|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | ||

Writing/Film Dear Aspiring Writers: The Worst Advice You'll Ever Read A Literary Look at I-State Lines Spirited Away: Decay and Renewal An American Poem (Robinson Jeffers) Taoist Chinese Poems The Nelson Touch "It's all about oil, isn't it?" Kurosawa's High and Low A Bountiful Mutiny Howl's Moving Castle Thailand's Iron Ladies Trois Colours: Red The Thin Man: Thoroughly Modern Movies Why My Book Is Better Than the DaVinci Code Iranian Films: The Mirror Piratical Nonsense A Real Pirate Movie: Captain Blood 2005-06 archives 2007 archives Recommended Books American Identity American Identity Literary Contest Winners, 2006 (fiction and essays) Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Your Tattoo in 50 Years The American House and Frank Lloyd Wright Cultural Commentaries On Hatred and Anti-Americanism Anti-Americanism Part 2 Anti-Americanism Part 3 French-Bashing Germany: We All Have Problems, But... Kroika! Chronicles This Blog Sells Out Doom and Gloom Sells The Kroika Mascot-"Auspicious Pet" Wal-Mart and Kroika Kroika and Starsbuck Take a Hit Kroika Ad 1 Kroika Ad 2 Kroika Ad 3 Kroika Ad 4 Kroika Makes Bid for Oreo (April 1) Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Corruption and Avian Flu: China's Dynamic Duo Exporting the Real Estate Bubble to China Is the Bloom Off the China Rose? China Irony: Steel, Marx & Capital Curing The U.S. and China's Dysfunctional Relationship China and U.S. Inflation Trade with China: Making Out Like a Bandit Whither China? Will the Housing Bust Take Down China? China's Dependence on Exports to U.S.; Is China About to Pop? 2005-06 archives 2007 archives Battle for the Soul of America Katrina, Vietnam, Iraq: National Purpose, National Sacrifice Is This a Nation at War? A Nation in Denial Why Is This Such a Tepid Time? That Price Isn't Cheap, It's Subsidized The Most Hated Company in America U.S. Fascists Seek Ban on Cancer Vaccine The Truth About Christmas American Dream or American Nightmare? 2006 Sea Change Obesity and Debt Immigration Ironies U.S. Healthcare: Working Toward a Real Solution A Drug Industry Running Amok Where There Is Ruin 2005-06 archives 2007 archives Financial Meltdown Watch What This Country Needs Is a... Good Recession Are We Entering the Next Age of Turmoil? Why Inflation Appears Low Doubling Down on 5-Card No-See-Um A Rickety Global House of Cards Are Japan and Germany Truly on the Mend? Unprecedented Risk 2 Could One Rogue Trader Bring Down the Market? Worried about Inflation? Stop Measuring It Economy Great? Bah, Humbug Huge Deficits and Huge Profits: Coincidence? Who's The Largest Exporter? Three Snapshots of the U.S. Economy Loaded for Bear Comparing Nasdaq to Depression-Era Dow Who's Buying Treasury Bonds? And Why? Derivatives: Wall Street Fiddles, Rome Smolders Financial Chickens Coming Home to Roost Is the Stock Market on the Same Planet as the Economy? The Housing-Recession-Oil-Healthcare Connection Could We Have Deflation and Inflation At the Same Time? What We Know, What We Can Safely Predict Bankruptcy U.S.A.: Medicare, Greed and Collapse Sucker's Rally A Whiff of Apocalypse Where There Is Ruin II: Social Security 2005-06 archives 2007 archives Planetary Meltdown Watch The Immensity of Global Warming Sun Sets on Skeptics of Global Warming Housing Bubble Watch Charting Unaffordability A Monster of a Housing Bubble A Coup de Grace to the Economy Hidden Costs of the Housing Bubble Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Housing Market Slips Toward Cliff Housing Market Demographics Housing: Catching the Falling Knife Five Stages of the Housing Bubble Derailing the Property Tax Gravy Train Bubbling Property Taxes Have You Checked Your Property Taxes Recently? Housing Bubble: Where's the Bottom? Housing Bubble: Bottom II The Housing - Inflation Connection The Coming Foreclosure Nightmare 1 How Many Foreclosures Will Hit the Market? Housing Wealth Effect Shifts Into Reverse Housing Bubble Bust Will Take Down the Global Economy The New Road to Serfdom: A Negative-Equity Mortgage The Housing-Savings-Recession Connection After the Bubble: How Low Will It Go? After the Bubble: Rents and Housing Values Why Post-Bubble Rents Matter After the Bubble: How Low Will We Go, Part II Housing: 10% Decline May Trigger Financial Ruin How to Buy a $450K Home for $750K Inflation and Housing: Calculating the Bust The Growing Financial Risks of the Housing Bubble Construction Defects: The Flood to Come? Construction Defects Part II Who Gets Hammered in the 2007 Housing Bust Real Estate Bust: The Exhaustion of Debt What Happens When Housing Employment Plummets? One More Hole in the Housing Bubble: Insurance Financial Kryptonite in a "Super-Strength" Housing Market Three Secrets to Unloading Property Today Welcome to Fantasyland: Housing's "Soft Landing" Why Is the Median House Price Still Rising? Why Median Prices Appear to be Rising? The Root Cause of the Housing Bubble Housing Dominoes Fall Twilight for Exurbia? Phase Transitions, Symmetry and Post-Bubble Declines Housing's Stairstep Descent 2005-06 archives 2007 archives Oil/Energy Crises Whither Oil? How much Is a Gallon of Gas Worth? The End of Cheap Oil Natural Gas, Naturally High Arab Oil Money and U.S. Treasuries: Quid Pro Quo? The C.I.A., Oil and the Wisdom of Crowds The Flutter of a Butterfly's Wings? A One-Two Punch to a Glass Jaw Running Out Of Oil vs. Running Out of Cheap Oil 2005-06 archives 2007 archives Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds Geezer Rock Overload Paying for Web Content Light-As-Air Pancake Recipe In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono Happiness for Sale: Jank Coffee Ten Guaranteed Predictions for 2010 Why My Book Is Better Than the DaVinci Code My Brand Management Stinks Design Follies The New Jank Coffee Shop Jank Coffee, Upscale Tropic Style One-Word Titles Complacency Nostalgia Lifespans Praxis Keys to Affordable Housing U.S. Conservation & China Steve Toma, Me & Skil 77s: 30 years of Labor Real Science in the Bolivian Forest Deforestation and Sustainable Forestry The Solar Economy (book) The Problem with Techno-Fixes I Love Technology, I Hate Technology How To Blow off Web Ads and More 2005-06 archives 2007 archives Health, Wealth & Demographics Beauty of the Augmented (Korean) Kind Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Is Obesity an Inflammatory Response? Demographics & National Bankruptcy The Decline of Europe: A Demographic Done Deal? Are the Risks of Obesity Overstated? Healthcare: Unaffordable Everywhere Medication Nation The New Disease We Just Know You've Got Can You Can Tell Which Pill Is Fake? Bankruptcy U.S.A.: Medicare, Greed and Collapse The 10 Secrets to Permanent Weight Loss 2005-06 archives 2007 archives Landscapes Selling the Landscape The Downside of Density Building Heights and Arboral Roots Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Waimea Canyon, Yosemite, Camping & Pancakes Nourishment The French Village Bakery Ideas What Is Happiness? Our Education System: a Factory Metaphor? Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi Splogs, Blogs and "News" "There is no alternative to being yourself" Is There a Cycle to War? Leisure, Time and Valentines Is the Web a Giant Copy Machine? Science Matters Anti-Missile Defense: Boost Phase Vulnerability History The Strolling Bones: Rock of Ages Bad Karma: Election Fraud 1960 Hiroshima: First Use All the Tea in China, All the Ginseng in America Friday Quiz Pet Obesity The Origins of Carbonara Organic Farms Oil and Renewable Energy Human Diseases Wine and Alzheimers Biggest Consumers of Chocolate 2005-06 archives 2007 archives Essential Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So Fewer: How the New Demography of Depopulation Will Shape Our Future The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal The Future of Life Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies The Solar Economy: Renewable Energy for a Sustainable Global Future The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Feeling Good: The New Mood Therapy Revised and Updated Recommended Books More book reviews Archives: weblog January 2007 weblog December 2006 weblog November 2006 weblog October 2006 weblog September 2006 weblog August 2006 weblog July 2006 weblog June 2006 weblog May 2006 weblog April 2006 weblog March 2006 weblog February 2006 weblog January 2006 weblog December 2005 weblog November 2005 weblog October 2005 weblog September 2005 weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

|

February 28, 2007 "I Wonder". . . If the Recession Has Already Started I wonder if the recession that former Chairman Greenspan hinted might start later this year has in fact already started. As you know, the "official" beginning and end of a recession are only established long after the fact; so it is entirely possible that sometime in early 2008 the announcement will be issued: the recession started in January 2007. I was mildly amused by Mr. Greenspan's reference to the "business cycle," as that was precisely what he tried to eliminate with his unprecedented "free loans for everybody with a job!" liquidity explosion in 2001-2003. The U.S. business cycle had a recession in those years, but rampant consumer spending and the housing bubble erased the consumer side of the cycle. Now we have to wring two recession's worth of excesses from the economy--starting with the housing market and then moving to the stock and bond markets. Why do I wonder if the recession has already started? The reasons have long been discounted via the "it's different this time" rationalization. Here are the usual suspects: Bottom line: tighter lending and lower housing values, derivatives and market losses, margin calls and job losses--they all add up to less money being borrowed and spent and less money available to spend because it was just lost in the market. Less money being spent means recession. I wonder what part of this equation the bullish pundits don't understand. Frequent contributor U. Doran was kind enough to forward a recent report from the-privateer.com (subscription service; thank you, U. Doran, for sharing it with us), which substantiates some of the major points listed above: The ISM (Institute for Supply Management) index fell to 49.3 percent in January, the lowest level since April 2003 and below the key 50 percent line, indicating that most firms in the factory sector are not growing. The index had stood at 51. The decline in US inventories was breathtaking. In January, inventories dropped by the largest amount since 1984, dropping to 39.9 percent in January from 48.5 percent the previous month. This is the lowest level of inventories since February 2002. The ISM survey committee said the �major sign of weakness� was the low level of order backlogs which fell to 43.5 percent from 45.0 percent in December. The National Association of Purchasing business barometer fell to 48.8 from 51.6 in December. The REAL numbers are all negative.And from the Financial Times: But the investment banks that fuelled the craze of lending to borrowers with weak credit histories look like they are escaping relatively unscathed. Amid increasingly ominous signs of a shakeout in the subprime mortgage industry, investors in securities backed by these risky mortgages have seen the value of their holdings slide this year. Risk premiums - or the spreads over government bonds - on the lowest-rated cash securities have risen by up to 400 basis points, while the cost of insuring such deals against losses through the derivatives market has doubled.I wonder how many pundits in the financial press issued a warning as pointed as I did Monday any time in the past 2 weeks. I think the answer is near-zero. I wonder if the average investor who gets a margin call tomorrow will suddenly become more skeptical of the "happy-happy, always Bullish, all the time" media coverage he/she has been reading/watching for the past five years. I wonder if anyone will become angry at the screaming "mad money" types who have relentlessly hyped and pumped stocks for the past five years. I wonder just how disappointed hopeful speculators will be when they realize the Fed can't lower interest rates for the simple reason it has to raise rates to defend the dollar. I wonder how long the charade of "permanent prosperity based on borrowing more" and "there won't be any recession this year" will continue. If the stock market falls by 20% or more, it will certainly be more challenging to maintain the ruse which has worked to perfection for five long years: you're richer, because you borrowed more. Here's the party line, issued today by the AP wire service: Economists Say Recession Unlikely. February 27, 2007 "I Wonder". . . What Will Happen in China  Dear Readers: I wrote this last night but wanted to add some further comments, so I

didn't post it. Events caught up with me, however, as the China stock market plunged 9%

and as I write this, the Dow Jones is down 130 points and Nasdaq is down 45 points. The

"correction" I called for Monday has begun, and gold has dropped, also as I suggested

it might.

Dear Readers: I wrote this last night but wanted to add some further comments, so I

didn't post it. Events caught up with me, however, as the China stock market plunged 9%

and as I write this, the Dow Jones is down 130 points and Nasdaq is down 45 points. The

"correction" I called for Monday has begun, and gold has dropped, also as I suggested

it might.

Continuing this week's theme of "I wonder"--I wonder how long the Shanghai stock market can go before it crashes a la the dot-com Nasdaq market in 2000. This chart (from a story recommended by frequent contributor U. Doran) is the picture of unsustainability. This chart forces us to wonder: when this market rolls over and blows up, will there be any consequences in the U.S. and global markets? Frequent contributor Albert T. pointed out another potentially hazardous connection between the U.S. and China: China's proported interest in buying risky, high-return mortgage-backed securities: This is news to me but I was thinking, who is going to hold the bag when the housing market goes bust? I found this and basically started laughing. The article is below...Excellent work, as usual, Albert T. I wonder if the Chinese fund managers are being pressed to find "alpha," (returns above the benchmark), and are therefore turning to higher return investments like mortgage-backed securities and CDOs without fully understanding the much higher risks. I wonder if China will mis-allocate its foreign reserves, just as it has largely mis-allocated the billions of foreign investments and its own government spending. I wonder when American will "get it" that the dollar/yuan level is meaningless because if China gets "too expensive" for manufacturers--say, its factory wages rise to $300 a month--the factories will not be shipped to the U.S. and its $3,000 a month wages and $1,000 a month medical insurance, but to Vietnam, Cambodia, Bangladesh, etc. February 26, 2007 This Week's Theme: "I Wonder". . . If the Stock Market Will Roll Over This week's theme is "I wonder"--as in, I wonder if the stock market is about to roll over into a sharp descent. To get the wonderment ball rolling, let's look at three charts: the SPX, a broad measure of the U.S. stock market; the VIX, a measure of near-term volatility, and the XAU, a broad measure of gold and silver, all in three-year timeframes.

Looking at the steep climb of U.S. stocks for the past 7 months, I have to wonder: is the economy really that much better now than it was over the previous 3 years? The market has screamed upward for over 7 months as if the economy is near-perfection. Uh, right. Did anyone say "subprime mortgage meltdown"? Rising oil prices? Declining GDP? Negative savings rate? And how about that flattened MACD? Looks pretty toppy, as does that 6 months of uninterrupted overbought stochastic.

The VIX, declining steadily for the past 3 years, fairly shouts, "No worries, Mate!" If you looked at this chart and nothing else, it might seem surprising that the yield curve has been inverted for months, industrial capacity utilization has dropped below 50 (big red flag), oil has risen from $50 to $61, the market has risen for nearly 8 months without so much as a hiccup, setting a record unmatched unless you go back 50 years to 1954...and those nasty subprime loans blowing up. Hmm. Nothing to worry about, eh? I wonder--if the market gets a whiff of reality, perhaps it will be cut down much like Napoleon's whiff of grapeshot cut down the mobs of Paris. (A thousand pardons for the egregious historical reference.)

And speaking of bullish: how about that gold? Wooie. Virtually every gold pundit and analyst out there is calling for $730 gold, $780 gold, and then that magic $1,000 gold. But a funny thing tends to happen on the way to unanimous super-bullishness: when everyone is in agreement that something can only go up, everyone usually turns out to be wrong. If it were that easy, we'd all be millionaires. First, there's that big wedge in the XAU. Yes, it might bust out to the upside, as everyone from 8 to 80 seems to be predicting. But then look at the MACD and the overbought stochastic, and a tiny doubt introduces itself, if not about the inevitability of the ascent to $730, then perhaps about its longevity. What could cause the market to roll over into a long-awaited correction? What fly could make its way into the ointment of the gold market? I don't know, but the charts make me wonder. Cold cereal mystery solved: In Friday's entry, I was puzzled by a reader's report that Kashi Go Lean had reduced its fat, sugar and salt content, yet the Go Lean package at Costco was unchanged. It turns out that some legerdemain in the serving size is the magic: by reducing the stated serving size on smaller packages of their product from 190 calories to 140 calories, the fat, sodium and sugar per serving is also magically reduced--not in the product, but on the "nutritional information" label. Talk about having to read the fine print. February 23, 2007 Healthiest Cold Cereal Revisited My entry from July 13, 2005 on "the healthiest cold cereal" shows up every month as one of the top search topics which direct readers to my site. For your amusement, I reprint it here. A reader recently claimed that the Kashi Go Lean nutritional data posted here was no longer current. But when I went to Costco yesterday and examined the package, I am hard-pressed to find any changes from the data I noted in 2005 except perhaps an increase in potassium--a data point I did not note in 2005--which is a common "salt substitute". My conclusion remains: Go Lean contains significantly higher levels of fat, sodium and sugar than other packaged cold cereals, and remains a deceptively labeled and marketed product in my view. Is a cereal with three times the fat of Mini-Wheats, one more gram of sugar than Mini-Wheats, and 19 times the salt of Mini-Wheats a "healthier" "leaner" cereal? On what basis? This kind of "read the fine print" deceptive packaging is rife in the American food industry, and it makes it very difficult for consumers to sort out what's actually healthy for you. In a fair analysis, Go lean cannot be considered a "healthy" food compared to plain old oatmeal with 0 fat, 0 sodium and 0 sugar--or in my view, Mini-Wheats. Here is the original 7/13/05 entry: And the Healthiest Cold Cereal Is: Frosted Mini-Wheats! I'm joking, right? Those sugar-encrusted little rectangles of wheat, healthiest of all? But I jest not. After a careful review of cold cereals at the local Costco, it seems clear that Frosted Mini-Wheats have the least harmful combination of bad things (fat, sugar and salt) and the highest content of good things (protein and fiber). The big shocker was the high sodium (salt) content of so many of the cereals. If I was of a conspiracy bent of mind, I would suspect the pharmaceutical industry of secretly paying the cereals companies to load up their seemingly benign products with salt, thereby causing ever higher blood pressure in unsuspecting Americans, who would then require that many more doses of highly profitable blood-pressure reduction drugs... The second surprise was that the "healthier alternatives" (Raisin Bran and Kashi brand Go Lean) had excessive amounts of sugar and salt, decisively lowering their score in the "healthiest cereal" contest. But let's not get ahead of the analysis. Highest sugar content: Sugar Frosted Flakes? Nope: Raisin Bran (19 grams per serving), followed by Kashi brand Go Lean with 13 grams. (Some health food, eh?) Frosted Flakes and Frosted Mini-Wheats came in with 12 grams each. Good old Cheerios scored lowest with 1 gram, right in with Oatmeal. Cinnamon Toast Crunch scored high with 10 grams, and Wheat Chex tipped in with a modest 5 grams. Most calories from fat: Cinnamon Toast Crunch clocked in with 30 calories of fat in each 130-calorie serving (guess where the "crunch" comes from). Go Lean came in with 25 calories of fat in a 190-calorie serving, while Frosted Flakes checked with the lowest of all, 0 calories from fat. Way to go Tony! Mini-Wheats had only 10 calories of fat per serving. Highest salt content: Cheerios has 210 mg. of salt in each serving, as does Cinnamon Toast Crunch; Raisin Bran is weighed down by 300 mg. of salt, while Wheat Chex must be made in the Salton Sea, for it has a staggering 420 mg. of salt per serving--fully 20% of all the salt you should eat in a day. Meanwhile Frosted Mini-Wheats has only 5 mg. of salt, comparable to wholesome plain cooked Oatmeal with 0. Highest Fiber content: Tony the Tiger doesn't do too well on this one with only 1 gram of fiber--ditto for Cinnamon Toast Crunch. Cheerios comes with 3 grams of fiber, while Mini-Wheats contains a respectable 6 grams; leaders are Raisin Bran and Go Lean with 8 grams each. Highest Protein (cereal only, no milk): Go Lean tops out with 9 grams of protein, but Mini-Wheats comes in second with 6 grams, good old Oatmeal does well with 5 grams, while Cheerios and Honey Bunch of Oats score 3 grams and protein-deficient Tony the Tiger (Frosted Flakes) stumbles in with only 1 gram. Conclusion: if you look not just at sugar, calories and fat, but at salt, fiber and protein, then it's clear that Frosted Mini-Wheats is the healthiest all-around choice of uncooked breakfast cereals. Yes, the sugar content is high, but it's less than Raisin Bran or Go Lean, supposedly "healthier" cereals. With super-low sodium, it's my top pick for an "honest" cereal, right up there with oatmeal. All that extra salt in packaged foods is a real detriment to health. Mini-Wheats also scores at the top in fiber and protein. So what's not to like? Sure, Oatmeal is a healthy choice, and I eat a lot of it (with flax seeds for all that yummy omega 3)--but with honey, and who knows how much sucrose I add in that "healthy choice" fashion... maybe as much as those 12 grams on the the Mini-Wheats.... February 22, 2007 Causality and Patterns A question from astute reader V.N. alerted me to the potential for confusion between causation and pattern in the Pareto Principle. V.N. asked what I was proposing as the causal mechanism behind my proposition that 4% of mortgages entering delinquency could trigger widespread declines in 64% of the housing market. My answer: I wasn't suggesting a causal mechanism as much as a pattern of Nature which may apply to housing as it does to income distribution, etc. Thus we cannot say that 2 million of the outstanding 50 million mortgages turning sour will necessarily trigger a widespread decline; we can only be alert to the possibility that the housing market will follow patterns such as the 20/80 and 4/64 rule. In a similar fashion, we can look at these two charts of stock market history and note some eerily prescient correlations between then and now:

In all three cases--1929-1936, 1966-1973, and 2000-2007--a multi-decade market high was followed by a precipitous decline and an ensuing 7-year recovery--at which point another precipitous decline occurred. As you know, the global stock markets hit euphoric highs in March 2000, and now we find ourselves just days away from March 2007. The Nikkei has just reached 18,000 for the first time in seven years, the Dow Jones continues to hit new historic highs, and so on. Could the next "unexpected" sharp decline in global stock markets be just around the corner? We can't say what might cause such a wealth-crushing drop, but we can note the similarities to patterns which have recurred in the past. Pareto Principle Housing Update: Mish just posted an excerpt from a USA Today story on housing price pressure in Sacramento, CA: Here's an alarming fact about Sacramento's housing market: About one of every five existing homes (20%) on the market is a "short sale." That means the home is worth less than the value of the mortgage, and the lender is willing to accept less than full repayment of the loan to avoid foreclosure, says Tracey Saizan, president of the Sacramento Association of Realtors.20% of the homes/mortgages/homeowners on the market are in trouble, and the other 80% are feeling the effects. 80/20, 20/80, take your pick. February 21, 2007 Can 4% of Homeowners Sink the Entire Market? If 4% of all American homeowners fall into foreclosure, could that "small number" cause a collapse in the entire housing market? The Pareto principle says: yes. Despite months of suspiciously negative data--housing sales and starts sagging, cancellations of sales and foreclosures rising--housing apologists have maintained that the problems with subprime borrowers and lenders can be "contained." In other words, only those "few" who lose their homes will suffer any economic impact; Home Depot and Lowes sales will remain robust, construction activity will continue unchanged, employment in construction, home furnishings, remodeling, lending and real estate will continue to hold up with minimal declines, etc.

That's the happy story. Let's get some facts before we buy into it. Here is a recent story in the Wall Street Journal: Sharp Drop in Housing Starts Adds To Fear of Wider Economic Impact (2/17/07) (subscription required) So far, defaults and late payments have remained very low on prime mortgages, which are made to lower-risk borrowers and account for the bulk of home loans. But late payments have risen swiftly over the past year on subprime mortgages -- those made to risky borrowers with spotty credit histories -- and on "Alt-A" mortgages, a category between prime and subprime which includes many loans for which borrowers haven't documented their income. According to trade publication Inside Mortgage Finance, 13% of mortgages outstanding are subprime.But if we dig a little deeper, we find that seems to understate the true scope of delinquencies and foreclosures. Here is the Financial Services Fact Book: Adjustable rate mortgages, loans in which the interest rate is adjusted periodically according to a pre-selected index, accounted for 31 percent of mortgage originations in 2005, up from 12 percent in 2001.The factbook also lists some very interesting charts of delinquencies: 12.9% of all FHA loans are delinquent. Are these listed as subprime? No. These are "conventional mortgages." The Factbook also states that 24.7 million homes are owned "free and clear," with no mortgage, and about 50 million have mortgages of one kind or another. About 10 million homeowners have equity lines of credit as well as a mortgage--in effect, second mortgages. Though rarely mentioned in all the hoopla about subprime ARM (adjustable rate) mortgages, it is important to note that equity lines of credit are adjustable-rate loans; they are not 30-year, fixed-rate "conventional" mortgages. The upshot: 10 million homeowners who statistically have "safe" conventional mortgages are at risk of their home equity line loans re-setting to higher rates. There's about $9 trillion in home mortgages on the books, and $500 billion is due to re-set higher. More Americans are losing their homes: Nothaft estimates that $500 billion in variable rate mortgages will reset, or rise, sometime this year, leaving many with a payment they can no longer afford. �Those would be the candidates for � delinquent status,� he said.Meanwhile, back at the ranch, Number of vacant homes for sale surges 34% The number of vacant homes waiting to be sold surged 34% to 2.1 million at the end of 2006 compared with the end of 2005, by far the fastest increase ever recorded, the Census Bureau reported Monday.According to the Financial Times, The inventory of new and existing homes waiting for buyers is now approaching 4m. The total value of US residential property is now around $19 trillion, according to the Joint Center for Housing Studies at Harvard University. The US Census Bureau calculates that there are around 123.9m housing units in the US. (ED: this includes condos and rental apartments)Total household debt is $11 trillion: $9 trillion in mortgages and $2 trillion in revolving credit (credit cards, etc.) That means net equity for all 75 million American homeowners is $8 trillion--including the 25 million households who own their homes free and clear. What if we subtract those folks? Since 1/3 of all homes are owned free and clear, let's assume about a 1/3 of the $19 trillion is represented by these mortgage-free homes. That's $6.5 trillion, which means all 50 million mortgage holders are left with a grand total of $1.5 trillion in net equity. If housing values decline 15%, that's a $2.85 trillion haircut off net equity. If we set 2/3 of that against mortgaged real estate, (the other 1/3 being a decline in the value of free and clear homes), then the decline collectively suffered by all mortgage holders is $1.9 trillion--enough to put them in a negative equity hole. This is a staggering conclusion, for it suggests just how a "mere" 4% delinquency/foreclosure rate could trigger a "modest" 15% decline in housing values, which would put the nation's mortgage holders (if taken in aggregate) under water: the nation's household debt would exceed the value of the mortgaged residential real estate. So let's put this together. With the Pareto Principle in hand, we can foresee the distinct possibility that when a mere 4% of outstanding mortgages enter delinquency / foreclosure, then a "tipping point" will be reached, triggering effects which far outsize the proximate causes. Please examine the chart above carefully. Over 69% of the population are homeowners, and another 26% are in poverty. According to the FDIC, the recent surge in ownership from 64% to 69.5% has created a pool of "at-risk" borrowers who couldn't have purchased a house with a conventional mortgage. Of the remaining 4% who are not homeowners or those living below the poverty line, the recent stalling home ownership rates at about 69.1-69.7% suggests these households are just above the poverty level and unable to buy a house, not yuppies renting penthouse suites who are now ready to buy a McMansion. There are 50 million mortgages. If 4% is the magic number, that's 2 million mortgages. In other words, when 2 million mortgages enter delinquency / default, then according to the Pareto principle, that will affect the 64% "trivial many," i.e. those holding "safe" conventional mortgages. According to the FDIC, about 4 million recent buyers are at risk of defaulting. Recent news items suggest 1 million subprime mortgages are already in that category. There are at least 6.7 million subprime loans outstanding, and if 13% are in foreclosure, that's nearly 900,000. We can be confident that a much larger number are delinquent, and that lenders are scrambling to keep them out of foreclosure. Also recall that 13% of FHA loans--"conventional fixed-rate mortgages"--are already in delinquency. (see Factbook link above for the chart) So while the foreclosure rate on those mortgages is still low--2% or so--the pool of potential foreclosures is large, and increasing. How close are we to the "tipping point" where a "small" 4% (2 million defaulted mortgages) will cause 64% of the effects, i.e. declines in housing prices? If you total up delinquencies, it would seem we are already well over the 2 million mark. As for 2 million foreclosures--the clock is ticking. Here's a question that deserves to be asked: if everyone who can afford a house--even those who stretched their credit to the breaking point--has already bought a house, then who's left to buy the 4 million empty dwellings? Please don't say someone who's selling their existing house--they're adding one unit of inventory even as they take one off. If you add up the facts presented above, it is difficult not to reach disturbing conclusions: there is no way buyers will emerge to snap up 4 million empty homes; the number of mortgages in delinquency is large, and rising, meaning the number of foreclosures in the future pipeline must also rise; once 2 million mortgages/homes are in foreclosure, a "tipping point" may well be reached which will lead to significant declines in all housing values far in excess of the supposedly "contained" "small" number of delinquent / foreclosed loans. Here's another way to consider the possible Pareto effects: if 20% of the housing stock in the "hot markets" of Florida and the West and East coasts declines in value, then will that cause a decline in 80% of the U.S. home market? Some other links of interest: Patterns of Housing Decline: "Core and Periphery" (recommended by frequent contributor U. Doran) After Subprime: Lax Lending Lurks Elsewhere (2/20/07) (Wall Street Journal Online subscription required) Foreclosures and Financial Ruin: How Bad Will It Get? (April 26, 2006) How Many Foreclosures Will Hit the Market? (May 1, 2006) February 20, 2007 Hedge Funds and The Pareto Principle Frequent contributor Harun I. invokes The Pareto Principle (the 80/20 rule) in an incisive analysis of last week's entry on hedge fund returns and alpha: What BGI (Barclays) does is what every technical trader attempts to do: develop a trading model with a statistical edge. The statistics sited are constant with the Pareto Principle (see below). I have found that what limits the trivial many investors and traders is an unwillingness to turn off the news, learn something about statistics, develop and rigorously test trading models and money management models and to understand the process of Group Rotation.

In other words, "the vital few" (20%) influence effects more than the "trivial many" (80%). As for regulation/unregulated: I must cop to not thinking through what "unregulated" means, given that who is allowed to invest in "risky" hedge funds is in fact highly regulated. This reminds me yet again not to take easy phrases for granted. Here is the Wikipedia link to The Pareto principle. This is a special case of the wider phenomenon of Pareto distributions. If the parameters in the Pareto distribution are suitably chosen, then one would have not only 80% of effects coming from 20% of causes, but also 80% of that top 80% of effects coming from 20% of that top 20% of causes, and so on (80% of 80% is 64%; 20% of 20% is 4%, so this implies a "64-4 law").If the "vital few" make most of the money in the hedge fund world--the Pareto distribution suggests 20% of the funds garner 80% of the returns, and only 4% have more influence on the markets than 64% of the "trivial many"--then we also discern the outlines of how a financial meltdown can occur with sudden, unexpected speed: the 4% of hedge funds who have over-extended leveraged bets on derivatives could bring down the entire derivatives market, even though it appears that their holdings are too limited to trigger such widespread havoc. February 16, 2007 A Random List of Films As a break from the relentless euphoria of the stock and bond markets, let's look at some movies. I keep a list of films I've seen, in no organized fashion, and just for laughs here's a few from last year's list--in no particular order. If you're searching for something to add to your Netflix queue, it might be fun to check these out. You'll quickly note that I like world cinema in all decades. Sea of Love (1989, director, Harold Becker) Al Pacino doing Al Pacino as a tough, boozing, conflicted cop who's falling in love with Ellen Barkin. If you hate Al Pacino, don't see the film. If you love Al, or gritty crime thrillers, go for it. A worthy script and one of his finest performances. Yesterday, Today And Tomorrow (1964, director, Vittorio De Sica) Three tales of sex and romance with the sumptuous sophia Loren in her prime, and Marcello Mastroianni as both an anxious "customer" in one story and a good-hearted working-class bloke who must keep his wife pregnant in another. If you haven't sampled much Italian cinema of the glorious 60s, this charmer is a good intro. Delightful perfomances by Loren and Mastroianni. La Strada (1954, director, Federico Fellini) Considered a classic by many, and certainly one of Fellini's most accessible and affecting films. Anthony Quinn (yeah, the American actor, dubbed into Italian) and ingenue Giuliette Masina are heart-rendingly true in this tale of a doomed romance. This is subtitled, and in black-and-white, which for reasons I have never figured out is a turn-off to many American film-goers. Lost Horizon (1937, director, Frank Capra) Famed director Capra's beautifully filmed version of the Shangri-La (Shambala) story, of a secret Himalayan kingdom where death has been banished. Some of the dialog may remind you of Yoda (from the Star Wars series), but the basic precepts of Buddhism are imparted without too much pain. This is a worthy 30s film, with much of the "treatment" which makes these films favorites 50 years later: great cinematography, a little adventure, a little romance, great costumes, and everything played "big." In other words, the evil people are visibly evil, the hero is clearly heroic, etc. All About My Mother (1999, director, Pedro Almodovar) Director Almodovar is famed for his insightful, sympathetic stories focused on women and this is one which won't disappoint. A tremendous cast of Cecilia Roth, Marisa Paredes and Penelope Cruz (among others) will reach right in and pluck your heartstrings. Almodovar has a knack for pulling off slightly wacky plot devices, and here we have a transvestite father who didn't know he was a father--until now. Oldboy (2004, director, Chan-wook Park) A very dark Korean morality play which is very over the top in plot development and violence. Korean cinema is hot right now, and has been for a few years. I think one reason is the Korean directors have explored edgy themes with great stylistic flair. Themes, like, well, eating your neighbor, as in cannibalism. Here we have a revenge plot worthy of the Count of Monte Cristo in its planning and execution. This film was too violent and emotionally unbelievable for my tastes, but if you want to see a film which exemplifies the no-holds-barred visuals and themes of recent Korean films, this might be your ticket. My list of recently viewed worthy films has about 40 titles, and there are so many others I would like to share which you may not have seen: Boudu, The River (French), 2046, Kung Fu Hustle (Chinese), Baran (Iranian) and McCabe and Mrs. Miller (American), just to mention a few more. Note: I am pushing ahead on a big writing project and so my entries next week might veer into the slight/zany. I apologize in advance for any disappointment. February 15, 2007 Who's Getting Alpha? Hedge funds--those loosely regulated funds reserved for rich folks and institutions--like to claim they outperform the market (alpha). But is that true? It's an issue, of course, because of the enormous rise in the number of hedge funds and in the assets they manage:

First, let's consider what the hedge funds skim for themselves and churn in brokerage/trading fees. In the standard "2 and 20" structure, the managers receive 2% of the assets they manage as a management fee and keep 20% of the profits as incentive pay. How much does that add up to? For comparison, let's consider the Wall Street (non-hedge fund) bonuses: Wall Street executives hit $23.9 billion: (USA Today) This year's bonus pool for Wall Street executives hit $23.9 billion, the New York State Comptroller's office estimates. That's a 17% jump from last year's bonus pool of $20.5 billion, and it works out to an average bonus of $137,580 for every person employed in the financial services industry.Sounds cushy, but this pales in comparison to what the hedge fund managers pay themselves:

Wall Street giants� compensation still pales in comparison with their hedge fund counterparts: (New York Times) In 2005, the top hedge fund manager took home $1.5 billion in pay while the price of entry to be on the list of the top 25 paid managers, compiled by Institutional Investor�s Alpha magazine, was $130 million. Here is the top 10 hedge fund managers' income: The full top 10 list of hedge fund earners according to Trader Monthly includes: 1. T. Boone Pickens - estimated 2005 earnings $1.5bn + 2. Steven A. Cohen, SAC Capital Advisers - $1bn + 3. James H. Simons, Renaissance Technologies Corp. - $900m - $1bn 4. Paul Tudor Jones, Tudor Investment Corp. - $800m - $900m 5. Stephen Feinberg, Cerberus Capital Management - $500 - $600m 6. Bruce Kovner, Caxton Associates - $500m - $600m 7. Eddie Lampert, ESL Investments - $500m - $600m 8. David Shaw, D.E. Shaw & Co - $400m - $500m 9. Jeffrey Gendell, Tontine Partners - $300m - $400m 10. Louis Bacon, Moore Capital Management - $300m - $350m 10. Stephen Mandel, Lone Pine Capital - $300m - $350m Here's an excerpt from Barron's Up and Down Wall Street: The average pay of the top 126 hedge fund managers last year was $363 million, up some 45% from the year before.Clearly, the hedgies pay themselves handsomely. But they also generate huge fees from "churning" or trading their immense holdings. The Great Unwinding Is Coming (Financial Times, Alphaville) Transaction costs run to 4 per cent of the $1,300bn of hedge fund assets under management. Manager salaries and performance fees take another 4-5 per cent, meaning hedge funds need to generate average annual returns of close to 20 per cent to keep everyone happy (including their investors).And here's an interesting piece passed on by contributor U. Doran on the high rate of churn in today's markets: Underreported, Understated And Certainly Not Understood.

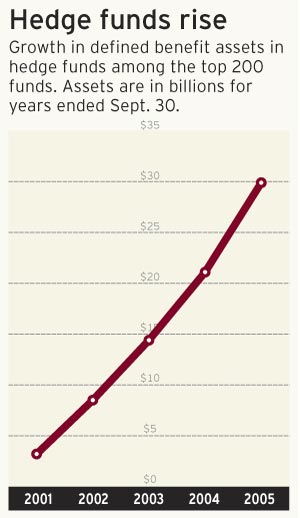

So how much alpha is left for the hedge fund clients? Not all the clients are rich folks with too much money; as this chart shows, pension funds--"defined benefit plans"-- have been rushing into hedge funds, hoping for that illusive alpha. In fact, the "quant shop" hedge fund Barclays Global Investors (BGI) profiled in the BusinessWeek story below largely trades ETFs (exchange traded funds) for the benefit of its 2,800 institutional clients like pension funds. The firm manages $1.62 trillion. From Outsmarting the Market: (BusinessWeek) Over the last five years the S&P 500-stock index has outperformed 71% of large-cap funds, the S&P MidCap 400 has topped 83.6% of mid-cap funds, and the S&P SmallCap 600 has bested 80.5% of small-cap funds, according to Standard & Poor's, a unit of The McGraw-Hill Companies.So BGI--one firm--skims 15% of the entire global haul of alpha. How much of the remaining $25 billion is divvied up amongst the other 9,000 hedge funds? That's an awful lot of thin (or non-existent) slivers. In summary: Wall Street pulls down $23 billion in bonuses (not counting salaries and stock options, mind you--this is all cash), hedge fund managers pay themselves another $30 billion or so (the top 10 pulled down $7.5 billion themselves), and global investors got a grand total of $30 billion, or .1% --a meagre tenth of a percent--of the global market's value in alpha. Pardon me for being underwhelmed by the fantastic returns being generated by hedge funds and their Wall Street pals who execute the trades and arrange the lucrative buyouts. Meanwhile, back in the real world, as more and more Americans fall behind on their mortgages, Banks Try to Return High-Risk Loans To the Originators. February 14, 2007 Hedgies Anonymous  In my unending quest to monetize this humble site, I designed this ad for a new

self-help group, Hedgies Anonymous.

In my unending quest to monetize this humble site, I designed this ad for a new

self-help group, Hedgies Anonymous.

