guaranteed bet that there will

never be any unhappy consequence of current account deficits on the order of $1 trillion/year.

I could go on, but we all know about housing, and how 46% of all corporate profits have flowed from the financial sector--you know, the companies which sold all those ARMs and option ARMs and mortgage-backed securities. And golly gee, if housing rolls over, where exactly is the financial sector gonna go to replace all that profit? And where are the stock markets gonna find enough profits to replace the half which will vanish along with the housing boom/bubble? And what will support stock markets if half their vaunted profits slip quietly into the night? Who knows, maybe housing will recover, and new loans will be written and all the risky loans will be re-financed, filling the coffers of the financial corporations with new profits. Nobody knows, but the risk remains high that the housing bubble, like any other financial bubble, will not deflate so kindly. But maybe it will. Maybe nothing will happen and the doom-and-gloom crowd (me included) will have to swallow our warnings for yet another year of upbeat, solid growth in sales, GDP, equity values, etc. Go ahead and bet on that scenario if you want, but I'll stay over here on the sidelines, thank you very much. The risk of injury looks pretty high in the pundit game right now. September 9, 2006 Protecting Capital: The Demographics of Decline  Astute reader Kevin K. recommended this article by Bill Gross, well-known bond guru at

Pimco: Investment Outlook,

September 2006: No Cuts, No Butts, No Coconuts, a long, thoughtful essay on the

demographics of the Baby Boom retirement and the financial consequences of that demographic.

Astute reader Kevin K. recommended this article by Bill Gross, well-known bond guru at

Pimco: Investment Outlook,

September 2006: No Cuts, No Butts, No Coconuts, a long, thoughtful essay on the

demographics of the Baby Boom retirement and the financial consequences of that demographic.

Before I quote from the essay, take a look at this small chart. It more or less encapsulates the dilemma Mr. Gross describes: there is no way in goldurn heck we as a nation can pay for the entitlements (Medicare and Social Security) which have been been promised to the Baby Boom generation--all 77 million of us, about a quarter of the entire U.S. population. And "we" start retiring in less than two years. Here are some insights from Mr. Gross: (emphasis added) Something has to give way. In financial terms alone, Laurence Kotlikoff, a Boston University economist has estimated the unfunded liabilities of Americans associated with healthcare and retirement amount to $80 trillion, over seven times our annual GDP!Talk about heresy! To state the obvious, that tomorrow's workers will be unable to fund the sort of lavish retirement that is being heaped on the present generation--why, it's heresy of the first order! Doesn't Bill Gross know that we can just borrow another trillion or two from the Japanese, Chinese and Saudis to fund the Baby Boom's big-bucks retirement? Doesn't Bill know that borrowing more is the painless solution to all problems? Get with the program, Bill. Don't frighten us with all that stuff about being in the hole $80 trillion and having to work past 62... whew, you had us going there. Next thing you know, Bill will be saying crazy stuff like housing can actually decline for years or even decades. Come on, Bill, I'm gonna be living like a millionaire once I sell my crib, without having to save a dime or work another day. Housing never drops nationally, it only rises, decade after decade, magically enriching us all. Ah, but Bill gets the last word, and its a doozy: Too late to have babies, too politically sensitive to import more workers, too daft to recognize that the boomer winter is rapidly approaching and that our assets will not fund our liabilities. Too, too. Too, too. Too, too. What does a government do that is too absorbed in the moment and fails to alert its citizens to the perils ahead? Cut in line, I suppose. It devalues its currency, it reflates/inflates its economy, and because that doesn�t create real wealth, it recites the mythology of a bygone era, of a �shining city on a hill,� so that its citizens believe they�ve never had it so good.  The 2008 retirement of the Boomers born in 1946--the first year of the Boom-- has been

drawing a lot of media attention, and for good reason: if Medicare and Social Security

are running huge deficits now, what happens as millions of Boomers start retiring and

drawing their entitlement benefits?

The 2008 retirement of the Boomers born in 1946--the first year of the Boom-- has been

drawing a lot of media attention, and for good reason: if Medicare and Social Security

are running huge deficits now, what happens as millions of Boomers start retiring and

drawing their entitlement benefits?

Not only that, but as other commentators have asked, what happens to the housing market when Boomers start selling off their primary residences and investment properties? Given that the generation behind the Boomers is much smaller in number, who exactly is going to buy all those millions of properties? What if the supply of housing for sale swamps the demand, not just for a year or two but for a decade or two? What happens to the price of any commodity when the over-supply is basically permanent? Then there's the financial assets, stocks and bonds. As Boomers start drawing upon their IRAs and 401K plans, guess how they will raise cash--by selling the stocks and bonds in their retirement accounts. Selling them monthly, year after year, or liquidating them in huge chunks to pay retirement or healthcare costs. What happens to the stock and bond markets when there is an unceasing wave of relentless, decades-long selling by millions of retirees? Exactly who will be the buyers of the hundreds of billions in stocks and bonds which will soon be liquidated? The saying is, "Demographics is destiny," and while that may over-simplify things, it certainly speaks to the power of raw numbers and simple multiplication. Programs such as Medicare which were designed in the 1960s to pay modest sums for the care of a few million poor elderly are now on the entitlement hook for tens of millions of oldsters, millions of whom are loaded, wealthy, rich, call it what you will--and their care is anything but modest. One solution has also been posited by various pundits--a return to thrift and savings. If middle-aged American wage earners changed from saving -1% of their earnings to 10% positive savings, then their retirement might actually have a chance to be funded. But what happens to a consumer economy utterly dependent on, well, consumer spending, for 70% of its GDP? The loss of 10% of that spending would sink that economy faster than a torpedo, taking profitability and hence the stock market with it. Last but not least, here are two links worth checking out. Fred Roper's Blog: Fred makes a fascinating argument based on Christian theology for a national healthcare system, and I think he's onto something important. As a lawyer, he also rightly traces many bankruptcies not to slovenly finances but to medical expenses. We live in a country where a brief hospital visit can cost $700 and treatment for a heart attack can run to six figures. What kind of insanity is this, and why do we as a citizenry tolerate it? In any event, check out Fred's blog for more on these topics. Correspondent Michael Goodfellow also recommended the The Prudent Bear website. If you're skeptical of the Goldilocks economy, check it out. September 8, 2006 Protecting Capital: Commodities  For your consideration: two charts of the commodity that people love to love or love to

