|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | ||

Writing/Film Dear Aspiring Writers: The Worst Advice You'll Ever Read A Literary Look at I-State Lines Spirited Away: Decay and Renewal An American Poem (Robinson Jeffers) Taoist Chinese Poems The Nelson Touch "It's all about oil, isn't it?" Kurosawa's High and Low A Bountiful Mutiny Howl's Moving Castle Thailand's Iron Ladies Trois Colours: Red The Thin Man: Thoroughly Modern Movies Why My Book Is Better Than the DaVinci Code Iranian Films: The Mirror Piratical Nonsense A Real Pirate Movie: Captain Blood 9 more in archive Recommended Books American Identity American Identity Literary Contest Winners, 2006 (fiction and essays) Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Your Tattoo in 50 Years The American House and Frank Lloyd Wright Cultural Commentaries On Hatred and Anti-Americanism Anti-Americanism Part 2 Anti-Americanism Part 3 French-Bashing Germany: We All Have Problems, But... Kroika! Chronicles This Blog Sells Out Doom and Gloom Sells The Kroika Mascot-"Auspicious Pet" Wal-Mart and Kroika Kroika and Starsbuck Take a Hit Kroika Ad 1 Kroika Ad 2 Kroika Ad 3 Kroika Ad 4 Kroika Makes Bid for Oreo (April 1) Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Corruption and Avian Flu: China's Dynamic Duo Exporting the Real Estate Bubble to China Is the Bloom Off the China Rose? China Irony: Steel, Marx & Capital Curing The U.S. and China's Dysfunctional Relationship China and U.S. Inflation Trade with China: Making Out Like a Bandit Whither China? Will the Housing Bust Take Down China? China's Dependence on Exports to U.S.; Is China About to Pop? 8 more Battle for the Soul of America Katrina, Vietnam, Iraq: National Purpose, National Sacrifice Is This a Nation at War? A Nation in Denial Why Is This Such a Tepid Time? That Price Isn't Cheap, It's Subsidized The Most Hated Company in America U.S. Fascists Seek Ban on Cancer Vaccine The Truth About Christmas American Dream or American Nightmare? 2006 Sea Change Obesity and Debt Immigration Ironies U.S. Healthcare: Working Toward a Real Solution A Drug Industry Running Amok Where There Is Ruin 10 more Financial Meltdown Watch What This Country Needs Is a... Good Recession Are We Entering the Next Age of Turmoil? Why Inflation Appears Low Doubling Down on 5-Card No-See-Um A Rickety Global House of Cards Are Japan and Germany Truly on the Mend? Unprecedented Risk 2 Could One Rogue Trader Bring Down the Market? Worried about Inflation? Stop Measuring It Economy Great? Bah, Humbug Huge Deficits and Huge Profits: Coincidence? Who's The Largest Exporter? Three Snapshots of the U.S. Economy Loaded for Bear Comparing Nasdaq to Depression-Era Dow Who's Buying Treasury Bonds? And Why? Derivatives: Wall Street Fiddles, Rome Smolders Financial Chickens Coming Home to Roost Is the Stock Market on the Same Planet as the Economy? The Housing-Recession-Oil-Healthcare Connection Could We Have Deflation and Inflation At the Same Time? What We Know, What We Can Safely Predict Bankruptcy U.S.A.: Medicare, Greed and Collapse Sucker's Rally A Whiff of Apocalypse Where There Is Ruin II: Social Security 31 more Planetary Meltdown Watch The Immensity of Global Warming Sun Sets on Skeptics of Global Warming Housing Bubble Watch Charting Unaffordability A Monster of a Housing Bubble A Coup de Grace to the Economy Hidden Costs of the Housing Bubble Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Housing Market Slips Toward Cliff Housing Market Demographics Housing: Catching the Falling Knife Five Stages of the Housing Bubble Derailing the Property Tax Gravy Train Bubbling Property Taxes Have You Checked Your Property Taxes Recently? Housing Bubble: Where's the Bottom? Housing Bubble: Bottom II The Housing - Inflation Connection The Coming Foreclosure Nightmare 1 How Many Foreclosures Will Hit the Market? Housing Wealth Effect Shifts Into Reverse Housing Bubble Bust Will Take Down the Global Economy The New Road to Serfdom: A Negative-Equity Mortgage The Housing-Savings-Recession Connection After the Bubble: How Low Will It Go? After the Bubble: Rents and Housing Values Why Post-Bubble Rents Matter After the Bubble: How Low Will We Go, Part II Housing: 10% Decline May Trigger Financial Ruin How to Buy a $450K Home for $750K Inflation and Housing: Calculating the Bust The Growing Financial Risks of the Housing Bubble Construction Defects: The Flood to Come? Construction Defects Part II Who Gets Hammered in the 2007 Housing Bust Real Estate Bust: The Exhaustion of Debt What Happens When Housing Employment Plummets? One More Hole in the Housing Bubble: Insurance Financial Kryptonite in a "Super-Strength" Housing Market Three Secrets to Unloading Property Today Welcome to Fantasyland: Housing's "Soft Landing" Why Is the Median House Price Still Rising? Why Median Prices Appear to be Rising? The Root Cause of the Housing Bubble Housing Dominoes Fall Twilight for Exurbia? Phase Transitions, Symmetry and Post-Bubble Declines 10 more Oil/Energy Crises Whither Oil? How much Is a Gallon of Gas Worth? The End of Cheap Oil Natural Gas, Naturally High Arab Oil Money and U.S. Treasuries: Quid Pro Quo? The C.I.A., Oil and the Wisdom of Crowds The Flutter of a Butterfly's Wings? A One-Two Punch to a Glass Jaw Running Out Of Oil vs. Running Out of Cheap Oil 2 more Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds Geezer Rock Overload Paying for Web Content In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono Happiness for Sale: Jank Coffee Ten Guaranteed Predictions for 2010 Why My Book Is Better Than the DaVinci Code My Brand Management Stinks Design Follies The New Jank Coffee Shop Jank Coffee, Upscale Tropic Style One-Word Titles Complacency Nostalgia Lifespans Praxis Keys to Affordable Housing U.S. Conservation & China Steve Toma, Me & Skil 77s: 30 years of Labor Real Science in the Bolivian Forest Deforestation and Sustainable Forestry The Solar Economy (book) The Problem with Techno-Fixes I Love Technology, I Hate Technology How To Blow off Web Ads and More 2 more Health, Wealth & Demographics Beauty of the Augmented (Korean) Kind Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Is Obesity an Inflammatory Response? Demographics & National Bankruptcy The Decline of Europe: A Demographic Done Deal? Are the Risks of Obesity Overstated? Healthcare: Unaffordable Everywhere Medication Nation The New Disease We Just Know You've Got Can You Can Tell Which Pill Is Fake? Bankruptcy U.S.A.: Medicare, Greed and Collapse The 10 Secrets to Permanent Weight Loss 5 more Landscapes Selling the Landscape The Downside of Density Building Heights and Arboral Roots Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Waimea Canyon, Yosemite, Camping & Pancakes Nourishment The French Village Bakery Ideas What Is Happiness? Our Education System: a Factory Metaphor? Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi Splogs, Blogs and "News" "There is no alternative to being yourself" Is There a Cycle to War? Leisure, Time and Valentines Is the Web a Giant Copy Machine? Science Matters Anti-Missile Defense: Boost Phase Vulnerability History The Strolling Bones: Rock of Ages Bad Karma: Election Fraud 1960 Hiroshima: First Use All the Tea in China, All the Ginseng in America Friday Quiz Pet Obesity The Origins of Carbonara Organic Farms Oil and Renewable Energy Human Diseases Wine and Alzheimers Biggest Consumers of Chocolate 7 more Essential Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So Fewer: How the New Demography of Depopulation Will Shape Our Future The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal The Future of Life Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies The Solar Economy: Renewable Energy for a Sustainable Global Future The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Feeling Good: The New Mood Therapy Revised and Updated Recommended Books More book reviews Archives: weblog October 2006 weblog September 2006 weblog August 2006 weblog July 2006 weblog June 2006 weblog May 2006 weblog April 2006 weblog March 2006 weblog February 2006 weblog January 2006 weblog December 2005 weblog November 2005 weblog October 2005 weblog September 2005 weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

|

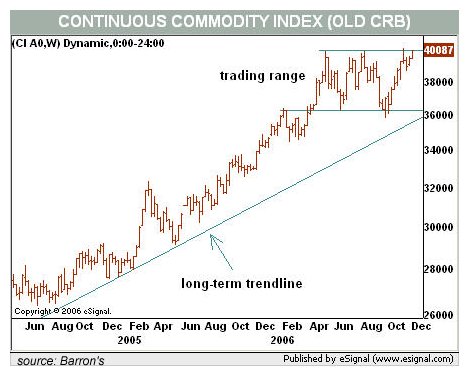

November 30, 2006 This Week's Theme: Beneath the Surface Part IV: Commodities, Gold, the Dollar and The Wealth Effect We turn once again to invaluable contributor Harun I. for two telling charts: the Dollar-Gold ratio and the Dollar-Commodity ratio. For a brief introduction to their import, here are Harun's comments: Every time I look at these charts I wonder how any reasonable economist could state with a straight face that there is a wealth effect. Against gold and commodities, the dollar�s purchasing power has plummeted at a mind boggling rate and somehow CNBC doesn�t think anything is wrong. Why haven�t they put up any of our charts on their screens and discussed their implications?"The wealth effect" is the cherished notion that rising property or equity values embue the giddy owner-consumer with a godlike sense of spending power due to his/her rising fortune. (And the best part, of course, is that all that extra wealth is free, i.e. unearned.) What these charts reveal is that, priced in actual goods (commodities like oil and sugar) or in a commodity which maintains its value in all currencies (gold), the Average Joe has suffered a stupendous loss of real wealth, i.e. buying power.

Even taking into consideration the rise (in dollars) of real estate and the stock market, the average American has still not kept pace with either gold or commodities. The rise in net worth priced in dollars has not even offset the decline in wealth priced in real goods and gold.

This may help explain why Americans have borrowed hundreds of billions of dollars from their declining home equity just to maintain their lifestyle, and why increasing numbers of Americans feel more financially insecure than they did five year ago. There is little wonder why they feel poorer when you gaze at these charts. They are poorer. Last but not least, let's consider the popular notion that commodity prices are falling. Oh really? Not according to this chart, which reveals that commodities--even with the 25% decline in crude oil prices--are poised to break out to new highs:

These charts reveal that there is a major divergence between wealth as measured in dollars--what the pundits crow about--and wealth in terms of purchasing power. Americans are far poorer than they were a mere five years ago, before the dollar lost a third of its value and gold and commodities began their ascent. Are you catching on to the deception here? It's similar to the "new Dow high" deception; adjusted for inflation and the declining value of the dollar, the stock market is far from its highs, and Americans have collectively become vastly poorer, even as we borrow billions from foreign investors every day to keep our fabulous deficit lifestyle afloat. Do chickens come home to roost? Yes, they do. And the cheerleader rah-rah Bull Market pundits will rue the day. November 29, 2006 This Week's Theme: Beneath the Surface Part III: The Dow and Gold Frequent contributor Harun I. was kind enough to provide this chart of the Dow Jones Industrial Average (DJI) and the DJI in a ratio with gold (DJI/gold). AT first glance you notice a rather startling disconnect which occurred at the market low in 2002.

From approximately 1980 through 2002, the ratio of the Dow and gold moved in sync (i.e. was in correlation) with the Dow Jones Industrials. But since the market low in 2002, the two have radically diverged. Now it is always possible that a historic correlation has been broken. But it behooves those of us trying not to lose whatever capital we might have in this world to consider an alternative: that the divergence will return to convergence. One way for this to happen would be for gold to drop in half to $300/ounce. Then the ratio of the DJI to gold would be 40 (12,000 / $300 = 40). Another way would be for the DJI to drop back to the neighborhood of 1,000, where it was in 1980. At that point, the Dow and the price of gold were roughly equal (800 and $800). In the current euphoria of a world awash with liquidity, leveraged assets (derivatives) and a mad scramble for higher yields, such possibilities sound absurd. But just for the sake of argument, what would it take for gold to plummet from $600 to $300? A mighty rise in the dollar, perhaps; and what might trigger such a massive appreciation in the dollar? A complete collapse of the yen and euro, perhaps? But with the U.S. current account deficit already at an unsustainable 7% of GDP, what would cause our trading partners' currencies to collapse and the dollar to double? I am open to the possibility, but the fundamentals behind such a move are unclear. The likelier possibility is a collapse in the dollar and a doubling of the price of gold. Could the Dow fall to 1,000? Various Elliott Wave theorists suggest this is a possibility. What could induce such as drastic collapse of valuation? One mechanism would be high inflation; when Treasuries are paying 15%, stocks are unattractive in the extreme. Another is a collapse in profitability; if a global recession decimated the profits of the DJI companies (for instance, orders for new Boeing jets were cancelled because air traffic had fallen off a cliff, and the need for more Cisco routers vanishes), then on a purely mechanical price-to-earnings basis the Dow could shrink to 1,000. At Bear market lows, the PE ratio sinks to around 8, which is roughly a third of the current Dow PE ratio. In other words, based on a Bear market PE, the Dow could fall to 4,000 with no reduction of actual profit. It's certainly something to ponder. (A.M. addendum: Harun just reminded me of yet another alternative--that the DJI will continue its stratospheric climb. Given the liquidity and euphoria of the past five months, this is entirely possible.) November 28, 2006 This Week's Theme: Beneath the Surface Part II: Bonds and Interest Rates Yesterday we looked at the downtrend in the dollar. Now let's consider the twins: U.S. bonds and interest rates. As long-suffering readers know, I never tire of repeating that the bond market, not the Fed, sets interest and mortgage rates. The consensus which has been propelling the stock market for months is that the Fed will lower Fed Funds Rates, and thereby lower mortgage and interest rates. Nice, but forces are at work which could force the Fed to do the opposite, i.e. raise rates. And why are we considering such an outlandish idea? Take a look at this chart of Treasuries:

What this chart suggests is a breakdown has occurred--put simply, interest rates aren't dropping, they're set to rise further. What forces could cause such a reversal? Inflation. Again, the consensus is deflationary: the slowing U.S. economy will cause everything to become cheaper. I have attempted to explain here many times that not all forces in the global economy are deflationary. Here is a quick summary: 1. If the dollar drops, imports cost more. That is inflationary. Given that imports are fully 7% of the U.S. GDP, rising import costs are non-trivial. 2. Many costs continue to rise regardless of "deflation:" medical costs, tuition, food, etc. While travel to India for heart surgery is being touted as a solution, it is an extremely small piece of a multi-trillion dollar cost machine. In the meantime, healthcare costs continue climbing. Ditto for tuition, food, water, government services, etc. These essentials are simply costing more on a fundamental basis. Hence my suggestion that deflation is limited to discretionary spending like restaurant meals, while non-discretionary costs such as food, education, healthcare, water and government services are all continuing to rise. 3. Labor costs continue to skyrocket. While outsourcing is continually touted as the deflationary trend which will slay high labor costs, the examples given are trivial in the extreme: yuppies can now hire online tutors based in India for their kids. Nice, but please compare those private savings with the hundreds of billions in local school district budgets, and note the fierce resistance which public unions will offer to "deflationary" proposals such as online tutoring via the Internet. 4. Full employment eventually raises labor costs. In case you haven't noticed, the economy is basically at full employment. Sure, many of the jobs are not great, many are low-paying, and many professionals are under-employed. But to someone who remembers the 15% unemployment of 1981, well, this is as close to full employment as reality can manage. Lest you believe that rising labor costs are mere figments of imagination, please read this recent piece from BusinessWeek: U.S.: Strong Labor Markets Put The Fed On The Spot; Weak productivity and rising labor costs could force more rate hikes. 5. The deflationary benefits of moving production to China have run out. Now the cycle of rising prices from China begins. Please read this feature from last week's BusinessWeek: Secrets, Lies, And Sweatshops. If you read the piece carefully, you'll note that the factories are all forced to cheat on labor laws because the wonderful U.S. retail giants are constantly squeezing the factories for ever-lower prices. This trend of ever-cheaper goods from China is over; labor costs are rising in China, too, as I have documented here previously. As profit margins for Chinese manufacturers drop to 5% and under, there are no more savings to be had. The cost of goods from Cbina will begin to rise. The deflationary wonder days are over. Ask yourself this simple question: what can be made in China that is not already made in China? Autos and aircraft? Undoubtedly, but that is well into the future. In the meantime, virtually everything that can be made in China is made in China. What this means is the deflationary forces of offshoring will diminish. The low-hanging fruit has all been picked, and from here on the benefits of offshoring will be harder to discern and perhaps illusory. 6. The price of oil will not plummet to $20/barrel. Why? Production is falling. As I have documented here repeatedly, the supermassive oil fields which we depend on for the majority of our oil from the Mideast are topping out. The Saudis and Kuwaitis are investing in technologies to wring more oil from these fields, but the easy, cheap stuff is already in decline. A U.S. recession may not depress the price of oil as much as expected. (Please see my "archives" link in the right column for all recent posts on oil/energy.) These forces are non-trivial, long-term and deeply embedded in the economy. Online tutoring is not going to make them all go away. Last but not least, as many others have noted, the Treasury may have to raise its bond yield if foreign buyers of Treasuries become reluctant to add to their $1.5 trillion stash of U.S. Treasuries. If you look at the chart of the dollar (yesterday) and the bond chart (today), both suggest that a defense of the dollar is looming. To defend the dollar, the Treasury must raise the yields. Interest and mortgage rates will also rise. As many have noted, this will pressure the housing market rather severely. Why would the Treasury defend the dollar? As I have noted here repeatedly: because they have no choice. We as a nation are living off the purchases of bonds by foreigners. If they hesitate or falter, the Treasury must raise rates to whatever the market demands. There is no Plan B, and the charts are rather clearly indicating this sobering reality. November 27, 2006 This Week's Theme: Beneath the Surface Part I: The Dollar Like many others who frequent this site, astute reader Jed H. has an interest not just in the bursting housing bubble but in all the moving parts which are intertwined with housing: the stock and bond markets, gold and the dollar. Jed was kind enough to send in links to three comprehensive, well-charted articles from safehaven.com: The Coming Collapse in Housing (11/17/06, by John Mauldin) Is the Dow Forked? (11/26/06, by Gary Tanashian) Death Knell of the US Dollar (11/26/06, by Clive Maund) Jed addressed one immediate topic of interest this way: Are the Dow Industrials & the S&P500 "topping out" from a Bear Rally, OR will this ~ 4 year rise from ~ 2003 go on more until spring 2007 ? Jed H.My own view is that "beneath the surface," the Dow and indeed the S&P 500 and the Nasdaq are all setting up for a very nasty, very sharp and very unexpected decline over the next few weeks. Rather than go directly to an analysis of the Dow (let's save that for later in the week), let's look at the dollar, which fell precipitously last week:

Now maybe the dollar's descent was just a burp caused by light holiday trading, but before you accept that standard-issue complacency, take a look at gold as reflected in the HUI index:

Note the many signs of technical strength in this chart: a successful re-test of lows (the classic double bottom), the rise in price above the 200-day moving average, the uptrend from the October low, and the RSI (relative strength) and MACD indicators in positive territory. It's also interesting that the HUI at 340 is a mere 10 points away from a critical level of support/resistance (350). If the index clears that hurdle then a move to previous highs and beyond would appear to be in the works. While gold and the dollar are not always on a see-saw--when one is up, the other is down--it is rather obvious that the dollar's last peak occurred in early October, just as gold hit its nadir. A vast army of analysts have pointed out that 80 is the key support level for the dollar, going back to the late 70s. There will of course be a defense in depth of that support, for if the dollar breaks decisively through 80, there is no bottom in sight. So what factors are at play in the dollar's decline? The standard line at the moment is that the Eurozone's central bank is poised to raise interest rates, just as the consensus (i.e. sure to be wrong) in the U.S. is solidifying around the idea that the Fed will lower the Fed Funds Rate in a matter of months. But there may be other forces at work beneath the surface--for instance, a divergence between China and the other massive buyers of U.S. debt and dollars. The standard consensus holds that China ($800 billion in dollar reserves), Japan ($700 billion in dollar reserves) and the oil exporting nations of the Gulf (uncounted billions in dollar reserves via London and offshore Caribbean banks) have all been propping up the dollar with stupendous purchases of U.S. Treasury bonds in order to keep the foolish American consumer spending freely on OPEC, Chinese and Japanese exports. While there is an undeniable logic to that, it is also true that a weakening dollar actually benefits China in a way that it does not benefit Euroland, OPEC or Japan. Since the yuan is pegged to the dollar, as the dollar plummets, so too does the yuan, making both American and Chinese exports ever cheaper in Japan and Europe. From China's point of view, what's not to like? Sure, their dollar reserves drop in value, but the name of the game for the Party leadership is jobs--as in creating tens of millions of them to provide incomes to tens of millions of restive peasants fleeing rural poverty. So if their dollar reserves drop in value by $100 billion or so, that is a small price to pay for extending their exports to Europe and Japan--two huge markets with which they currently run trade deficits. Japan, Euroland and OPEC, meanwhile, will be hurt by a plummeting dollar. Since oil is priced in dollars, a 20% drop in the value of the dollar means OPEC receives 20% less value for every barrel of oil they sell in terms of non-U.S. currencies. Japan and Euroland still depend very heavily on exports to the U.S. to prop up their own economies, so a drop in the dollar is most unwelcome, as it immediately raises the cost of their goods to the U.S. consumer. To maintain their market share, they'll have to slash their profit margins--also not a happy thought. You've undoubtedly read how top Chinese bankers keep talking about the risks of holding too many dollars and U.S. bonds. Read between the lines, these cautioning statements are actually akin to loud shouting: "We're not going to support the dollar any longer!!" And why should they? If the dollar drops to 80 or under, then China's exports to Europe and the rest of Asia just got cheaper in those markets. And since the yuan is pegged to the dollar, Chinese goods exported to the U.S. are unaffected by the decline in the dollar. A drop in the dollar can only boost Chinese exports--a very welcome prospect to a nation seeking to create 30-40 million jobs a year. As gold tracks a strongly bullish uptrend, it's something to ponder. Disclosure: I own calls on gold and puts on the DJIA. This is a disclosure, not advice. Note: I may be horribly wrong about everything. I offer no recommendation other than this: do not buy or sell securities based on what others recommend or don't recommend. Do your own analysis and make your own decisions. November 22, 2006 What Is the Low VIX Telling Us? Take a look at the Volatility Index (VIX) and the Dow Jones Industrial Average (DJIA) for 2006:

As the VIX drops to a 20-year low, we should wonder: what is this low telling us? Some analysts would have you believe that the low VIX means nothing. But as you can see on these charts, the last time the market topped out, the VIX had declined to a relative low. And conversely, when the VIX jumped, those spikes of high volatility marked the market bottoms. Is a record-low VIX meaningless? Time will tell--but it very likely means something. Extremes tend to reverse at some point, and so we have to ask: if the VIX rises, what happens to stocks? The answer is rather clear: stocks go down. November 21, 2006 Is China a Bubble?  Frequent correspondent Albert T. recently sent in comments and links on the question:

is China's economy a bubble? Here are his thought-provoking comments:

Frequent correspondent Albert T. recently sent in comments and links on the question:

is China's economy a bubble? Here are his thought-provoking comments:

The three articles below did it for me. Excerpt from the first article...Thank you, Albert, for the insightful links and commentary. From what I read, Japan's global manufacturing corporations retain the most critical engineering and production facilities in Japan. This is not happenstance; it's about competitive advantages and the issues Albert raises in his commentary. November 20, 2006 The China Syndrome: Growth at Any Cost  Frequent contributor Michael Goodfellow was kind enough to send this link to an excellent

New York Times article on China's Yellow River:

A Troubled River Mirrors China�s Path to Modernity.

Frequent contributor Michael Goodfellow was kind enough to send this link to an excellent

New York Times article on China's Yellow River:

A Troubled River Mirrors China�s Path to Modernity.

Even occasional readers know that I have often written about China, for its emergence from the dark gloom of the "Bamboo Curtain" and the self-inflicted catastrophe of the Cultural Revolution is truly the "story of the century." (Please see China: An Interim Report and other stories in the left sidebar under "Unfolding Crises: Asia.") The themes I have written about are well-illustrated in this story of the Yellow River: 1. The pervasively gross misallocation of capital in China (for instance, the glorious gambles on massive "international city" centers far from transportation hubs) 2. The distorting influence of corruption (for example, the millions of acres stolen by local governments to be sold at a hefty profit to developers) 3. The possibly uncorrectable environmental degradation which stems from rampant development and corruption (as described in this article and many others, factories which only begin spewing toxins after dark, so they escape "official" notice) The problem is not just China's but the Earth's, for the limits of growth are already upon us. Take a look at this chart and then read this excerpt from this week's Barron's interview with Lyric and David Hale:

Right now, Americans have 148 million cars, the Chinese 19 million. and the Indians, all billion of them, have 9 million cars. By 2050, Goldman Sachs projects the Americans will have 233 million cars, the Chinese will have 514 million cars, and the Indians will have 610 million cars. The Americans with 148 million cars already consume one-quarter of the world's oil.Yes, yes, I know, the miracles of the free market will send the internal combustion, petroleum-based, steel-frame car to the scrapheap of history. But 2 billion cars--for let's not forget to add auto-mad Europe or the rest of Asia to their estimate--is a lot of something, even if it isn't oil or steel: carbon fibers, hydrogen fuel-cells, batteries, or whatever solution you believe will win out. And the energy required to fabricate those technologies will still be stupendous. As a result, we all have a stake in China's rush to modernize and employ its hundreds of millions of previously rural subsistance workers. What is not stated openly (or at least not very often) is this: China only gets one chance to get it right. Right now, global warming is reducing the watershed of the Yellow River. If they mismanage their water assets (rivers and aquifers), they won't get a second chance. If they misallocate all the billions being poured into factories, city centers and infrastucture, there won't be another trillion dollars available to waste on absurd mega-projects or shoddily constructed infrastructure. The global economy will turn to other, even cheaper sources of labor, just as it has always done. China's task (and India's as well) is unprecedented. In the same issue of Barron's, a story covered a University of California at Irvine study which sought to quantify China's competitive advantages: low labor costs, and so on. The article states: Astonishingly, counterfeiting and piracy are worth up to a third of China's gross domestic product, according to some estimates. This makes a government crackdown on a phenomenon which creates millions of jobs exceedingly unlikely.That is putting it politely. If you were one of China's leaders, which would you make a priority: throwing all those counterfeiters of Hollywood movies, Microsoft software, European luxury goods, pharmaceuticals, Japanese motorcycles, etc. etc. etc. in jail, or wink at their "growth industries" as they hire millions of restive peasants? It will be a close race. Can China grow fast and smart enough to satisfy its millions of workers who are currently left out of all the prosperity of the coast? Can they develop sustainable resources before they run out of air and water? Can they do all this before the population ages? (see "Fewer" in recommended books for more on the consequences of their "one child" policy of the past 20 years.) If any of these issue blows up--political unrest, environmental collapse, financial decline--then all bets are off for a stable, prosperous China. A Note to Readers: A large and time-consuming writing project has put a huge squeeze on my time recently, and I apologize to those readers who were kind enough to email me for my tardy replies. My blog entries have also been a bit thin, and may well be sporadic this week as I push to complete this big project and prepare our humble abode for the Thanksgiving Celebration. I am most grateful for hot running water, my mobility, freedom of the press and Internet, having friends and family to join for the holiday--and you, dear patient Reader, who may hail from any one of a 100 nations or a 1,000 cities. Thank you for your continuing readership. November 17, 2006 The Not-So-Famous Lessons of Lord Nelson's Success  This biography does a superb job of providing context and background for Nelson's astonishing rise to fame and his equally astonishing victories at sea--and lesser known defeats, which always occurred on territory unfamilar to Nelson, i.e. land. We find that the extreme risks of Britain's war with Napoleonic France created a brief window of opportunity for commoners such as Nelson to rise within the class-conscious and peerage-dominated Admiralty. Merit was so essential to victory that the Admiralty could not afford to advance captains by favoritism alone. Equally interesting is the author's careful descriptions of the importance of mentors in Nelson's career arc--captains and admirals above him in the bureaucratic Royal Navy who guided, aided and promoted him, not so much to benefit themselves but in recognition of his talents. Yet without these mentors--several of whom he maintained as close personal friends until death--his rise from the ranks of hundreds of junior captains to admiral at a young age would not have happened. Not that Nelson enjoyed a perfect career. A gross political miscalculation--falling under the influence of the King's ne'er do well son, who had been given a position as Admiral not on talent but on birthright--caused Nelson's career to falter at a critical juncture. Having fallen out of favor for his destructive sycophancy, Nelson was sent home without a command, where he languished for seven long years as a poor gentleman landowner. A renewal of the war with France gave him one more chance, and with the aid of his mentors, he assumed command of the Mediterranean Fleet (bypassing many jealous senior admirals), enabling him to score his first great strategic victory in the Battle of the Nile. Life at sea was not easy, and Nelson was often ill and exhausted. Having lost an eye and an arm in two land engagements (he was deployed twice to joint Army-Navy commands, both of which ended badly, partly due to Nelson's ignorance of land warfare), he was often in pain. he also had to make judicious political decisions regarding allies, harrass the Admiralty for supplies, maintain discipline on a huge fleet of wooden ships in poor weather, and a host of other challenges which would have ground down by sheer workload alone a lesser commander. I would like to honor my own stock market analysis mentor, H.I., whom I met via this very blog. Without mentors, few of us can achieve our full potential. So if you're in a position to mentor someone, by all means do so. The American Identity Literary Contest is my own poor attempt to encourage and mentor young writers (see the left sidebar for more about the contest.) Even the most talented individuals still need mentors at critical stages of their careers. November 16, 2006 Recommended Reading: Gavan Daws  If you have any interest in Hawaii, I recommend Gavan's history, which has remained in print for decades: Shoal of Time a History of the Hawaiian Islands.  Once you click on either of these links to amazon.com, you can navigate to Gavan's other titles as well. As always, feel free to read about the books on amazon and then go borrow them from your local public library. November 15, 2006 The Housing Bubble: Made in China and Japan? BusinessWeek's lead article, Can Anyone Steer This Economy? observes that "Global forces have taken control of the economy. And government, regardless of party, will have less influence than ever." While it's true that the U.S. government has little control over the U.S. economy, that's not to say government has no influence. I don't refer to the U.S. government, of course, but the central banks of China and Japan, which have enabled the easy money which fed the speculative fever which created the housing bubble. (See illustration below.)

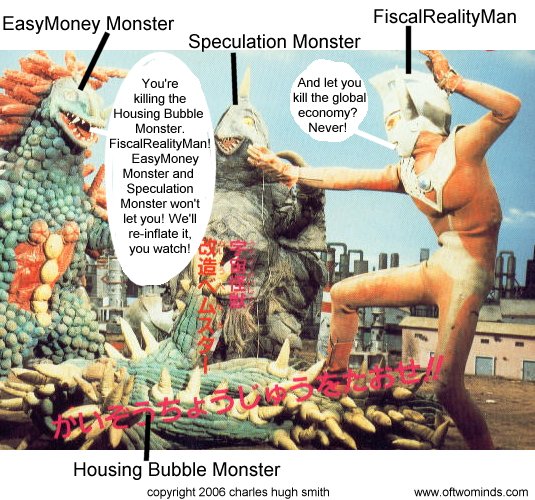

EasyMoney Monster was born from the monstrous marriage of MS (massive liquidity) and LLS (lowered lending standards). Speculation Monster was sired by the union of DSFHYILIW (desperate search for high yield in a low-interest world) and HIASI (housing is a safe investment). By buying U.S. debt in previously unimaginable quantities--over $1.5 trillion in Treasuries alone--the government-run central banks of China and Japan enabled the Fed to lower interest rates to inflation-adjusted zero, fueling a speculative frenzy in U.S. housing. With treasury bonds yielding such low returns (thanks to massive buying of basically zero-return T-bills by the Chinese and Japanese banks), the slightly higher yields on U.S. corporate bonds and mortgage-backed securities looked good to overseas investors and institutions, who then snapped up veritable mountains of private-sector U.S. debt. Since virtually any debt instrument issued in the U.S. is being purchased regardless of yield or risk by foreign banks and institutions (Gulf oil producers' buying has been funneled through London and offshore Carribean banks), there are no brakes on debt creation--or on the speculation such easy money encourages. And why the speculation in housing? In a low-interest world, the yield on bonds is also low, and many investors burned by the dot-com stock market meltdown sought the higher returns and apparently lower risk of real estate/housing. Given easy money, low lending standards and low interest rates, the barriers to entry were lowered to near-zero. No savings? Get a no-down payment loan. Low income? Get a no-document loan. Can't afford the payments? Get an option ARM with low teaser rate and interest-only monthly payments. Is there any wonder these conditions have created a massive speculative bubble in housing? FiscalRealityMan appears to have the upper hand in his battle with the Housing Bubble Monster, but the dynamic duo of the EasyMoney Monster and Speculation Monster will be hard to beat, as long as the Chinese and Japanese governments continue sopping up ever greater quantities of U.S. and lending standards continue to bounce along rock bottom. Why are they absorbing such risky quantities of dollar-denominated debt? To enable the U.S. consumer to keep buying their exports, of course. That strategy has paid off handsomely now for years, but the true cost of the gambit is becoming increasingly obvious: a global speculative frenzy which is blind to risk. November 14, 2006 Up, Down or Sideways? Since I am writing this Monday night, I have no idea what will happen to the stock markets on Tuesday. But here are the possibilities: up, down or sideways. Given the data coming up this week on inflation, sideways seems unlikely, so let's look at up or down. Here's a chart to consider:

Scenario #1 is the Dow runs in a straight line up to 13,000 or more. The trendline is undoubtedly up, and so the argument goes, why bet against the trend? Why, indeed. The counter argument goes: hmm, that's a double top there at 12,196 or so, and the markets are not far from that mighty trendline. Should it dip below, then a retrace to the previous high (in the case of the Dow, 11,723) would be typical for a market in an uptrend (scenario #2). If the market loves the Producer Price Index (PPI) inflation number and October retail sales today, then it could run above the 12,200 ceiling, setting up a run to 13,000. If, however, the market takes a "buy on the rumor, sell on the news" direction and drops below the trendline, then a drop back to 11,700 could be expected. Being a cautious sort, I dumped my call options on the DJIA this morning for a modest profit of 13% for the week and picked up some puts (a bet that the market will decline). The reason is that I engaged a friend's pet simian to toss some darts at the pages of the Wall Street Journal taped to a wall, and this was the result. Truth be told, the monkey's first dart-toss narrowly missed his owner's pet parrot, and the second just skimmed the cat. After some stimulus-response-reward behavioral training, the over-active monkey became less interested in darting his fellow pets and more interested in hitting the stock pages. The results are secret, but I think it is fair to say that only a fool follows a monkey's dart tosses. NOTE: The part about the calls and puts is true, the part about the monkey is fictional. But back when the Wall Street Journal ran a contest between professional stock pickers and a monkey tossing darts, the monkey often beat the pros. November 13, 2006 Doom, Gloom or Boom? Whether you're a confirmed Bull or Bear, it behooves us all to constantly question our beliefs. As I have documented here, I fully expect the housing bubble to burst in a slow-motion crash which will take down the U.S. economy and very possibly the global economy. But being a slow-motion crash, events will take years to transpire. In the meantime, as I have also noted here, Is The Dow Poised to Break Out?, the stock market may follow the pattern set in earlier secular Bear markets by running up in one final sprint before the ultimate collapse in valuations. Let's revisit that thesis. Here is a chart of the Dow Jones Industrial Average. Yes, it is a narrow selection, even an arbitrary selection, of large-cap stocks, but the much broader S&P 500 looks remarkably similar.

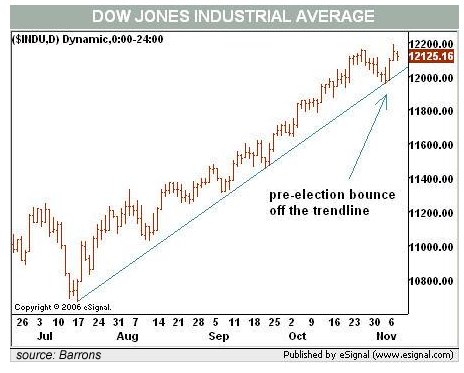

The bulls and the bears are currently engaged in an epic tug of war. As we can see in this chart, the DJIA formed a classic double bottom in July, presaging the massive runup to the present. (Would that I had been smart enough to buy calls back in late July, but alas; at the time, my Bear blinders were firmly in place.) The question isn't, at least to my mind, if the U.S. economy will stumble into a deep recession due to the implosion of the housing debt bubble, but when. Nonetheless, as investors seeking to better our financial place in a dangerous and uncertain world, we must ask: could the market be poised for a final run to the stars? The answer is anything but clear. This chart clearly shows the market is in an uptrend, which is bullish, and that the market has recently bounced off the trendline, maintaining its bullish trend. So far so good. But there is a disturbing double-top formation just below the 12,200 line, which suggests that the bulls' powers are waning.  Could this be the "pause that refreshes"? Some analysts see this as a sign of

strength, as by all rights, the DJIA should have dropped back in a significant retrace

by now--and a logical support level would be its previous high at 11,723.

Could this be the "pause that refreshes"? Some analysts see this as a sign of

strength, as by all rights, the DJIA should have dropped back in a significant retrace

by now--and a logical support level would be its previous high at 11,723.

Instead, the worst that the bears have managed is a brief dip to the trendline, which held as support. This weakness, in other words, has yet to break the trendline. If this is the expected retrace, then the market could be setting up another sharp leg upward. On the other hand, the double top suggests it might be poised to break decisively through the trendline. This week may well provide the data which will trigger either the meltdown through the trendline many expect, or a resumption of the solid uptrend. Either scenario is supported by the charts. Frequent contributor Harun I. kindly sent in this chart, which shows a negative divergence in the MACD (moving average convergence-divergence) and a subtle failure in the uptrend to reach into its upper channel.

What will settle the tug of war? perhaps the inflation and retail sales data due Tuesday and Wednesday. If the PPI and CPI (producer price index and the consumer price index) reveal undertows of inflation, the market might well sell off sharply on fears that the Fed will be forced to raise rates yet again. If retail sales drop through the floor, then the market may well sell off on fears that the dreaded recession is already upon us. If these data (cooked, broiled, poked and massaged as they are) show inflation as a no-show and retail sales as surprising to the upside, that might light a fire under the market. So stay sharp Tuesday. Even if you're only an observer, it should be an interesting week. IMPORTANT NOTE: in the interests of disclosure, please note that this does not constitute a recommendation to buy, sell or even own any security, option, futures contract, pork belly, side of beef, tofu future, foreign currency, quatloos, container of corn or indeed, anything tangible or intangible. I really don't know what's going to happen, so for goodness sake, do not misconstrue this as guidance. It isn't. It's commentary only. You'll have to make up your own mind, based on your own analysis, judgment, intuition, etc. For what it's worth I do hold calls on the DJIA (75 cents each) and NEM (Newmont Mining) (60 cents each) and long positions in APC (Anadarko Petroleum) (at $44) and MDG (a gold mining company) (at $26). But I might liquidate these positions at 9:31 a.m. Monday and go short on something else, do don't put any credence in what I own (or don't own) at any given moment. A monkey throwing darts at a listing of stocks would do as well and very likely much better than I will. But since everyone is supposed to disclose their positions, I don't want to be left out--so there it is, my idiocy is in full view. November 11, 2006 A Partial Answer to National Health Care  Correspondent Jim Twamley (last seen here in my "wheel estate" entry) sent in a

"Partial Answer to National Health Care" from the road. What I like about his

partial answer is 1) that it is partial--no one idea will solve all our healthcare

problems; 2) it employs market forces, and 3) it eliminates insurance claims and all

the paperwork which chews up 30% of all the money spent on healthcare. By offering

basic medical services on a cash basis, it encourages people to only spend money on the

care they actually need, as opposed to the "free" care paid by insurance--which is anything

but free to the employers and government.

Correspondent Jim Twamley (last seen here in my "wheel estate" entry) sent in a

"Partial Answer to National Health Care" from the road. What I like about his

partial answer is 1) that it is partial--no one idea will solve all our healthcare

problems; 2) it employs market forces, and 3) it eliminates insurance claims and all

the paperwork which chews up 30% of all the money spent on healthcare. By offering

basic medical services on a cash basis, it encourages people to only spend money on the

care they actually need, as opposed to the "free" care paid by insurance--which is anything

but free to the employers and government.

As you know my wife and I travel in our RV full time. As a result we see and experience many things that others do not. Not only do we see the normal tourist sites but we also observe people, communities and trends. One of the trends that I intend to invest in at its future IPO is what I call "drive through health care."Thank you, Jim, for the thought-provoking observations and commentary. Low-cost treatments which are paid in cash certainly seem like part of the total solution. P.S. In honor of Veteran's Day, I want to mention that Jim is a retired Navy Chaplain. November 10, 2006 Friday Quiz: Where Is This?

Where is this? Send me the answer and I'll send you a free copy of my novel I-State Lines. Hint: this locale is not in Japan or Hawaii; it's in the continental U.S. Wow! My email has already lit up with winners: this is the Japanese Garden in the Huntington Library, located in San Marino, California (adjacent to Pasadena). There is a Chinese garden currently under construction which will be quite authentic. Thanks to everyone who already sent in an answer. November 9, 2006 Financial Survival Now that the political circus has ended, let's return to what is beyond the control of the Federal government in whatever political configuration you assemble: the global economy and its impact on our individual financial future. Reader D. Tofel asks the question we all face very succinctly: Many, many thanks for your insightful articles. I have found myself making the same observations and wondering why I was the only one seeing the insanity in the real estate market and elsewhere. I have also been following the peak oil issue very closely.This gets right to the core issue: financial survival. Let's start with what we know: 1. No one can predict the future. If this were easy, we'd all be millionaires. 2. "The trend is your friend." Markets have a way of rising and falling in long-term trends which often make no sense in terms of fundamentals like value and earnings. But betting against the trend is a good way to lose your shirt--no matter how right you may be about its unsustainability. The housing bubble is a good example. I wrote an article for the San Francisco Chronicle back in 2004 calling for a top in housing. The bubble promptly expanded for another year and a half. My point: the trend runs until it stops and then reverses. Trying to call the top before it is visible is a fool's errand. (As I so ably proved.) 3. No one can predict the ultimate top or bottom in any market. No one predicted in 1995 when the Nasdaq topped 1,000 for the first time that it would run to 5,000 in a mere five years, just as no one in 1996 predicted house prices would triple in California. And of course no one in 2000 predicted Nasdaq would fall to 1,100 within 2.5 years. 4. Those who make money buy when no one else is buying. Those who lose money buy when everyone else has already bought. For instance: housing sales were slow in 1996; no one was buying 3 or 4 houses to speculate on rising prices. Gold and oil stocks were at multi-year lows in 2000, as the feverish buying was concentrated in technology stocks. Those few souls who bought gold and oil stocks instead of technology stocks are now wealthy, while everyone who bought tech stocks (and didn't get out in March 2000) lost their capital. 5. Understanding the reasons behind the trend is less important than getting the trend right. The whys and the wherefores of the oil and gold markets in 1999 - 2001 were debatable, but the beginning of a new uptrend was not. 6. The real financial harm comes not from missing the latest "get rich quick" idea but from the destruction of capital in a losing bet. The person who sat out the housing bubble did not rake in $100,000 from flipping a few homes in the last manic rise of 2004-2005, but then on the other hand, they are also not facing foreclosure and bankrupcty on the 4 homes they bought in 2005 (to flip for vast profits, of course) in 2006. Investors like Warren Buffett who sat out the dot-com bubble looked like idiots in 1999 and geniuses by 2002. Yes, Buffett passed up massive profits, but he also preserved his investors' capital while others lost trillions. So what trends are visible? Let's look at some charts.

Here we see a proxy for the housing market, the homebuilders' index. The uptrend has reversed and a downtrend is in place. Since no one can predict the bottom, prudence suggests avoiding the housing and real estate markets until the downtrend ends. That will only be apparent after a new uptrend has become visible.

Even if you are convinced that the U.S. economy is about to implode (as I am), the trend in the Dow Jones Industrials is solidly up. How long the uptrend will last, or when it will reverse, is unknown. In general, such a breakout is bullish.

The bond market has formed a wedge. It could break up or down. Prudence suggests awaiting for the break to occur, i.e. waiting for a trend up or down to become visible. In the meantime, bond investors won't lose their capital owning short-term (90-day or 6-month) Treasury bonds.

Here is a 10-year chart of the CBOE gold index. Note the downtrend, the uptrend, and the current wedge. Again, prudence suggests waiting for the wedge to break up or down rather than deciding ahead of time which way it "should" go. The current uptrend suggests the wedge will break to the upside, but again, the future is unknown. The presence of wedge formations in both bonds and gold suggest that the level of uncertainty about the future is high. Markets dislike uncertainty, so it's prudent to wait for the trend to become visible. Regarding yesterday's post on derivatives, frequent contributor Harun I. had this recommendation for further reading on the subject: You post today was great. I would strongly recommend to every one of your readers to read copy of When Genius Failed: The Rise and Fall of Long-Term Capital ManagementThank you, Harun, for the insightful comment and recommendation. To sum up one possible answer to D. Tofel's excellent question: What can I as an individual do to survive? Avoid risky markets, be prudent in preserving your capital, and don't bet against the trend. November 8, 2006 Derivatives and the Real Estate Bubble  Reader Kenny G. posed a fascinating question about the impact of derivatives on

the housing bubble:

Reader Kenny G. posed a fascinating question about the impact of derivatives on

the housing bubble:

"My question is this: How will the huge amount of credit derivatives play out in way of the deflating of the bubble? I hate to say it but, "this time MAY be different"? I have read that there was about $1 trillion worth as little as 5 years ago and now there is in excess of $27 trillion. Will the need to put this "money" somewhere give this market a true early floor or will there be some unwinding that will create an even worst result?Though no expert, I'll do my best. There are at least three parts to the answer: the impact of mortgage-backed securities derivatives, the growth of derivatives across all financial markets, and the demand for a "home" for excess capital. The scale of derivatives appears to be fully 10 times greater than $27 trillion; according to The Economist: "Finance has been convulsed by a computer-enhanced frenzy of creativity. In today's caffeine-fuelled dealing rooms, a barely regulated private equity group could very well borrow money from syndicates of private lenders, including hedge funds, to spend on taking public companies private. At each step, risks can be converted into securities [like mortgage-backed securities], sliced up...re-packaged, sold on and sliced up again. The endless opportunities to write contracts on underlying debt instruments explains why the outstanding value of credit-derivatives contracts has rocketed to $265 trillion � $9 trillion more than six months ago, and seven times as much as in 2003."Derivatives have also skyrocketed in value in the past 5 years as the need to take on more risk has increased. The demand for superior return in a low-interest environment has driven the capital markets into accepting more and more risk in an attempt to "beat the market" or do better than a safe 6-month Treasury note. (Recall that "risk and return" are related; the lower the risk, the lower the return, and vice versa.) To offset the greater risks, money managers have turned to derivatives for portfolio insurance.

Here's (basically) how a derivative works. (Skip this if you already know.) The simplest way to grasp a derivative is to consider put and call options on a stock or index. Let's say you invest a whopping chunk of money in XYZ Corporation which trades at $50 a share. To protect yourself against a sudden collapse in the value of XYZ shares, you buy put options, which increase in value as XYZ drops. If you own 10,000 shares of XZY, that means you've got $500,000 invested. If you buy contracts for 10,000 shares (options come in contracts of 100, so this means you'd buy 100 contracts) for, say $1 a share, then you'd spend $10,000 to protect your investment against a massive drop. Say your put was at a strike price of $50; if XYZ plummeted to $40, your put options would be worth $10, or the difference between the strike price and the current price. Even though your shares have lost $10 in value, your put gained $10 in value. So you've suffered no loss despite the steep drop in XYZ's value. If XYZ stays at $50 or goes up, your option expires worthless, which means the party which wrote the option pockets the $10,000 and you receive nothing--very much an insurance policy. But your worst case scenario was effectively reduced to the cost of the puts: you couldn't lose more than $10,000, even if XYZ stayed at $50/share. Now this may sound confusing, but the reason why no one worries too much about puts and calls unraveling is to write such an option, you need to own or at least control the underlying security. In other words, there is collateral for the "insurance" being sold. Not so with all derivatives. In more exotic derivatives, the potential loss to the firm issuing the derivative is covered by another derivative. Thus, derivatives are swapped, layered, chained and intertwined so that every potential loss is covered by another derivative. If everything stays stable, then the firm writing the derivative pockets the fee and pays out nothing. Issuing derivatives is highly profitable, and seemingly safe. Major investment houses may juggle several hundred derivatives contracts at any one time, thereby balancing all the (visible) risks of their portfolios. So what can go wrong? Somewhere down the chain, if someone didn't adequately cover their risk, some shock in the financial system may cause a loss they can't cover. They go belly up, and as a result the firms expecting these guys will pay off their derivative bets find their "insurance" just became worthless. They in turn may find themselves short of cash to cover derivatives they wrote, and then they have to sell hard assets such as stocks and bonds to cover the losses. Such selling may well trigger additional selling, which will trigger more derivatives claims, which launches yet more selling... and that's how the entire "safe" structure could collapse in giant waves of selling. Here's how derivatives impact the housing bubble. Small-town bankers still write mortgages and keep the "paper," meaning they actually own the mortgage and collect the principal and interest payments from the homeowner. But most of the hundreds of billions of sub-prime and option-ARM mortgages written in the past few years have been aggregated into vast pools of mortgages which are then sold much like bonds. These mortgage-backed securities (MBS) are often tranched (sliced and diced) into various levels of risk. The buyers then offset the risk by purchasing derivatives which will increase if the underlying mortgages go south (i.e. become non-performing loans as the homeowner defaults and stops paying the mortgage). Here's a chart showing the recent rapid rise in MBS:  To connect the dots, scroll back up and look at the chart which shows that 10% of U.S.

households are in danger of defaulting on their debt: (the chart is from the FDIC;

in other words, this is a Federal agency's assessment of the risks.)

To connect the dots, scroll back up and look at the chart which shows that 10% of U.S.

households are in danger of defaulting on their debt: (the chart is from the FDIC;

in other words, this is a Federal agency's assessment of the risks.)

Let's say "only" 5% of homeowners default--that's some 4 million mortgages. Those mortgages are spread out in MBS all over the planet, and as millions of people stop paying their principal and interest (each one goes to a different tranch, by the way), then the owners of those MBS start collecting less income. The value of their mortgage security plummets, as who wants to buy a mortgage-backed security which is receiving fewer dollars every month? Derivatives written against all these MBS will then increase in value, and somebody will have to make huge payouts of cash to cover the decline in the value of the MBS. To raise the cash, they either need to collect from another derivative bet they themselves made or they need to sell the underlying MBS. But the mortgage-backed security has lost a big chunk of its value, and buyers may well be scarce. Maybe the writer of the derivative will have to sell some other asset to make good--like a stock or bond. Any way you cut it, losses will be gigantic if 4 million U.S. households default on their sub-prime or option ARM mortgages. And it is at least conceivable that the unraveling of the MBS and CDO derivative markets could trigger an ever-widening circle of unraveling. This is more or less what threatened the entire global banking system in 1998 when the highly leveraged bets (read: derivatives and options) placed by the firm LTCM (Long-Term Capital Management) started unraveling. If you recall our option example above: $100 million (not much money in today's world) could very easily control or expose to meltdown $1 trillion in underlying securities, bonds and stocks. The industry claims risk has been banished; mathematician Benoit Mandelbrot disagrees. I never tire of recommending his book The Misbehavior of Markets I have no doubt that money is still seeking a "home" in real estate--just as inflows rose to record highs as the dot-com stock market reached its final highs. The willingness of money managers to throw in "new money" on "bets" that paid off handsomely in the recent past (i.e. real estate) is well-known--as is the resulting crash and destruction of the wealth they controlled (Nasdaq 2000-2002, down 80%). The key take-away here is this: With the explosion of mortgage-backed securities and the steep rise in appetites for risk (such as sub-prime mortgages), the housing market has become inextricably intertwined with global financial and derivatives markets. Thus the unraveling of the housing bubble may well trigger the unraveling of the entire global derivatives markets. For more on this subject, I recommend two articles: As Home Owners Face Strains, Market Bets on Loan Defaults New Derivatives Link Fates Of Investors and Borrowers In Vast 'Subprime' Sector (WSJ) If Credit Market Tightens, CDO Boom Could Go Bust (NY Sun) (see chart of CDO explosion at the top of this entry.) November 7, 2006 I Am a Member of an Absurd Elite  What elite do I have the honor of belonging to, and why is it absurd? The elite is

those Americans who vote, and it is absurd because it is an elite not of privilege but

one granted by the passivity of non-voters.

What elite do I have the honor of belonging to, and why is it absurd? The elite is

those Americans who vote, and it is absurd because it is an elite not of privilege but

one granted by the passivity of non-voters.

Exit polls suggest that the segment of the population with the highest voter turnout is Caucasian citizens over the age of 50. Since I am Haole and 52 years of age, I belong to this elite: "Baby Boomer and up" white folks who vote. The lowest voter turnouts as a percentage of eligible voters tends to be young people of all ethnicities. From the point of view of someone who proudly voted at age 18 in 1972 (for McGovern) and in every election since, this is an intolerable abandonment of political power. But voting is just like eating vegetables or donating time to the community or any other activity which is not enforced: no one makes you do it. As a carpenter, I worked with a great number of blue-collar guys over the years. Most did not vote, stating lame old cliches like "don't vote, it only encourages them" or "it doesn't make any difference who wins" to justify their lethargy. But it does matter, and I can point to an issue which is entirely political in nature yet impacts every American: healthcare. I don't want to get into the debate at this point, but even if you disagree as a matter of policy with a National healthcare system akin to Japan's, anyone willing to deal with facts and not ideology is appalled by the waste (30% thrown away on paper shuffling), gross incompetence (needless procedures, horrendous malpractice expenses) and sheer injustice (46 million with no insurance whatsoever, emergency rooms shutting down, bankrupted by the costs of treating the uninsured, etc. etc. etc.) It is a fact that we as a nation spend more per capita than any industrialized nation on healthcare but are far less healthy in terms of chronic diseases like diabetes. (Speaking of Japan: Have you heard any talk about how that national healthcare system is poised to bankrupt that nation of rapidly ageing citizens? Why not? Could their system be much more efficient and less costly than ours?) The solution to our healthcare fiasco is political, and the shape of that eventual solution depends on who controls Congress. Yes, yes, it's often a matter of whose special interests are better represented, but if the citizenry kicked out the current raft of bums and then did so again two years hence if they came up with a healthcare plan which served the trial lawyers, HMOs, hospital corporations and the AMA, the politicians would get the message: quit jerking around and get it done. But if nobody votes them out on their plump duffs, then it's "business as usual." It wasn't always this way. In the past, most citizens voted. Read this feature from the October 16 Wall Street Journal for more: Why Don't Americans Like to Vote? Politics Are Only One Reason If you're an American who is not planning to vote Nov. 7, join the crowd. In the past few decades, less than 40% of eligible voters in the U.S. have bothered to cast ballots in midterm elections.What's the connection between Election Day and the photo above? It's my personal history anecdote showing the power of even a few thousand votes. I was once one of the Triumvrate of The People's Party of Hawaii, a third party which sprang gloriously to life in the early 70s in Hawaii, along with a bumper crop of other off-beat splinter parties. (The Triumvrate was Jeff Blair, Dexter Cate and myself. Ken Ellingwood and Tony Hodges added their considerable talents in 1976.) In 1974, our candidate for U.S. Senate was every conservative's nightmare: a wild-bearded hippie who literally worshipped marijuana, going to court to win the right to use marijuana in his religious ceremonies (Unsurprisingly, he lost. Alas; it would have become a very popular religion.) The Republicans, roiled by the Watergate scandal, didn't even dredge up a candidate to oppose Senator Dan Inouye. So they voted for our guy, the wild-bearded hippie. We received, as I recall, over 40,000 votes. Though this was not enough to send Mr. Kimmel to the Senate, as 10% or more of the votes cast, it did maintain our legal status as a registered political party, which meant we didn't have to collect thousands of signatures to run a slate of candidates in 1976. And as a result, we were empowered to bring new ideas and candidates to the voters. Those votes for the People's Party candidate mattered. Look at this photo of our weekend braintrust meeting. Eat your sclerotic little heart out, Karl Rove! It's true: third parties have more fun. I predict national healthcare will finally be addressed when middle-class voters start getting their healthcare in the overcrowded emergency rooms along with the poor folks. In the meantime: heads up, young people. If you give up your political power so easily, expect to be ignored. You "voted" to be ignored whether you realized it or not. November 6, 2006 Astra Zastra's New Medication: Discolegato I just wanted to say that I enjoy your essays. I was a reader for a while then I got side tracked, lost the bookmark etc....Then when I wanted to revisit I couldn't for the life of me remember the site. To the chase....I was watching TV and that astra zeneca ad came on and the light bulb flashed! I typed astra zastra into google and I have returned.

click here to find out more about Zombiestra and Quattro-Polar Disease. November 4, 2006 More Reader Reports on the Housing Bust My parody of the debt bubble yesterday generated few comments, and I am wondering if it's because the core point--that the true bubble is not in housing per se but in the lax lending which drove up housing prices--is painfully obvious to all. Here's a fascinating range of housing-related commentaries, links and stories from readers. First up is reader Tom K. with a story about a state prison parolee by the name of Taiwan Lee who bought three houses in Colorado for $1.9 million: I think the "new math" is: No documentation + No income verification + (probably) No money down = Taiwan Lee + cash back at close. Check out this story, but be forewarned you might be gasping for air so remember to breath! By the way, it's part of a series... so yes, incredible as it may seem, there's more...Next up, a link from from reader Ben Z. with a startling chart which suggests the U.S. economy will tank in 2007: This story is worth checking out, especially the "Just a Coincidence" graph:Reader Aaron K. sent in a sobering report of a conversation he overheard between a realtor and potential home buyers: Yesterday I was sitting at the local Starbucks, out on the deck reading the paper, and realized after a few minutes that the three people at the table next to me were a couple and a real estate agent in a home buying transaction. I perked up when I heard the real estate agent (who was white) say to the couple (who were black) that interest rates would be going down (implying the home value would go up, or maybe that payments would go down, if the loan was an ARM).Reader M.P. provides this commentary and analysis on the role of rising property taxes in the cost of homeownership--a topic I have covered several times, including Post-Bubble Blues: Derailing the Property Tax Gravy Train (April 6, 2006) Bubbling Property Taxes (April 13, 2006) Have You Checked Your Property Taxes Recently? (April 17, 2006).... just read the "The Housing Market - Plateau of Denial" and had a few thoughts of my own.In reference to my Oct. 18 entry on the HGX-Homebuilders Index, The Housing Bottom is Now--Or Not, reader Thomas B. Storey offered this perspective on the "bottom" which is being called in housing stocks by various pundits/cheerleaders: Just a note on housing stocks. Shorts are prevalent. They will impact the down trend in their own way.(CHS NOTE: Toll Brothers is a national homebuilder, ticker symbol TOL. The stock is down from a January 2006 high of $39.98 to its current price of $28.23.) Thank you, readers, for an enlightening array of topics, sources and commentaries. November 3, 2006 The Solution to the Housing Bust: The 60-year Mortgage In a bid to stem the crumbling value of U.S. housing, the Coalition to Rid America of Surplus Savings (CRASS) has announced the launch of a new loan product: the 60-year mortgage.

The new product's innovation, says Spokesperson I. (Ibogaine) Lyeahlot, is a 20-year fixed rate of 1%. The loan reverts to an interest-only mortgage in the second 20-year period, and the principle and interest are paid off in the final 20-year period. "We're taking our cue from Japan," Lyeahlot explains. "They dropped their interest rates to 1%, and look how great they're doing now." "At 1% interest for 20 years, you pay only $416 a month to own a $500K home for half your adult lifetime," he explains. "Sure the mortgage climbs to $1 million by the end of that period, but hey, one of your kids will probably get a job at the Youtube of the day and rake off a million or two in stock options, so why worry? And if your kids don't make the big bucks, maybe their kids will. We have faith that our grandkids will step up to the plate and pay down these mortgages." The only catch, he reports, is that couples who fail to procreate or adopt children (one is considered a risk factor) will have their mortgages called. "It's good for America," he says. "We need to keep our birthrate up, and this will do the trick." Critics denounce the new debt instrument as yet another off-loading of debt onto our grandchildren, a charge Lyeahlot accepts and defends. "Look, we're already off-loading the Medicare and Social Security debt bombs onto our grandchildren. Why not load the nation's mortgages onto the pile, too? But in the meantime, these loans will spark a whole new round of rising house prices. When the sky's the limit on debt, the sky's also the limit on housing values." Other critics wonder how such a mortgage can win investor backing, given the likelihood of default at the 40-year juncture, when the payment jumps up to cover both interest and principle, Lyeahlot says, "There's already huge interest in these loans from bankers and investors. So the house reverts to the lender in 40 years--so what? Everyone's made so much money by then that it doesn't matter. Nobody cares. Even the original buyer doesn't care--they're either in a retirement home or in an RV." Lyeahlot countered the criticism that homeowners who put nothing down and pay 1% interest, allowing the rest of the interest to add onto the original mortgage, will have no equity. "Sure, the homeowners will have no equity. In fact, they'll be underwater to the tune of a half a million bucks. But so what? They will have the illusion of ownership, which is all they really have now. So what's the difference? They feel like they own something, and that pride of ownership is what these loans are all about." As for why anyone would buy a 20-year mortgage which only paid 1%, he explained, "The money's not in the interest--it's in the derivatives which will be written against the tranches. The actual interest is, pardon the wordplay, of no interest. With derivatives, an investor can leverage the 1% into a position with 10 times that return." Given that a significant majority of total U.S. debt is being purchased by foreign entities and central banks, some claim that by the end of the 60-year mortgage, when our grandchildren will finally make the last payment, China, Japan, the oil exporting nations, Canada (in trade for tar sand oil) and Mexico (in trade for low-cost labor) will own the entire U.S.A. In response, Lyeahlot sniffed, "So what? Our savings rate is already negative and what difference does it make? We live better than the people who own all our mortgages and bonds and all that stuff. Let 'em buy up the assets--we still get to live in the mansions. Savings are so 20th century." Lyeahlot reports that CRASS is also considering launching a 90-year mortgage next year, "We thought about a round 100-year time frame, but that seemed to scare people, so we dropped it back to only 90 years. We think it's going to open new territory in truly long-term debt packages. The derivative opportunities are just huge." November 2, 2006 Could the Dow Jones Industrials (DJI) Be Poised to Break Out? In my Oct. 21 entry The "Record" Dow Jones Industrials--A Clear-Eyed Look, I indicated that the new highs in the DJ-30 were rather suspect, as relatively few of the stocks had hit new highs. But if we look at a 10-year chart, another view emerges. As long-time readers know, I believe the evidence suggests the bursting of the housing bubble has already mortally wounded the current run of U.S. "prosperity." But the stock market has often proved that it exists in a parallel universe with few ties to the "real economy." We may be in just such a disconnect. In my Oct. 6 entry, Do Your Trust This market Rally?, I took a skeptical view of the current rally. But if we look with unprejudiced eyes at the chart below, we see a powerful uptrend in place:

Note that the DJ-30 has broken multiyear resistance and is rising above a multiyear channel. The uptrend since March 2003 is very much in place. Am I still skeptical of the staying power of this rally? Yes. The wheels will fall off the economy at some point, perhaps as early as the first quarter of 2007, but in the meantime there are reasons to suspect the rally will extend beyond this week's retrenchment: 1. The vast majority of mid-term eelction years have experienced a Q4 rally. 2. Sentiment is now bearish/negative/skittish--the opposite of the euphoria/widespread bullishness which marks a market top. 3. With the housing and energy sectors in well-publicized declines, there is reason to believe money might continue flowing to the "safe" large-caps in the Dow and S&P 100. 4. If the "trend is your friend," there is reason to be on the long rather than short side of this chart. 5. Perhaps we are in an era analogous to 1973, when the DJ-30 shot up to a new high just before plunging into a grinding, multiyear Bear market. Take a look at this chart:

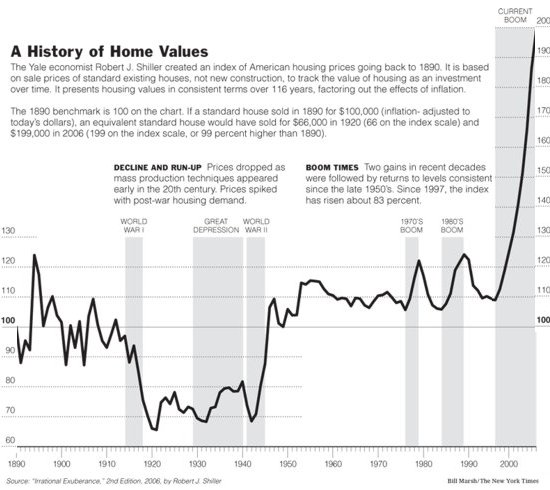

What powered the market to new highs in an era with so many warning signs of impending economic malaise? The same conditions which apply now: supreme complacency, momentum, wishful thinking, to name just a few. Will the market drop precipitously now that I have suggested it might make one more powerful lep upward? Possibly; but all we have in the way of predictive tools is factual displays of data, i.e. charts, so make of them what you will. November 1, 2006 Stories from the Front Lines of the Housing Bust Let's start with a "ground zero" report from astute reader David S. in Florida: I'm at ground zero here in SW Florida and I have personally seen dozens of mostly empty subdivisions within a 25 mile radius. This mess is going to end up worse than ugly, with the end result a bad recession if not depression. One thing that really disguises the current huge drop in sales price is the misuse of MEDIAN price to reflect price drops.Thank you, David, for highlighting the inadequacies of "median home prices." (Sharp-eyed reader Anton S. pointed out my confusion of "median" and "mean". I had written "This number can also be skewed by a handful of very expensive sales, which effectively raise the median price." As Anton observes: "Mean price is skewed by a handful of expensive sales, Median is NOT, and thus it is a preferred 'average'.")

chart courtesy of Michael Goodfellow Next up, a report from knowledgeable reader Todd N. in southern California: In your latest piece you write, "Let you imagine that I have made up the first stair down..." and then quote the LA Times piece from Friday. Here's another bit of evidence: builders offering $100,000 off if you close by the end of the year.Thank you, Todd, for this frontline report on the "$100,000 discount"--a number I have heard in other first-hand accounts from the overbuilt areas around Sacramento. (And such a nice round number it is, too.) Please see the October 30 entry "39 Steps" for background--the link to October entries is at the bottom of this column. Frequent contributor Michael Goodfellow sent in these links to excellent charts of the housing bubble here in the U.S.: California Housing Prices Inflation-adjusted Housing Prices (U.S.) 100-Year History of Housing Prices (reprinted above)