|

|

|

||||||||

|

The Pareto Principle and the Next Wave Down in Real Estate (August 24, 2009) In February 2007 I suggested a 4% mortgage delinquency rate could trigger a decline in the entire housing market. Since that proved prescient, we should revisit the analytic tool behind that call: the Pareto Principle. There is a whiff of euphoria in the housing market, a heavily touted confidence that "the bottom is in." It's all roaring back--rising sales, multiple bids by anxious buyers, 3.5% down payments, low mortgage rates and the bonus of an $8,000 first-time home buyer credit (a gift from U.S. taxpayers). Housing Lifts Recovery Hopes (Wall Street Journal) Foreclosure-related sales account for over 30% of all sales nationally, and over 70% in hard-hit markets such as Las Vegas, but like piranhas feasting on a school of weakened fish, nobody in the real estate business mentions the huge losses of capital and equity which created all these "bargains." All we need for a complete bubble reflation is people avidly gaming the system... oh wait, we have that, too. A recent Time magazine cover story on Las Vegas contained this informative tidbit (courtesy of Michael Goodfellow):

(Realtor) Boemio specializes in short selling, in a particularly Vegas way. Basically, she finds clients who owe more on their house than the house is worth (and that's about 60% of homeowners in Las Vegas) and sells them a new house similar to the one they've been living in at half the price they paid for their old house. Then she tells them to stop paying the mortgage on their old place until the bank becomes so fed up that it's willing to let the owner sell the house at a huge loss rather than dragging everyone through foreclosure. Since that takes about nine months, many of the owners even rent out their old house in the interim, pocketing a profit. Hmm, isn't this the same recipe of froth, low down payments, cheap, easy mortgage money and scamming which got us in trouble the last time? Only the lenders lose, but then now that Ginnie Mae and FHA have stepped up to replace the disgraced, bankrupt shells of Fannie Mae and Freddie Mac, then it really isn't the lenders taking the risks, it's the U.S. taxpayer (again). It's the same old mispriced risk and misallocated capital which created and popped the housing bubble in the first place, with the lagniappe insanity of giving people $8,000 of taxpayer funds to prop up home sales to benefit builders, realtors and lenders. (Hats off to their lobbyists--Congress stood on its hind legs and barked on command. "How many years to the next election, Tuffy? Bark! Good dog--only one!") It's not just new buyers and gamers buying--it's investors plunking down all cash for "bargains," in many cases outbidding each other just like the good old days. 'Cash is king' in market for foreclosed homes (SFGate.com)

All-cash sales are most common where prices are low and bank-owned properties account for the lion's share of listings. In foreclosure-ridden Pittsburg, for instance, 42.7 percent of home sales in the first three weeks of July had no record of a purchase loan, according to county data analyzed by MDA DataQuick. The median price for those transactions was $105,000. Despite the cheerleading, the gaming and the "Gold Rush mentality" there are a few flies in the ointment. Topping the list: almost one in seven mortgages are distressed--in foreclosure or delinquent: 4.3% of mortgages in foreclosure (marketwatch.com)

The non-seasonally adjusted delinquency rate increased from 8.22 percent in the first quarter of 2009 to 8.86 percent this quarter. Then there's these factors: Souring Prime Loans Compound Mortgage Woes (Wall Street Journal) Improving Home Sales Belie Market Reality (Wall Street Journal) Can Vanished Real Estate Wealth Come Back? (Wall Street Journal)

I have applied the Pareto Principle to the housing market over the years, and now that foreclosures have hit the critical 4% mark, it's time to revisit the 4/64 rule and the 80/20 rule. I was introduced to the Pareto Principle by longtime correspondents Harun I. and U.K.C. The Pareto distribution quite effectively predicted that the 4% "vital few" subprime defaults would have an outsized effect on the 64% "trivial many" households with mortgages. Readers of this blog learned in May 2006 of the likelihood that 5 millions homes would soon be in foreclosure:

How Many Foreclosures Will Hit the Market? (May 1, 2006)

Bingo, foreclosures are on track to exceed 5 million shortly. (1.3 M in 2007, 2.3 M in 2008 and 1.8 M (est.) in 2009.) Critics might well ask why the The Pareto distribution should apply to the mortgage/housing market. It is a fair question, because the Pareto Principle is not causal--it merely captures the distribution probabilities within groups. That said, there are a number of fundamental causal drivers which suggest the 4% of homes in foreclosure will have a dramatic, long-term negative influence on the value of 64% of the housing market (the 4/64 rule). Once the number of distressed mortgages rises from 13% to 20%, then we can anticipate the 80/20 rule will apply: those 20% will wield an outsized influence on the remaining 80% of mortgages. Recall there are about 50 million mortgaged homes in the U.S. and about 25 million owned free and clear. The value of all homes will be pressured as foreclosed and distressed housing is placed on a saturated market. A key driver of future delinquency is negative equity. Owing more than the value of the home saps homeowners' willingness to "stay the course" and keep sacrificing to pay the mortgage. Regardless of your opinions on the morality of this trend, it is undeniable:

Almost one-third of home loans under water

More than 15.2 million U.S. mortgages, or 32.2% of all mortgaged properties, were in a negative-equity position on June 30, edging down from 32.5% at the end of March, according to the real-estate information company, which tracks data on about 90% of mortgage loans nationwide.Foreclosures Drag on U.S. Recovery (Dismal Scientist)