hate: gold. What is clearly visible in the first one is what technical analysts call

a wedge. The general view of a wedge is that it presages either a big break down or a

big break up.

For your consideration: two charts of the commodity that people love to love or love to

hate: gold. What is clearly visible in the first one is what technical analysts call

a wedge. The general view of a wedge is that it presages either a big break down or a

big break up.

As we ponder which way POG (as price of gold is affectionately known) might go in the near future, let's look at a longer term chart of the GOX, a basket of gold mining stocks which make up the CBOE (Chicago Board of Exchange) Gold Index. (This chart displays the activity from June 2004 to the present.)

I have added some trendlines, which show that the index has been in an upward trend for some time. The recent spike and decline has set up the above-mentioned wedge, but technically, there are several reasons to believe that gold remains in a long-term uptrend. 1) The index has bounced off major support levels (the 200-day simple moving average and the 50-day simple moving average), and the MACD (moving average convergence-divergence) chart is showing a bottoming formation which in the past presaged a major, sustained rise in the index. Fundamentally, the price of gold reflects the value of the dollar and the general "fear factor" in the marketplace. When times were confidently euphoric in the late 90s, gold was hitting 20-year lows. No one was interested in a commodity which had been dropping for 20 years. But as times have grown more uncertain, gold has reflected this anxiety by rising inexorably since the dot-com crash of 2000. Those who believe we are entering a deflationary period, in which cash grows in value as the price of goods and services drops, have little reason to turn their rising-in-value dollars for gold. Those who believe the Wall Street nostrums about the "Goldilocks economy" in which GDP growth and inflation both stay around 2% also have no reason to buy a commodity (or the miners which produce it) which produces no dividend and which hedges a dollar which is basically (in their view) benign. Those who believe the inflationary pressures which are building as a result of inflationary expansion of the money supply, the tripling in the cost of oil and the unabated rise in the costs of domestic labor benefits, medical expenses, etc. have a number of reasons to own gold or gold mining stocks. As inflation gnaws away at the value of cash and the value of other asset classes drops in a stagflationary malaise, gold at least holds out the possibility of retaining its value, i.e. rising as the dollar drops.  No one knows what the price of gold or mining stocks will do, next week, next month or

next year, but those are the basic scenarios. Some analysts, for instance,

Louise Yamada Technical Research

Advisors, believe that both gold and agricultural commodities are in 20-year uptrends.

No one knows what the price of gold or mining stocks will do, next week, next month or

next year, but those are the basic scenarios. Some analysts, for instance,

Louise Yamada Technical Research

Advisors, believe that both gold and agricultural commodities are in 20-year uptrends.

As for agricultural commodities, consider this chart of the demand for grains in China. If this demand is sustainable--and there are reasons to think it might be, such as the loss of cropland in China due to desertification and urbanization, the rising wealth of the populace (and hence their growing appetite for grain-fed poultry, pork and beef) and perhaps even the changing fortunes of agricultural areas in an era of rising global temperatures-- then grains and perhaps the lands which produce it might well become more valuable. The danger in any commodity, however, is that new supply may rise to meet or even exceed demand. It is only when oil, gold and grain production cannot meet demand that prices will rise in a sustainable fashion. Are we at that point? Those who give credence to long cycles see the past six years of commodity price increases as only the first stage of a much longer cycle. No one knows if this will prove true, but the rise of India and China certainly makes a fundamental case for that position. September 7, 2006 Protecting Capital: The Trade Imbalance and the Dollar Before we get to the dollar, let's take a look at a chart of the Nasdaq. Why? Because the market suddenly discovered the wage inflation I documented yesterday, and promptly dropped. As my notes indicate, this is a critical roll-over, as this "head-fake" rally failed to rise to the 200-day moving average (the thin red line). Note also that the index managed to hit the classic signs of a Bear Market--lower lows and lower highs.

Does any responsible person actually believe the hocus-pocus line that inflation is benign and will always remain so, now that the Fed has raised rates from a massively inflationary 1% to a still-historically low 5.25%? This chart suggests traders are no longer so sure that Tooth Fairy Fantasy is actually true.  OK, on to the dollar. Why should we care about the relative value of the dollar? Let's

take a look at a chart of how much we as a nation are buying from other countries.

Gee, it seems we're buying about 6% more of our entire GDP than we sell. That works

out to a deficit (imbalance) of about $800 billion. So why do we care? For two reasons: