|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | |||||||||||||||||||||||||||||||||||||||||

Writing/Film Dear Aspiring Writers: The Worst Advice You'll Ever Read A Literary Look at I-State Lines Spirited Away: Decay and Renewal An American Poem (Robinson Jeffers) Taoist Chinese Poems 11 more in archive Recommended Books American Identity Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Cultural Commentaries On Hatred and Anti-Americanism Anti-Americanism Part 2 Anti-Americanism Part 3 French-Bashing Kroika! Chronicles This Blog Sells Out Doom and Gloom Sells The Kroika Mascot-"Auspicious Pet" Wal-Mart and Kroika Kroika and Starsbuck Take a Hit Kroika Ad 1 Kroika Ad 2 Kroika Ad 3 Kroika Ad 4 Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Corruption and Avian Flu: China's Dynamic Duo Exporting the Real Estate Bubble to China Is the Bloom Off the China Rose? 9 more Battle for the Soul of America Katrina, Vietnam, Iraq: National Purpose, National Sacrifice Is This a Nation at War? A Nation in Denial Why Is This Such a Tepid Time? That Price Isn't Cheap, It's Subsidized U.S. Fascists Seek Ban on Cancer Vaccine The Truth About Christmas 10 more Financial Meltdown Watch What This Country Needs Is a... Good Recession Are We Entering the Next Age of Turmoil? Doubling Down on 5-Card No-See-Um A Rickety Global House of Cards Are Japan and Germany Truly on the Mend? Unprecedented Risk 2 Could One Rogue Trader Bring Down the Market? Worried about Inflation? Stop Measuring It Economy Great? Bah, Humbug Huge Deficits and Huge Profits: Coincidence? Who's The Largest Exporter? Three Snapshots of the U.S. Economy 21 more Planetary Meltdown Watch The Immensity of Global Warming Sun Sets on Skeptics of Global Warming Housing Bubble Watch Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Hidden Costs of the Housing Bubble Housing Market Slips Toward Cliff Housing Market Demographics Oil/Energy Crises Whither Oil? How much Is a Gallon of Gas Worth? The End of Cheap Oil Natural Gas, Naturally High Arab Oil Money and U.S. Treasuries: Quid Pro Quo? The C.I.A., Oil and the Wisdom of Crowds The Flutter of a Butterfly's Wings? A One-Two Punch to a Glass Jaw Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds Geezer Rock Overload In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono One-Word Titles Complacency Nostalgia Praxis Keys to Affordable Housing U.S. Conservation & China Steve Toma, Me & Skil 77s: 30 years of Labor Real Science in the Bolivian Forest Deforestation and Sustainable Forestry The Solar Economy (book) The Problem with Techno-Fixes I Love Technology, I Hate Technology How To Blow off Web Ads and More Health, Wealth & Demographics Beauty of the Augmented (Korean) Kind Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Is Obesity an Inflammatory Response? Demographics & National Bankruptcy The Decline of Europe: A Demographic Done Deal? Landscapes Selling the Landscape The Downside of Density Building Heights and Arboral Roots Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Nourishment The French Village Bakery Ideas What Is Happiness? Our Education System: a Factory Metaphor? Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi Splogs, Blogs and "News" "There is no alternative to being yourself" History The Strolling Bones: Rock of Ages Bad Karma: Election Fraud 1960 Hiroshima: First Use All the Tea in China, All the Ginseng in America Friday Quiz Quiz #1: Pet Obesity Essential Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So Fewer: How the New Demography of Depopulation Will Shape Our Future The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal The Future of Life Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies The Solar Economy: Renewable Energy for a Sustainable Global Future The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Recommended Books More book reviews Archives: weblog February 2006 weblog January 2006 weblog December 2005 weblog November 2005 weblog October 2005 weblog September 2005 weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

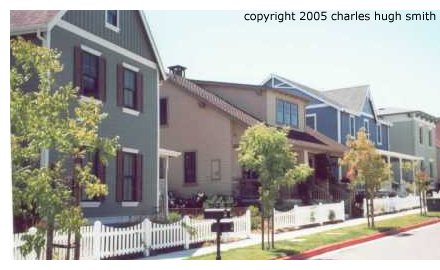

Please scroll down to 3/29 for "The Five Stages of a Housing Bubble" March 31, 2006 Hidden Costs of the Housing Bubble  An akamai (Hawaiian for astute) reader pointed out an enormous financial burden being

placed on non-wealthy homeowners by the housing bubble: rising property taxes. Revenue-hungry

cities and counties are re-assessing all real estate at new, bubble-era prices, and

adjusting the property taxes skyward accordingly. I have heard anecdotal evidence of this in locales

ranging from Virginia to Hawaii.

An akamai (Hawaiian for astute) reader pointed out an enormous financial burden being

placed on non-wealthy homeowners by the housing bubble: rising property taxes. Revenue-hungry

cities and counties are re-assessing all real estate at new, bubble-era prices, and

adjusting the property taxes skyward accordingly. I have heard anecdotal evidence of this in locales

ranging from Virginia to Hawaii.

It is possible, of course, to lower the assessed value of your property after the housing bubble bursts, but cash-starved municipalities do not necessarily make that an automatic process. Generally, you have to fill out a form and then wait months for the re-assessment to occur. Given that other revenue streams will be in sharp decline during a recession, the assessors' office will no doubt be instructed to be rather parsimonious in handing out lower assessments. The net result: all property owners will be paying for the housing bubble via much higher property taxes. Some states, including that well-known tax haven, California (that's a joke, folks) have limits on assessment and property tax increases (i.e. Prop 13 caps): it is 1% a year here in the Golden State. That's all well and good for property owners who bought long ago, but what about recent buyers? The absurdly inflated property taxes they are paying as a result of the housing bubble exacerbates the huge inequality that exists between those who bought cheap decades ago and recent buyers. The oldsters' property tax might be $600 annually, while their new-buyer neighbor is saddled with a nearly $10,000 annual tab. These are not invented numbers, but actual numbers from our own town. This, mind you, is for a wretched, should-be-bulldozed "fixer-upper" in a blighted neighborhood which sold for over $400,000. For a fixer-upper in the oh-so-desirable Berkeley Hills, well, that's an $800,000 price tag, which in high-tax Berkeley translates into an annual property tax bill of almost $20,000. $1,600 per month just to pay property taxes and other local taxes? (mosquito abatement, bond issue for new library, etc. etc.) By any sane measure, that would be enough to pay the mortgage, fire insurance and taxes. Do I heard chortling from deep within the bowels of City Hall?  Another pernicious fallout from the housing bubble may be rapidly rising "official" inflation rates.

As I have pointed out here before, the Federal government's method of calculating inflation has long been

manipulated in order to keep it low by under-estimating medical and housing costs.

Another pernicious fallout from the housing bubble may be rapidly rising "official" inflation rates.

As I have pointed out here before, the Federal government's method of calculating inflation has long been

manipulated in order to keep it low by under-estimating medical and housing costs.

Housing, fully 40% of the weight in the calculations, is based solely on rents, which have plummeted 20% nationally as the housing bubble inflated and millions of people switched from renting to owning. Fully 70% of the populace now owns their own home. But does the consumer price index reflect higher property taxes, or the effect of rising interest rates on all those holding adjustable-rate mortgages? No, for it doesn't consider the costs of homeowners at all. One effect of the bursting of the housing bubble will be rising rents as construction of new housing dries up and people begin losing their homes. Yes, rents will stay cheap in over-built exurbs like Manteca, CA, where there's 7,000 new houses in the pipeline and zero new buyers; but if you're going to rent, why put up with a 4-hour commute each day to get home? Not only that, but even those exurb rents won't stay cheap. As desperate gamblers (oops, I mean "investors") realize that rents will never cover their costs and their "investment" will remain a gaping hole in their cash flow forever, they will join the flood of foreclosure refugees who have given up their homes and voted with their feet. Banks are notoriously wary of becoming landlords; they would rather dump a property for 60 cents on the dollar than try to rent out and maintain hundreds of homes. So the reality will be hundreds of locked-up houses awaiting auction, and growing demand for rental houses in conveniently located neighborhoods. As people exit the shattered Paradise of homeownership, increasing demand for rental housing, landlords will only be too happy to respond with incrementally higher rents. (Recall that since they've taken a 20% hit since 2000, from their view they're simply getting back to level ground with a 20% increase in rents.) This will show up in the CPI, causing inflation to rise even as the economy falls deeper into recession--an apparent conundrum, as costs usually fall when demand for goods and services falls. This will be the bad karma consequence of manipulating the calculations to make inflation appear low all these years. This entry is an updated version of an October 2005 story on the same subject. March 30, 2006 Trade with China: Making Out Like a Bandit  The protectionist hysteria gaining mindshare in Congress may be good politics

to some, but it overlooks one simple fact about U.S.-China trade:

the U.S. is making out like a bandit.

The protectionist hysteria gaining mindshare in Congress may be good politics

to some, but it overlooks one simple fact about U.S.-China trade:

the U.S. is making out like a bandit.

What supports this shocking statement? Everything. If anyone has cause to get sore, it's the Chinese, and here's why.  Just how profitable are U.S. companies having their products made in China? Let's take

some examples. Apple has been doing very well with it's Chinese-manufactured iPod,

raking in $16 billion in sales and $1.6 billion in profit. Their 10% net isn't that impressive,

but look at the sales and profit growth numbers: sales increased 66%, but net profit grew

318%. The stock returns are even more spectacular--up 812% in the past three years.

Just how profitable are U.S. companies having their products made in China? Let's take

some examples. Apple has been doing very well with it's Chinese-manufactured iPod,

raking in $16 billion in sales and $1.6 billion in profit. Their 10% net isn't that impressive,

but look at the sales and profit growth numbers: sales increased 66%, but net profit grew

318%. The stock returns are even more spectacular--up 812% in the past three years.

Apple looks rather tame compared to Motorola, another global supplier of technology with huge operations in China, which pulled in $4.6 billion on sales of $36 billion, a net margin of almost 13%. Intel, which also manufactures products in a number of countries, including China, made a staggering $8.7 billion from $39 billion in sales, a very healthy 22% net profit. (Microsoft, which manufactures nothing material, made $13 billion from $41 billion in sales.) So who's making all the profits in this trade? The U.S. companies. This was carefully documented in an August 2005 article in Foreign Affairs entitled A Trade War with China?. The author demolishes all the hearsay arguments about how trade with China is detrimental to the U.S. economy, revealing that much of China's manufacturing is owned and managed by foreign corporations. In effect, the companies aren't Chinese at all; only the workers are Chinese.

These days manufacturers in China seem unable to pass on the higher costs. Wage inflation is "eating into margins. There is very little pricing power in China -- or globally, anywhere -- anymore," says Michael Barbalas, general manager at the Suzhou factory of Andrew Corp., a Westchester,Illinois maker of wireless networking gear. "You can't negotiate with Wal-Mart , and if you're selling to the large electronics firms, you don't have a lot of pricing power, either." For people bemoaning the loss of manufacturing jobs in the U.S., here's a suggestion: get real. Companies go where they have to in order to survive and prosper in a world where foreign corporations will gladly take sales away from them. If they don't compete on quality and price, they wither. For a better understanding of the realities of the global marketplace, read this Foreign Affairs article, Offshoring: The Next Industrial Revolution?  Many U.S. companies still have huge American manufacturing workforces--Catepillar and Boeing

come to mind, both global leaders which generate big profits--but they also manufacture

components in other nations as well, for a number of compelling reasons which may have little or

nothing to do with low-cost labor. Boeing, for instance,

essentially guarantees sales in Japan by subcontracting out the wing assemblies to high-tech

Japanese manufacturers. No parts made in Japan, no sales in Japan, and so fewer planes made

in Seattle. Pink slips fly, both in Japan and America--not good for anyone.

Many U.S. companies still have huge American manufacturing workforces--Catepillar and Boeing

come to mind, both global leaders which generate big profits--but they also manufacture

components in other nations as well, for a number of compelling reasons which may have little or

nothing to do with low-cost labor. Boeing, for instance,

essentially guarantees sales in Japan by subcontracting out the wing assemblies to high-tech

Japanese manufacturers. No parts made in Japan, no sales in Japan, and so fewer planes made

in Seattle. Pink slips fly, both in Japan and America--not good for anyone.

If you compare the rates of "hard core" long-term unemployment in the industrialized nations (see chart), then you'll see that the U.S. workforce has a far smaller problem than the European nations, which are staggering beneath a long-term unemployment rate of 40% - 50%.

The U.S., on the other hand, exported $819 billion and imported an astonishing $1,526 billion in 2004--and the imbalance only grew larger in 2005. For more statistics, visit the U.S. government site of the Bureau of Economic Analysis So exactly what are the Chinese gaining from this supposedly favorable trade? How about massive environmental damage and the resulting health costs, a potentially devastating asset bubble, a trillion dollars in risky dollar-denominated bonds, and a bunch of foreign-owned factories which will move to the lower-cost competition once wages rise in China. Meanwhile, what has the U.S. gained? Enormous, unprecedented corporate profits, offshored environmental waste, cheap goods, and the off-loading of huge debt. So who's making out like a bandit? The U.S., not China. At least one keen observer, Stephen Roach of Morgan Stanley, sees the Chinese government as moving away from this entire model of growth at any price. I found this link to Roach's recent report from China on the always thought-provoking and well-researched Mish's Global Economic Trend Analysis blog: The Coming Rebalancing of the Chinese Economy. His commentary suggests that the Chinese are already beating a path away from their unhealthy dependency on the U.S. consumer by growing their own consumer spending. If trade with China becomes less imbalanced, perhaps the benefits of the trade will also become more balanced. It's about time. March 29, 2006 The Five Stages of a Housing Bubble  Psychologist Elizabeth Kubler-Ross suggested the process of grieving has five distinct

stages. In a somewhat analogous

fashion, participants in the housing bubble will pass through five emotional

stages: euphoria, doubt, denial, disillusion, realism.

Psychologist Elizabeth Kubler-Ross suggested the process of grieving has five distinct

stages. In a somewhat analogous

fashion, participants in the housing bubble will pass through five emotional

stages: euphoria, doubt, denial, disillusion, realism.