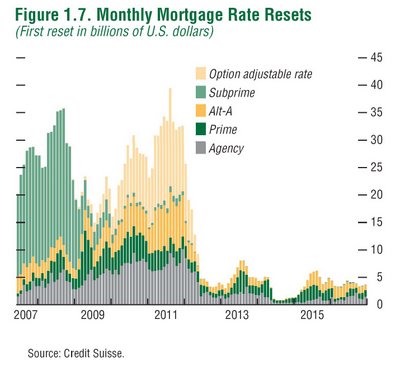

Foreclosures depress house prices through three channels: increased supply, discounting, and the neighborhood effect. In the first case, additional inventory comes on the market when homes are foreclosed, adding to supply just as the recession is curbing new household formation, keeping demand for housing weak. Second, banks typically discount the price of foreclosed properties to encourage quick sales. Foreclosed homes also are often damaged, reducing their value. None of the conventional price indices capture this effect. Once the homes with negative equity surpassed 20% of the total market, a new dynamic set in. One recent report estimated 50% of U.S. homes would be "under water" by 2011. Given the Pareto distribution, this seems entirely reasonable and even conservative. What about all those homes being snapped up with investor cash? The idea, of course, is that the "smart buyers" will rent the properties out to cover all the carrying costs and then profit as housing "recovers." Please excuse my cynical snort. Being a landlord/landlady is not an easy business. Human being have all sorts of perverse reactions to higher rents, such as moving out and leaving you with big fat vacancies. Humans under financial stress also display all sorts of quirky behaviors such as not paying the rent, or paying sporadically. And when you try to evict them, other quirks can kick in, like suing you for discrimination, claiming you failed to keep the property habitable, and so on. Some might take out their anger at your unreasonable greed by trashing the house. To make them go away usually requires a few thousand dollars' cash "incentive." So much for those "easy profits." Most annoyingly, houses actually require constant upkeep and financial investment to be rentable. Houses are not bonds. They do not pay "dividends" with no work and no further expenses. Costly things are always going wrong. You can ignore them and be a slumlord, but then an amusing reaction called "karma" sets in and you end up getting the kind of tenants you deserve. Fantasies of easy wealth via landlording die quick and hard. A funny thing happened on the way to a long, drawn-out New Depression--lots of people no longer have the financial ability to pay rent in any amount above zero. All those folks the new "investors" are counting on to rent their trashed, abandoned houses will be moving back home with parents, sleeping on sofas, renovating garages and outbuildings into semi-habitable spaces, moving into welfare SROs, moving back to their nation of origin, etc. Just anecdotally, I know of one investor who bought a multi-unit building and promptly jacked the rents 20% to reap a tidier profit. Most of the tenants are leaving. Good luck with that "I'm gonna get rich as an absentee landlord" game. I anticipate a wave of desperate sellers in 2010 trying to dump their "can't lose rental investments" for any price as long as it's cash. Yes, it is possible to earn a modest positive return on rental properties, if you maintain the property scrupulously, screen your tenants as if they were future in-laws, study your neighborhood rental markets carefully and respond to your tenants as valued customers rather than annoyances. Few landlords are willing or able to do the above and hence losses and vacancies are guaranteed. And the mortgage re-sets just keep coming. We've all seen this chart so often that we've become numb to the dire consequences it implies:

Let's also consider the waveform of every financial bubble. With minor variations just to keep life interesting, all financial bubbles follow this basic progression:

There is always a false bottom/false dawn marked by euphoric buying by those who expect a resumption of a trend which is irrevocably broken. Now that foreclosed houses are drawing 30 cash bids above asking, I think we can safely announce that the post-false bottom peak is at hand. There is generally a rough symmetry to bubbles. Thus since the housing bubble took about 11 years to reach its apex (roughly 1996-2006) then we can expect about an 11-year downcycle (2007-2017) give or take a few years. To expect a decade-long bubble to bottom in a mere 18 months is folly. Few beyond historians know that half of all urban homes were in default/delinquency during the Great Depression of the 1930s. Various Federal schemes were put in place to suppress this national default: bans on foreclosures, renegotiating existing under-water loans, etc. None of them changed the fundamental reality or "fixed" the housing market. We would be wise to recall this history before placing too much faith in re-runs of the same policies.

Thank you, Cheryl A. and Alberto R., for your suggestions to revisit the housing market.

"Your book is truly a revolutionary act." Kenneth R.

"This guy is THE leading visionary on reality.

He routinely discusses things which no one else has talked about, yet,

turn out to be quite relevant months later."

NOTE: contributions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Or send him coins, stamps or quatloos via mail--please request P.O. Box address. Your readership is greatly appreciated with or without a donation.

For more on this subject and a wide array of other topics, please visit

my weblog.

All content, HTML coding, format design, design elements and images copyright © 2009 Charles Hugh Smith, All rights reserved in all media, unless otherwise credited or noted. I would be honored if you linked this wEssay to your site, or printed a copy for your own use. |

|

| consulting | blog fiction/novels articles my hidden history books/films what's for dinner | home email me | ||