Kubler-Ross's five stages were: denial, anger, bargaining, depression, and acceptance. As people grieve the losses of their paper profits, or more tragically, the loss of their homes or entire equity, they may well pass through these very human feelings along the way. My list is somewhat different, as it starts with the essential emotional building-block of any bubble: euphoria. This is the sense of empowering glee as prices rise, seemingly inexorably, as the participants re-calculate their ever-rising wealth--and all without any application of labor! (Or recently, any deployment of capital, either.) This stage can be seen in the chart of KB Homes, a company which is a good proxy for the large residential builders. The euphoria is visible in the sharp rise of the stock price from mid-2004 to mid-2005. The decline (which I marked for emphasis) from this peak is the doubt/denial stages. As doubt about the housing bubble grows, the stock price falls. Then, as denial kicks in, the price recovers--but importantly, never to the previous high. This "lower highs, lower lows" is the classic stock market definition of a downtrend. A similar battle between doubt and denial plays out in the media every month when housing prices, inventory and sales figures are released. Every lower number spurs doubt, and every stabilizing number elicits denial: everything is OK, prices are stabilizing, etc. At some tipping point, denial gives way to full-blown disillusion. As declines in prices and sales and fast-rising inventories become inescapable trends, the flimsy walls of denial participants have constructed give way, and they become disillusioned with their real estate investments. Some decide to hang on, others decide to bail, and still more stop looking at the very real estate section they used to open first, when their net worth was rising by the month. As the declines continue unabated, year after year, participants finally make a realistic appraisal of the situation: housing was a bubble, and the deflation seemingly lasts forever. Investors give up and sell in disgust, banks give up the ghost and go bankrupt or sell their portfolios of non-performing mortgages for pennies on the dollar, and the ranks of working realtors thins to those few with connections to lenders, who are still dumping their foreclosed properties. When nobody in their right mind would consider buying real estate as an investment, the bottom will finally be reached. Unfortunately, all this takes a long time. That we are just in the very first stages of the decline are apparent in articles such as this one from The Wall Street Journal: Back To Reality, about the quickening slide in vacation home values. So who is still buying houses? It's hard to quantify, but here are my guesses: What appears to be lost on these folks--many of whom own six, ten or even more houses scattered around the country--is that they're simply exporting the bubble to areas which didn't have bubbles for a very good reason: permanent residents lack the big-bucks incomes needed to overpay for houses. While a house valued at $169,000 seems cheap to a Left or Right-Coast investor, when that house drops back to $80,000 in a few years, the loss suffered will be, percentage-wise, as unpalatable as losses suffered in "hot" areas. For examples of locales which are clearly toppy, skim this chart:

March 28, 2006 Housing: Who Wants to Catch the Falling Knife?  The stock market is home to many trenchant phrases--the trend is your friend, sell in May,

go away, among many--but one is particularly relevant now to the housing market: Catching

the Falling Knife.

The stock market is home to many trenchant phrases--the trend is your friend, sell in May,

go away, among many--but one is particularly relevant now to the housing market: Catching

the Falling Knife.

The phrase perfectly captures the dangers of buying into a declining market. To do so is like trying to catch a falling knife: the momentum is all down, and we all know what happens to those who grasp a razor-sharp blade in mid-air. In the stock market, the expression is a warning: it isn't safe to buy until the knife has fallen to earth, i.e. the market has finally hit bottom. Now that the housing market has rolled over and is in decline, the same is true for this bubblicious market. At the risk of preaching to the choir, let's review the evidence that housing has finally slipped off the precipice and is starting its long freefall:

For an understanding of how the Federal Reserve can tighten lending in a "stealth mode" unknown to the average American (including me, until I read this), please read The Fed Officially Kicks Off the Next Recession. This is fascinating reading--a real insider's view of how the Fed can undetectably constrict lending. Lenders are getting squeezed in other more visible ways as well, as The Wall Street Journal reported on March 27: Housing Banks May Be Forced To Cut Dividends: "A crackdown by regulators of the Federal Home Loan Banks threatens to shrink a subsidy long enjoyed by thousands of lenders, including giants such as Washington Mutual Inc. and Citigroup Inc."

and thus mortgage rates--are on the rise. The corporate cheerleaders over at BusinessWeek are actually applauding the rise of the long bond, bond yields are rising--and it's about time, for they know all too well that interest rates in the U.S. are now completely dependent on foreign buyers of U.S. Treasuries. If nobody buys the Treasury's massive auctions of U.S. debt, then interest rates have to go up to entice wary buyers to buy Treasuries rather than Eurobonds. As bond yields rise throughout the world, U.S. rates have to rise, too, lest everyone abandon the dollar and the U.S. bond market. As this chart reveals, the problem is that bond-yield cycles last about 20 years. Just as interest rates and bond yields dropped for 22 years, historical evidence suggests they will rise for the next 20 years. Since housing become increasingly unaffordable as interest rates rise, exactly when will the knife hit the hard dirt of a real bottom? If you consider the last housing top occurred in 1990, and late 2005 appears to be the top of this cycle, you'd have to guess between five and ten years in the future--or maybe even 20 years hence. So who's still willing to try their luck at catching the falling knife in housing? More on that tomorrow. March 27, 2006 Jank Coffee, Upscale Tropic Style  At reader Craig S.'s suggestion--one he may well regret after seeing this, but I hope not--

here is my design for an upscale tropic-flavored Jank Coffee shop.

At reader Craig S.'s suggestion--one he may well regret after seeing this, but I hope not--

here is my design for an upscale tropic-flavored Jank Coffee shop.

To start, I conjured up an island-style coffee bar facing the entry, inviting passersby with serious caffeine on their minds to drop in and take a seat in this bright, airy space. (Yes, that's lava rock supporting the curved bar.) I also selected a fun font for the discreet signage. The other half of the space is devoted to an eclectic, purposefully informal dining area with upscale rattan chairs and a hammock to establish a carefree vacation atmosphere. Add a few plants and some cheap fun lighting, and voila, Have a Vacation Today--at Jank Coffee. To work its magic, this design needs to face a light-filled courtyard or atrium; by sheer coincidence, upscale malls all seem to feature just such courtyards or atriums. So which would you rather step into--one of those cookie-cutter Mermaid coffee shops, or this bright tropic retreat? Remember: Jank Coffee: cause you're worth it. Special bulletin: Read my story Lofty Ambition about the renovation of an old Ford factory in Richmond, Calif, in the San Francisco Chronicle. March 25, 2006 Intriguing Reader Feedback  This blog had the good fortune of being linked this past week to several very popular

websites:

This blog had the good fortune of being linked this past week to several very popular

websites:

As a result, this humble outpost on the great World Wide Web received over 3,000 unique visitors in one day--about the monthly average for this site. With so many curious, intelligent readers coming through the door, so to speak, it's to be expected that I received some interesting feedback. First up is I.M. Vronsky, the editor of the gold-eagle.com website, who addresses the question, "What has been the best investment in the past 5 years: Real Estate or Gold Equities?" in a piece entitled The Real El Dorado: Real Estate or Gold Equities? Calling this "The Cardinal Question of the new Millennium," Vronsky lays out the case that gold and silver actually outperformed real estate over the last five years, and are poised for continued outperformance for a number of reasons. Here is an excerpt: That amounts to $4 Trillion, which is 36 TIMES GREATER than the total combined market cap of all publicly owned gold and silver stocks in the world AT CURRENT PRICES ( i.e. $110,000,000,000 is the market cap of all the world's gold stocks/equities - Source: Sept. 25, 2005, Denver Gold Conference). CLEARLY, spec investments in Real Estate represent a hugh reservoir of money that can flow toward high performance precious metals. It then logically follows if any fraction of spec RE monies divest their properties with the objective of taking advantage of the formidable recent returns in Gold and Silver Equities, precious metal values will soar to unimaginable levels.So if you're an investor (and who isn't, in one way or another), please check out this important essay. Next, reader Richard C. posited another explanation for the "conundrum" which I discussed in the March 20 entry, e.g. who's snapping up Treasury bonds despite the risks and low returns: Your Arab money explanation is highly plausible, but here's another possible scenario for you to consider: the "secret" buyer of US Treasuries is the Federal Reserve itself (possibly in collusion with the Arabs), acting on a political agenda to stabilize the market in US Treasuries to prevent the system from falling apart when foreign governments of record balk at buying. The Fed, of course, can create the money out of thin air.For an explanation of the Plunge Protection Team from our esteemed colleagues across the pond (The Evening Standard in London), read this: Plunge protection and rallying shares. Reader R.C.D. sent along a link to THE FED OFFICIALLY KICKS OFF THE NEXT RECESSION, which I highly recommend for its clearly "insider" account of how the Federal Reserve can tighten lending under the radar of both the public and the media. The article suggests the Fed has signaled just such a cycle of tightening, hence the title of the piece. Especially disturbing is how the Fed is dispensing with the time-honored M3 measurement of money supply; one naturally wonders if it's to hide what they're doing with the tens of billions of dollars they're creating out of thin air. According to this source: Over the past 8 weeks, M-3 is up 129.6 billion, an 8.2 percent rate of growth, and is up a whopping $249.7 billion over the past 12 weeks, a 10.7 percent annualized rate of growth, a $1.0 trillion annual expansion.Yikes! $250 billion is serious money. I wonder if this will replenish the stash of the Plunge Protection Team, which may well already be at work pumping up the suspiciously resilient stock and bond markets.... On a lighter note, reader Craig S. had an inspired suggestion regarding the design of the Jank Coffee Shop: Please allow me to offer constructive feedback on your Jank Coffee concept. It is good, but the English are known for their love of tea, not coffee. How about an upscale Brazilian Planter decor?Your wish is my command, Dear Reader, and though it's a tough challenge, I'm toiling away on a design which will reflect this brilliant concept. Thank you, Craig S., and everyone else who is willing to suspend belief for a moment and put up with the occasional absurdities which crop up (perhaps too regularly) on this site. As always, it is my honor to host you, readers, and a special honor to receive comments from such thoughtful, knowledgeable folks. March 24, 2006 Friday Quiz: Wage Inflation in China  Q. Wages in China are rising; what is the annual percentage increase?

Q. Wages in China are rising; what is the annual percentage increase?

A. Wages are rising by approximately 10% annually throughout China. Regionally, wages rose by 12% in the Nanjing area, 10% in Suzhou and 9% in Beijing. Wages have risen as much as 40% per year as factories try to lower turnover and retain qualified workers. Q. How much did the price of imports from China rise last year? A. The price of imports from China actually dropped .4% last year. Q. How long can wages rise by 10% annually before prices of Chinese goods reflect those higher costs? A. Unknown, but companies with rising expenses must eventually either raise the price of their goods or go out of business. Source: BusinessWeek, March 27 edition March 23, 2006 Wall Street Fiddles While Rome Smolders  A fire is already smoldering in the gasoline warehouse, but Wall Street is fiddling

away, fanning the embers. Rome won't burn, it will explode. What's the gasoline?

Derivatives--trillions of dollars' worth. What's the smoldering fire? Wall Street's

insatiable appetite for ever riskier "investment vehicles" and "hedges."

A fire is already smoldering in the gasoline warehouse, but Wall Street is fiddling

away, fanning the embers. Rome won't burn, it will explode. What's the gasoline?

Derivatives--trillions of dollars' worth. What's the smoldering fire? Wall Street's

insatiable appetite for ever riskier "investment vehicles" and "hedges."

But don't take my word for it. Check out the March 22 edition of the business-centric Wall Street Journal for this story: Debt Party: Investors Scoff at Risk, But Their Borrowing May Haunt Them This isn't exactly a new story--note that the second chart dates from last Fall--but that doesn't mean the risks aren't real. If anything, they're increasing in a heretofore unimaginable manner. Like a rubber band being stretched tauter and tauter, the risks can only increase so much; at some point, the band (and market) will snap. Longtime readers know that I have suggested reading mathematician Benoit Mandelbrot's exploration of market risk, The Misbehavior of Markets  In a nutshell: Mandelbrot proves that standard "portfolio management" models and tools

radically underestimate the risks inherent in any chaotic system, i.e. the market. He

graphically illustrates with historical charts that the stock market does not perform as statistical

models would suggest; rather, it is prone to sudden highly volatile drops and upward

spikes, much as the fractal geometries he developed would predict. He then shows you a real stock

chart and one based on fractals; you won't be able to tell them apart.

In a nutshell: Mandelbrot proves that standard "portfolio management" models and tools

radically underestimate the risks inherent in any chaotic system, i.e. the market. He

graphically illustrates with historical charts that the stock market does not perform as statistical

models would suggest; rather, it is prone to sudden highly volatile drops and upward

spikes, much as the fractal geometries he developed would predict. He then shows you a real stock

chart and one based on fractals; you won't be able to tell them apart.

In other words, the full amount of risk in the market cannot be accurately predicted. We can, however, look at these charts and see that risks are completely underestimated, and that the amount of money being leveraged in derivatives is truly frightening. But let's hear what the Wall Street Journal has to say about risk and complacency: Debt investors expect prices in the market to be stable and returns to be meager for as far as the eye can see. So they are coming to a natural conclusion: It is time to borrow more money and make riskier bets. That type of thinking is often dangerous.Long-Term Capital Management, you'll recall, was the outfit which believed they'd discovered the secret to managing risk--the Black-Scholes formula for pegging the value (price) of options (a form of risk management which even regular investors can buy--the familiar puts and calls). Lo and behold, the market stubbornly refused to follow their predicted models, and LTCM's over-exposure to derivative losses collapsed the firm and very nearly the global banking system. Only the sudden mobilization of the storied "Plunge Protection Team" saved the day. Interestingly, the market has floated along without any prolonged or severe spikes of risk since that blow-up in 1998--almost eight years of ever lower measurements of volatility. (Take a look at the VIX, a measure of option volatility, if you need more proof.) Gazing at these charts, one wonders if the market isn't due for one of the sudden, seemingly random appearances of risk predicted by fractal geometries. Perhaps it's a good time to recall the old dictim: Cash is King. March 22, 2006 The New Jank Coffee Shop  As part of my lucrative design contract with the new franchise, Jank Coffee, I was tasked

with designing a shop front which would appeal to upscale customers willing to drop $3 for

a cup o' Jank. Here is my first rendition of a "killer coffee shop" exterior.

As part of my lucrative design contract with the new franchise, Jank Coffee, I was tasked

with designing a shop front which would appeal to upscale customers willing to drop $3 for

a cup o' Jank. Here is my first rendition of a "killer coffee shop" exterior.

My first thought was to milk Americans' absurd worship of all things English. (As if we didn't have enough dysfunction, scandal and intrigue in our own nobility. OK, we aren't supposed to even have a nobility, so we create one out of largely talentless media stars and politicians; but hey, they cavort, lie, cheat and dissemble with the best, I reckon). So I start with a tweedy little Empire-style facade, complete with fake British lions and faux-Roman columns, both of which add a certain gravitas to what is clearly the smallest and cheapest stroefront on the street. Next, I add a cute little hanging sign, so pedestrians will spot Jank and be drawn in. No detail is too small for your discerning designer; even the font was carefully selected: all capital letters in a classic-looking serif font. Then I pop in a charming little entry/vestibule, so passersby can duck in and look at the specialty coffees on display in the glass cabinet, and be attracted to the rich scent of freshly ground coffee wafting out whenever the heavy wooden door (another nice touch, if I do say so myself) opens. The competition--a long-tressed, voluptuous and apparently quite nude maiden mermaid wearing a crown--is certainly alluring. It's an uphill battle for Jank, but hopefully this exterior which appeals to the Anglophile snob in so many gauche Americans will prove even more alluring than a naked mermaid. Is all this about a mermaid confusing? Perhaps you've never closely examined the green Starbucks logo to deconstruct its true charms. March 21, 2006 Happiness For Sale

The Wall Street Journal recently reported on the trend for marketing companies to cash in on academic research into what makes us happy. Unsurprisingly, Happiness is for sale--for a price. According to Happiness Inc.: Science is exploring the roots of joy – and companies are putting the findings to work (subscription required, but check the local library for the March 18 edition), researchers can help your salespeople overcome the sales-blues caused by customers walking away, or sharpen your marketing to take advantage of the happy fact that insecure people tend to boost their self-esteem and self-fulfillment by--hold onto your hat--impulse shopping. Dang, who'd a thunk it? The Happiness researchers also found that the anticipation of the activity (or purchase) created more joy than the actual activity (or purchase).  Building on the success of my work for Kroika Cookie and Biscuit Company, Ltd., (Xiangxi,

China), I've been contracted to design the initial ad campaign for Jank Coffee. More

about the shadowy owners of Jank Coffee later, but first, feast your eyes on the ad I've

designed to exploit all that fancy research into Happiness.

(To see the full animation, please re-load this webpage.)

Building on the success of my work for Kroika Cookie and Biscuit Company, Ltd., (Xiangxi,

China), I've been contracted to design the initial ad campaign for Jank Coffee. More

about the shadowy owners of Jank Coffee later, but first, feast your eyes on the ad I've

designed to exploit all that fancy research into Happiness.

(To see the full animation, please re-load this webpage.)

While I don't want to delve too deeply into the secret ingredients and subtexts of the ad, I will point out a few obvious features: In other words, here you are, a cog in some bureaucratic machine, underappreciated and underpaid, slogging through hideous traffic and all the other annoyances of life, thinking, "What's in it for me?" when suddenly that cute little Jank Coffee shop beckons. "Cause you're worth it!" the ad says, and you think, subconsciously or consciously, "dang right I'm worth it!" Hey, it's not grammatical, but that didn't hurt Apple's "think different," did it? Heck no, it showed they could care less about those stupid details! Right on, Jank! Stick it to the grammar Man! So you wander in and order a cup o' Jank your way, with soy milk foam and chocolate sprinkles, and you feel better about yourself, and thus fortified to sally forth and do battle with a cold, uncaring world. That was probably the best $3 you ever spent, because look at the big payoff you got for a measly three smackeroos. Cause you're worth it, and Jank is happy you are. March 20, 2006 Who's Buying All the Treasury Bonds? And Why?

Here's an honest-to-goodness mystery for you: Who's snapping up all the hundreds of billions of U.S. Treasury bonds which get auctioned off every quarter, And why are they plunking down such vast sums of real money for such lousy returns? The chart on the right further deepens the mystery. It seems that every time government buying (the blue line--mostly from China and Japan) dries up, threatening to create a crisis in the bond market, then lo and behold, mysterious "private buyers" (the red line), mostly based, it seems, in secretive off-shore banking centers like the Cayman Islands, step up and suck up billions of dollars of the U.S. bonds being auctioned off. Before we get too deep in the mystery, let's cover a few basics of the Treasury market: So if nobody steps up to buy the Treasuries being autioned off, then interest rates will rise--quickly. And what happens to the debt-crazed American economy if mortgage rates (and other loan rates) rise quickly? Recession, because the entire U.S. economy has been supported by rising consumer debt and cash pulled out of housing via mortgage re-finances. OK, let's get back to the magic appearance of huge "private money" every time our trading partner nations start to get queasy about loading up on yet more U.S. debt. (Recall that Japan already holds over $1 trillion in U.S. Treasuries, and the Chinese government has nearly $700 billion.) Let's start by asking, who has hundreds of billions of dollars accumulating every year? China? Nope. Japan? Nope. Europe? Nope. Russia? Nope. The Mideast Oil Exporters? Bingo! A couple of questions come immediately to mind. First: why would the Arab nations want to hide their purchases of U.S. bonds by slipping the money through off-shore banks? And second, why would they be timing their purchases to support the U.S. bond market, insuring low interest rates continue for the debt-mad American consumer? It doesn't take much moxie to suspect the Mideast bankers are hiding the purchases to avoid angering the "Arab Street," i.e. the uneasy mass of citizenry who blames the U.S. for all the region's ills. No leader wants to be asked, "Why is our national treasure being handed to the Americans to support their corrupt lifestyle?" Better, by far, to ease the cascading billions into off-shore private banks and make the purchases from there, real secret-like. Some people speculate that this massive buying originates from hedge funds, and no doubt some of it does. But hedge funds are notoriously fickle investors--buy today, sell tomorrow. Yet the Treasury market has remained remarkably stable. If anyone were dumping a hundred billion dollars' of U.S. bonds, the market would quickly reflect that dumping. Since nobody's selling, it can't be all hedge funds. Furthermore, the amounts of money being dumped into Treasuries exceeds even the grasp of the largest hedge funds. So then we have to ask: why are the Mideast oil barons buying American bonds? One could claim that it's for safety. Perhaps--but why time the purchases so perfectly to support the U.S. economy? The better answer is: If the U.S. economy goes into a tailspin, the price of oil will plummet along with it. As cash-starved consumers tighten their belts, demand for gasoline and jet fuel drops--triggering lower oil prices. That's true, and a very powerful argument. But I also wonder--and I have yet to read this supposition anywhere else in the media--if it isn't a Sunni quid pro quo: we'll fund your war in Iraq indirectly by buying up all your Treasuries, as long as you protect the Sunni minority in Iraq from the Shiite majority. Farfetched? Not at all. Suppose the wealth of the U.S. was held by a small coterie of pragmatic Pentacostal Christians of the sort whose beliefs inform their worldview and their actions. Wouldn't they funnel money to a government which was protecting a Christian minority from a potentially devastating civil war? I think there is no question that such a spiritually-based leadership would have absolutely no qualms about doing exactly that. Would the players want such an arrangement to become public? Of course not. It would be handled in a thoroughly "wink wink, nudge nudge" manner. It makes sense to me, and perhaps this is one reason why the U.S. won't be leaving the Iraqi Sunnis (only 20% of the population) to twist in the winds of civil war. Recall there's no love lost between the Iranian Shiites and the Arab Sunnis, and you have the makings of a carefully cloaked Grand Master Strategy board. Are Treasuries part of the game? Well, why wouldn't they be? there's no bigger pieces right now than oil, Iraq and an increasingly fragile U.S. economy. March 18, 2006 A Monster of a Housing Bubble

Take a look at this chart and tell me there's no housing bubble, and that real estate can keep on rising indefinitely. What the chart reveals is that over-investment in housing (as measured by investment per worker) is inevitably followed by a recession. The two exceptions which prove the rule were the Korean War and the Vietnam War, which goosed the GDP by 15% and 10% respectively, pulling the economy out of the recession which would have otherwise taken the nation by the throat. The cost of that deficit spending on both "guns and butter" in the late 60s and early 70s? A structural inflation which gutted the bond and stock markets for a decade. "This time it's different," we're told, because China's manufacturing costs are so low, inflation has been banished. "This time it's different;" hmm, isn't that what the housing Bulls are saying as well? Isn't that what the tech analysts were saying in January 2000, just before the dot-com bubble burst in March 2000? The glaringly obvious point is that the present level of over-investment is unprecedented, suggesting that the ensuing recession will be deeper and longer than previous over-investment/recession cycles. It's worth noting that the last "real" recession--that is, one that lasted more than a few months--occurred 25 years ago. That's an awfully long run of expansion.

The chart's upward trajectory since 1990 has a eerie, if not downright frightening, resemblance to the parabolic rise of the NASDAQ stock market 1997-2000. As we all know, the NASDAQ subsequently plummeted 80%. Six years after the bubble's peak, the Nasdaq has only recovered 45% of its bubble valuation. That couldn't happen to real estate, the yammering industry Bulls yelp; maybe so, but what about a 40% drop? Check back in 2010 and let's see where valuations are then. March 17, 2006 Friday Quiz: Median Price of an American House Q. What was the median price of an American house in 1996, and in 2005? A. The median price of an American house in 1996 was $140,000. In 2005, it was $234,000. Q. If housing had only risen with inflation (26% total since 1996), what would the median house price have been in 2005? A. The median house price would be only $176,000. Q. Inflation has risen a total of 26% since 1996; by what percentage has housing risen? A. The median house price has risen by 67% since 1996. Sources: inflation data: www.bls.gov median house prices: economagic.com March 16, 2006 Books of Interest: Identity and Multiculturalism My interest in identity and multicultural America recently led me to the following titles. The first is by a Nobel-prize winning economist who has turned his attention to the two versions of multiculturalism he sees--specifically, the false multiculturalism of various groups living side-by-side in a polyglot society but never interacting, a state he calls "plural monoculturalism." The next two are by an African-American academic. Both books explore the nature of multiple identities, and how having multiple or fluid identities is a natural consequence of liberty in a multicultural society. The last one is by a philosopher with a wide range of interests. I cannot yet comment on it at length (I need to buy a copy first) but it looks accessible and promising. Identity and Violence: The Illusion of Destiny by Amartya Sen The Ethics of Identity and Cosmopolitanism: Ethics in a World of Strangers by Kwame Anthony Appiah The Ethics of Authenticity by Charles Taylor March 15, 2006 The Coup de Grace to the Economy  Please examine the two charts in this entry carefully. If you look closely, you'll

see they spell "doom" in rather large, dayglo letters. Why? Because they reveal two

ominous trends: that real estate investment has become an unprecedentedly large percentage

of total GDP (Gross Domestic Product), and that homeowners are no

longer able to extract cash from their property via refinancing.

Please examine the two charts in this entry carefully. If you look closely, you'll

see they spell "doom" in rather large, dayglo letters. Why? Because they reveal two

ominous trends: that real estate investment has become an unprecedentedly large percentage

of total GDP (Gross Domestic Product), and that homeowners are no

longer able to extract cash from their property via refinancing.

Why do these two trends spell doom? The first and most important reason is that

heavy reliance on residential real estate investment always precedes a recession. The more

extreme the dependence on housing, the more extreme the recession (and subsequent drop in

real estate values).

Why do these two trends spell doom? The first and most important reason is that

heavy reliance on residential real estate investment always precedes a recession. The more

extreme the dependence on housing, the more extreme the recession (and subsequent drop in

real estate values).

For the chart which proves this, go to a previous entry entitled Housing Bubble III: Pop! The second reason is that merely halting the rise of real estate values has been enough to utterly quash the removal of spendable cash from Americans' home equity ATM (otherwise known as the family home). As noted in a previous entry this week, Americans drew out $880 billion from their homes via re-fi's and home equity credit lines in 2005 alone. Add up all the home equity extracted since 2000, and you have a number in the trillions. So what happens, now that the home equity ATM has finally run out of money? For one thing, consumer spending falls. And since consumer spending is 2/3 of the U.S. economy, that's all you really need to know. Squeezing 2/3 of the economy is more than enough to induce recession, especially when you add in the millions of households who will be paying more to service their adjustable-rate mortgages when the "resets" kick in later this year. March 14, 2006 As the Real Estate Bubble Pops, so Does the Economy  First, let's demolish the cliches people spout to justify the notion that today's

skyhigh real estate prices are permanent:

First, let's demolish the cliches people spout to justify the notion that today's

skyhigh real estate prices are permanent:

As described in yesterday's entry, this hopeful cliche also ignores what happens when adjustable-rate (alas, always a low "teaser rate" to start) mortgages rise (the harmless sounding "resets"), triggering foreclosures. The lenders can't wait five years for values to recover; they need to get the distressed properties off their books ASAP, regardless of their losses.

"The market feels a lot like it did in March of 2000, right near the top," says Mr. McClintock of Babson. He doesn't expect a pullback nearly as severe as that one, but he has the same sense of excess market optimism at a time when the economy is slowing and bond yields are rising.In a nutshell: foreign buyers of U.S. debt (bonds) have artificially suppressed interest rates. Now, with rates around the world rising, the U.S. must raise interest rates in order to keep our bonds attractive to foreign investors--Asian central banks and Mideast nations flush with record oil profits. The inevitable conclusion: as bond rates rise, so do interest rates. As Interest rates rise, housing prices drop and foreclosures rise, putting more downward pressure on housing values. As housing values drop, American can no longer borrow their equity to spend, spend, spend. According to many sources (for example, Parade Magazine this past Sunday), American pulled out $880 billion from their home equity in 2005 alone. That accounts for about 7.5% of the entire U.S. economy, and about 10% of all consumer spending.  And what happens to the economy when Americans can no longer count on more debt

to support their lavish spendng? Recession.

And what happens to the economy when Americans can no longer count on more debt

to support their lavish spendng? Recession.

If you need some numbers, please read this piece from the Wall Street Journal: The Debt Bubble Threatens to Derail Many Baby Boomers' Retirement Plans Let's start with a shocking revelation: If you borrow money, it eventually has to be repaid. We all know this, of course. Yet the data suggest many Americans are trying their hardest to ignore this inconvenient fact.While this might be easily dismissed if it was from some wildly unfactual blog, this is from the august Wall Street Journal. How long can we as a nation dismiss the facts? For better or for worse, the markets will not dismiss the facts for much longer. The stock market is heading lower, predicting the coming "the real estate bubble has finally popped" recession. As housing weakens both in sales and prices, it feeds what is known as a negative feedback loop: the lower prices drop, the less people can borrow, and the debt machine grinds to a halt. As the cost of borrowing rises, people's spendable cash plummets, leaving them less to blow on consumer goods, further weakening the economy. In sum: the evidence is in, and it's compelling. Look out below. March 13, 2006 The Three Laws of Real Estate

We've all heard the three rules of real estate: "location, location and location."

Cute, but have you heard the Three Laws of Real Estate? They're not quite as droll.

So let's look at what's happening with each of these laws in the real world.

So let's look at what's happening with each of these laws in the real world.

The reason is not hard to fathom. As interest rates rise, people can no longer afford to pay absurd sums for houses. Let's take a buyer who squeezed into a $400,000 home (or condo) with little or no money down and an interest-only adjustable-rate mortgage of the sort which has funded about 40% of the recent home purchases in California. At the starting teaser rate of 5%, the annual payments total $20,000, or $1,666 per month. (Recall that 666 is the number of the Beast...). Their property tax in the high-tax Bay Area will run at least $8,000 per year and more likely $10,000 a year, depending on the municipality. Fine and dandy, but guess what happens to the rates when the first two years are up? They rise by 40% to 80% overnight. Don't believe this? Then check out this Wall Street Journal piece Millions Are Facing Monthly Squeeze On House Payments; Many Adjustable-Rate Loans,Popular in Recent Years, Will Soon Be Reset Higher. According to the WSJ, subprime borrowers (those with less than sterling credit histories) will be paying 8%, 9% and even 10% interest soon, as the loan "catches up" to all the principal which has accumulated unpaid in the "interest only" stage. The monthly payments at 8% would rise to $2,666, plus accelerated principal payments. That's over a $1,000 more per month. Many recent home buyers won't have the equity to justify a re-fi into a lower fixed-rate mortgage, and with no other alternative, they'll walk away. Guess what happens to the foreclosed home? The lender puts it on the market so fast your head will spin. And they'll "price it to move," i.e. whatever it takes to sell it quickly, because all that bad debt on their books raises their reserve requirements drastically. And what does that mean? It means they have to keep huge quantities of cash on hand, which means they can't lend as much money, which means they can't make money, either. Which leads us to Laws Two and Three. As tens of thousands of foreclosed homes hit the market, along with the hundreds of thousands of new homes and condos currently under construction, then supply will dwarf demand. As people see prices plummeting, they'll hold off buying, further weakening demand. As demand falls, lenders will lower the price of their swelling portfolio of "distressed" properties, dropping prices further. Don't think can happen? Read what happened in the dim dark misty past of 15 years ago, when the last real estate boom died a slow agonizing death. Here is where Law Three enters the picture. Real estate is highly illiquid. There are thousands of houses and condos in a city, but only a few hundred change hands in the normal course of events--people move, they die, they get transferred, their families grow or shrink in number, they retire, etc. The salient point is: the value of 10,000 houses rests solely on the price paid for the last house sold. If prices fall, then the value of all houses falls, regardless of the purchase price or what the appraisal says. More on the consequences of these three laws tomorrow. March 11, 2006 Oscar Injustice III: Kieslowski and "Red"  Yet the Trilogy will undoubtedly endure while the Oscar winners of those years will be largely forgotten. Why? Well, let's start with all the Hollywood cliches about screenplays: story arc, plot points, blah blah blah. Open any screenwriting guide and you'll find that the first plot point arrives on page (and therefore minute) 20. Check it out. Twenty minutes into a film, something happens which causes the action to swerve in a new direction. If we follow up the idea that all art works from some "center," some gravitational focal point which draws us in, then the vast majority of Hollywood films work from a a plot-driven center: a character must overcome an obstacle, there's something at stake which has to be resolved by a voyage, and so on. On ocasion, the center of a movie will be the transformation of a character. In a good movie, the two are seamlessly overlaid. Thus, in Casablanca, the "something at stake" is Victor Lazlow's escape to America, and the transformation is Rick's emergence from self-pity to understanding, sacrifice and action. What makes Red so intriguing (other than its visual virtuosity) is the ambiguity at its center. Exactly what is the "plot"? A model accidentally hits a dog and finds the owner, who feigns indifference. The model cares for the dog and establishes a vague sort of relationship with the owner, an irascible retired judge. Not much here in terms of story arc and other Hollywood conventions. But there is a beating heart to the story, perhaps even several. One is certainly "contingency," a philosophic word for chance, serendipity and even synchronicity. Things happen in a causally linked but outwardly haphazard fashion. Another center in this film is intimacy, the difficulties of intimacy and the secrets plumbed or hidden in intimacy. The model's boyfriend seems to be extremely suspicious of her; during every call, he cross-examines her as if unbelieving she is truly alone. We never see him, we only hear his disembodied voice. When she asks him if he loves her, he replies, "I think I do, which is the same thing." She demurs. The retired judge, meanwhile, is secretly listening to the intimate phone conversations of his neighbors. A third center to the movie is how patterns of human behavior and relationships pop up again and again. Thus the judge's own story of a lover's betrayal is played out by a promising young lawyer, and perhaps also by the model's own relationship with the boyfriend. The charm of the film is that these patterns, overlays and elliptical references are not announced, they are hinted, suggested, brushed on in chiaroscuro. The use of color is unavoidably central in the films, as befits a series of movies named after the French tricolor flag, as are the themes of liberte, egalite et fraternite. Yet just as striking is the powerful deployment of music. You would be hard-pressed to name another film which wasn't specifically about music itself (i.e. The Last Waltz, etc.) with a better vocabulary of musical flourishes and colors. This is clearly referenced in the first film, Blue, whose main characters are composers and their lovers. The transformation of character is understated in Red, but it is nonetheless visible. The judge turns himself in for spying, and returns from his punishment a better man. His dog, the one he cared so little for at the beginning, has a litter of puppies. As for the model, her growth is nearly invisible, but we sense it beneath the surface. The film ends with her traveling to see her boyfriend in London, leaving us with the anticipation of some discovery, revelation and perhaps closure or renewal. Maybe the model hasn't changed much so far, but we sense that her experiences have prepared her to deal forthrightly with her boyfriend's infidelity. At least that's my read of a purposefully, and artfully, ambiguous movie about life's inherent ambiguities. March 10, 2006 Friday Quiz: Calories in Chocolate Q. How many calories in a 5-ounce (141 grams) bar of Hershey's chocolate? A. 800 calories, roughly equivalent to a McDonalds double cheese burger and fish burger or 13 apples or 8 bananas. March 9, 2006 Rot at the Center of the Empire I don't follow baseball much, but it's clear that Barry Bonds, Mark McGuire and Sammy Sosa are frauds and liars, and that the institution of baseball is shielding their chicanery in the name of profit. This is yet another example of the rot at the core of American society. The hollowness of a record being broken by a drug-enhanced athlete is so blatant that it defies belief that major league baseball has the chutzpah to ignore the drug scandal at its very heart. This is, sadly, the "All American Game" in its truest sense--a game in which deceit and deception a la Enron et. al. are actively encouraged by a culture of unmitigated greed and corruption. From the lobbying scandals rocking Congress to the bizarrely bloated bodies of American athletes to the deceptions and cover-ups of Pat Tillman's tragic death by friendly fire in Afganistan, the rot at the center of American society is painfully obvious. Is this really nothing more than "business as usual"? That is the apologists' line, that the corruption in Congress is standard operating procedure, that friendly fire deaths have always been covered up, and that sports has always had a seamy, sleazy underbelly of gambling fixes and other frauds. While it's easy to make the case that all this is merely business as usual, I see this complacency as evidence of a much deeper and more pervasive rot than the ills of greed, deception and corruption. Even as our tottering financial empire rests precariously on the shifting sands of rapidly mounting debt, this same complacency--it's "business as usual," nothing alarming here, move along folks--reigns supreme. As Social Security and Medicare head toward inevitable insolvancy, complacency reigns supreme. As our enormously wasteful lifestyle rests ever more precariously on dwindling oil served up by despots, complacency reigns supreme. These issues have no ideological label--they will affect us all. Yet complacency reigns supreme. Let's be clear about one thing. Barry Bond's bulky body has the same resemblance to his physique 10 years ago as Michael Jackson's face has to his teenage features. Yet we as a people are swallowing the lies at the heart of baseball whole, still ponying up $60 or more to see a parade of drugged-out millionaires chase a "record." As long as we're gullible enough to enrich the fraudsters and liars by watching their silly antics, and paying big money to do so, the liars and cheats have every incentive to keep up the charade. Want to do something useful this summer? Don't watch baseball and don't attend any games. What an easy and painless boycott it will be. March 8, 2006 Oscar Injustice II: Thailand's "Iron Ladies"  Unlike the more serious, if not downright dour Brokeback Mountain, Iron Ladies is a spirited, very Asian telling of a wonderful story: how a group of transvestite gay males came together to form a champion volleyball team in 1996. This isn't just "based on a true story," it is a true story; the actors' even bear an uncanny resemblance to the actual guys and gals (their coach was a gay female) who lived the reality (they're shown in some clips at the end of the film). Unlike most Western films about gays, this film isn't afraid to have fun, from the ribald gutter language to the over-the-top antics of some of the players. For added frisson, the team captain is a hetero guy who has to come to grips with his own ignorance and intolerance. The Asian influence is very visible; at several points, a cheesy pop song breaks out for no particular reason, and the action sequences of the guys playing volleyball do not have the realism expected of a Hollywood sports film. Still, all the sports movie cliches are intact, right down to the cliff-hanger final grudge match for the national championship. (Volleyball, it seems, is the Thai equivalent of basketball in the States, while the ultra-violent Thai kickboxing more or less assumes the role of the NFL--if football included boxing and no-holds-barred kung fu.) Yet despite the cliches, the film perceptively imparts the swirling interplay of tolerance and intolerance within Thai society for openly gay people. Despite the cliches, we are openly rooting for the team to win, and we hope for each individual's happiness. Especially touching is the husband and wife who openly accept their son as he is, and enthusiastically celebrate his team's success. As a footnote, it must be said that the one actor who plays a dancer is more beautiful than most women. Having seen similar guys in Thailand myself, I can only say the outward transformation of a Thai male into a female is most remarkable and most convincing. March 7, 2006 Oscar Injustice: Howl's Moving Castle  Part of the charm of this film stems from the way the quasi-Victorian clothing and setting is inhabited by the dark Japanese anime themes of malevolent witches and a tortured, impetuous young wizard. Though ostensibly a children's film, the themes are certainly mature. The heroine is cursed by an evil witch not for any wrong-doing or even nobility on her part, but simply by being in the wrong place at the wrong time. The young male wizard's moral character is ambiguous; while he speaks kindly to the poor cursed girl, and offers her some aid, he also returns from wizardry outings bloodied and beaten. There is a secret war within him and in the world beyond, and some thread connects the two. The witch's animosity for the young wizrd is unexplained and must be intuited; nothing is as it seems at first glance, and we, like the innocent heroine, must figure out a complex world of strange powers and shifting alliances. Too bad this wonderful and thought-provoking film didn't win the Oscar. March 6, 2006 Healthcare Will be Unaffordable Everywhere  The OECD just issued a report concluding that the U.S. is not alone in its healthcare

woes. Seeing as how I just reported on Kaiser Permanente as a potential model for

a cost-effective national healthcare, it's eye-opening that virtually every nation,

developed and developing alike, will face unaffordable government spending as the

population ages and medical technologies increase in sophistication and cost.

(Note that the graph to the right only charts government expenditures, and does not

include private sector spending.)

The OECD just issued a report concluding that the U.S. is not alone in its healthcare

woes. Seeing as how I just reported on Kaiser Permanente as a potential model for

a cost-effective national healthcare, it's eye-opening that virtually every nation,

developed and developing alike, will face unaffordable government spending as the

population ages and medical technologies increase in sophistication and cost.

(Note that the graph to the right only charts government expenditures, and does not

include private sector spending.)

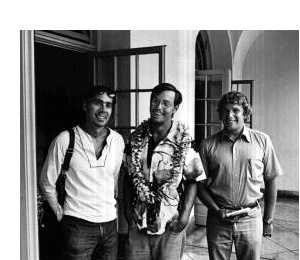

To quote from the Wall Street Journal's story on the report, U.S. Needs a New Prescription To Slow Health-Care Spending: Economists at the Organization for Economic Cooperation and Development, a think tank in Paris bankrolled by 30 developed countries from Australia to the U.S., are waving a red flag.What's truly frightening about this report for Americans is that government spending is less than half of our total healthcare costs: In most OECD countries, including Canada and Britain, health-care systems are financed primarily through taxes. In the U.S., by contrast, about 55% of the health-care bill is paid by individuals and their employers. Yet U.S. government spending on health care -- mainly Medicare and Medicaid -- amounts to an above-average 7.2% of GDP. (Overall U.S. health-care spending, private and public, this year is projected to equal 16.2% of GDP.)This is a staggering sum, yet we have not even begun to pay the full cost of caring for the 76 million Baby Boomers. The 800-pound gorilla in the room which no one wants to recognize, of course, is that virtually the only way any society can manage to offer equitable healthcare to its citizenry is to ration it. That is, no heart operations offered to those over 72, no artificial hips to those over 70, and so on--unless you can pay for it yourself or have private insurance. Given the poor health of our citizenry, correcting the ailments caused by smoking, excessive alcohol consumption and poor diet/obesity is increasingly unaffordable. As reported in today's San Francisco Chronicle, We're living longer -- is that a good thing? The benefits of increased lifespans could come at the cost of greater societal burdens, some experts believe that the obesity epidemic is dooming the younger generations to shorter lifespans than those of the Baby Boomers. Sobering stuff, indeed, especially if you grasp the extreme precariousness of the U.S. government's finances today, never mind in 10 or 20 years. On a happier note, I recently assembled a page of all the books and films I've recommended here over the past few years--80 titles--and I invite you to browse the list, which has been helpfully broken out into various topics: books and films. March 4, 2006 Is the Web a Giant Copy Machine? My old friend and AFSC/People's Party of Hawaii mentor/comrade Jeff Blair has created a compelling and novel way to understand the Web: as a global copy machine. Here are excerpts from Jeff's academic paper on the subject, Using Images Posted on the World Wide Web. It is not surprising that many people still think about the use of images on the World Wide Web as if they were images in a book. The Web, however, is not just a super-sized digital library. It is also a copy machine. (emphasis added)In essence, what Jeff is proposing is a new understanding of digital sharing, community and rights. If you post a photo on the Internet, you are de facto granting other users the right to print or otherwise use that image--to make a copy, so to speak, on the global copy machine. This concept has broad-reaching intellectual-property rights and technology implications. Is it fair that someone could copy your photo, modify it (or not) and then sell the copies (on T-Shirts, for instance) for commercial gain? Obviously it is not. Yet demanding that every user obtain legal permission to print your photo on his/her home inkjet printer for their own enjoyment is impractical and as Jeff notes, impossible to enforce. As Jeff wrote in a recent email: My feeling is that giving access is defacto permission to make direct links and make personal copies (without publication or posting on other websites--although, practically speaking, these infractions would be difficult, maybe impossible to enforce).From one point of view, then the solution is straightforward: if you don't want others to use an image, or direct a URL to it on the Web, then don't post it on the Web. Yet this would deprive many people of the enjoyment of viewing images which the vast majority of users have no intention of using for commercial gain. Furthermore, is it "copying" if someone posts a link to your image on their website? If it is a free site, is this OK? But what if it is a commercial site which charges "admission"? While I am only a technological neophyte (though I do know about ./etc and stuff like that), I foresee the solution being technological rather than legal in nature. New commands (i.e. controls) could be written into a future version of HTML by the W3C which would enable or block copying the image from a browser. These controls could then be embedded in the IMG SRC tags of HTML by the creator. If you wanted to block copying of an image, you'd simply add a command to the IMG SRC tag much like you add an ALT command now. It may even be possible to add commands which would enable or disable URL links to images from outside websites. I don't know enough about the inner workings of HTML to speculate beyond these possibilities. It's also possible that a new image compression tool could be coded (like PNG is supposed to replace JPG) such that copies would carry a digital watermark which would destroy the image when printed. There is already digital watermark software, but enabling this feature in the compression protocol itself would simplify the process. I think the "global copy machine" is a fascinating and profound idea, and I recommend you check out the full paper at the link above. Just to show you how far back Jeff and I go, the photo on the right (courtesy of Ian Lind) is from the early 70s, circa Jeff's resistance/arrest/court battle/acquittal against the Selective Service system. Jeff is in the middle, just to the left (physically, if not figuratively) of famed activist Jim Albertini. The photo on the left is from Jeff's visit to Berkeley a year or so ago.

March 3, 2006 Friday Quiz: Biggest Consumers of Chocolate Q. Which countries have the highest per capita consumption of chocolate? A. The per capita consumption of chocolate in both Switzerland and the United Kingdom is 22 pounds ( 10 kilograms) per person. U.S. per capita consumption is 12 pounds, while the French consume 5 kilograms ( 11 pounds) per person. Japan consumes only 1.4 kilograms per capita (about 3 pounds). March 2, 2006 National Healthcare Made Easy Amidst all the hand-wringing and political jockeying over the insane inefficiencies and skyrocketing cost of healthcare in this country, everyone overlooks a model which currently serves millions of Americans at moderate expense and which could easily serve as the blueprint for a simple, affordable National Health Plan. It's called Kaiser Permanente.  The problem is startlingly visible in the chart to the right: Medicare and Medicaid (the

Federal healthcare program for the poor) will soon cost more than the nation can possibly

afford.

The problem is startlingly visible in the chart to the right: Medicare and Medicaid (the

Federal healthcare program for the poor) will soon cost more than the nation can possibly

afford.