With somewhere between 9,000 and 10,000 hedge funds--one for every tradable equity in the U.S. markets--countless hedgies are suffering from addiction to borrowing and leveraging leverage. Swelling the mighty hordes of wretched victims of addiction are the employees of private equity firms, which specialize in borrowing vast sums, buying public companies, and then stripping them of assets. For these rapacious souls, an addiction to looting and pillaging is almost as powerful as their addiction to borrowing billions. We all know the explosion of hedge funds and the desperate search for alpha (any gain above the standard benchmark, usually the S&P 500 or the Wilshire 5000) will end badly, and Hedgies Anonymous is gearing up to offer solace to the thousands who will lose their livelihood and fortunes when the derivatives house of cards the hedgies have so carelessly constructed blows away in the storm of an unexpected "financial crisis." When those winds sweep away the leveraged leverage of derivatives, then Alpha will be reduced to "losing less than everyone else." February 13, 2007 The Cover of BusinessWeek as Lending Implosion Bellwether Two readers alerted me to the bellwether aspect of this week's BusinessWeek cover, which boldly states: "It's a Low, Low, Low, Low-Rate World: why money may stay cheap longer than you think." Astute reader B.G. Cooke asked: Have you seen the cover of the recent Businessweek magazine (low, low, low rates)? Wouldn't you say that that is a contrarian indicator?While frequent contributor U. Doran characterized the cover as a "Mega Historic Mkt call." Let's consider the lending and low, low rates which most directly affect typical Americans: mortgage lending and interest rates. Here is a graphic depiction of recent events in this astonishingly permanent world of low, low rates:

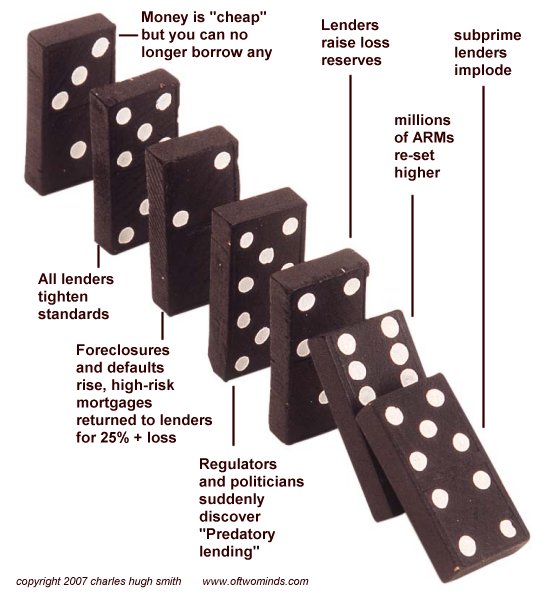

So, yes, I would have to agree that this BusinessWeek cover is the high water-mark of cheap, readily available money, at least in the mortgage market. As you probably know, Newsweek ran a cover on "the housing boom" in mid-2005, which eerily marked the top of the bubble, and The Economist is famous for running covers announcing the demise of the dollar, just before the dollar rallies strongly. I suggest starting your research on Domino 1 (subprime lender implosions) at Aaron Krowne's Mortgage Lender Implode-o-Meter. Congratulations, BusinessWeek, for nailing the top of the "low, low rates" and cheap, easy money mortgages. February 12, 2007 A Fibonacci Analysis of the Housing Market: Where We're Heading Readers familiar with stock market analysis know about the Fibonacci series, and how stock prices tend to rise and fall to levels corresponding to Fibonacci numbers: .382, .618, etc. The way this works is straightforward: if a stock (let's use a fictional one such as Predatory Subprime Lenders Corp., PSLC) rises from $10 to $20, and starts descending, then with a Fibo analysis we can predict the levels it will likely fall to in a stairstep down. We take the size of the move up--$10--and then multiply it by the Fibo series: $3.82, $6.16, and so on (there are intermediate numbers, as well as 1.382 and 1.618.) Next, we subtract that Fibo number from the price peak. Thus our first target for PSLC on the way down is $20 (its top price) minus $3.82, or $16.18. After the stock breaks through that level, we can then look for it to fall to $20 - $6.18 or $13.82. In a full-re-trace, the stock descend back to $10. Since the Fibo series can be applied to any chart of prices, why not apply it to the housing market? Here is a chart of California median home prices over the past 10 years, and a simple Fibo analysis of its price move up, and what we can expect on the way down.

Inflation complicates our analysis. Thus a "new high in the Dow Jones Industrials" in nominal prices doesn't mean the value has returned to its value in 2000--adjusted for inflation, the DJI is still well below its value in the dot-com peak. To keep things simple, I've kept the Fibo targets in nominal (non-inflation adjusted) dollars, except for the starting price. In other words, in 1995 the median price was about $175,000. If the price had risen only with inflation (as defined by the Bureau of Labor Statistics), then the median price would be $231,000 in 2006. If we look out to what prices may be in 2011, five years hence, we have to keep inflation in mind. If we assume inflation continues at a low rate of 3%, then we find that the $175,000 in 1995 would have to be worth $266,000 just to keep up with inflation. If it is worth less than that, it represents a decline in value. Let's look at our Fibo analysis of the future:

Another feature of price movements is symmetry: what takes five years to rise often takes a similar amount of time to decline. Applying these two simple but powerful concepts--Fibonacci series and symmetry--to the chart of median housing prices in California, we find that in terms of inflation-adjusted value, the price will reach a full re-trace in mid-2011. In other words, the house purchased for $175,000 will have returned to its starting value when the price hits $266,000 in 2011. Should the the price of the house fall below $266,000, the owner is experiencing a net loss in value. While it may give psychological comfort to the owner that the house he purchased in 1995 for $175,000 is still worth (say) $250,000 in 2011, the $75,000 "profit" or "increase in value" is pure illusion. Adjusted for inflation, the owner is under water by $16,000. Yes, a home is more than an investment. But it should still be analyzed with the same rigor as any other investment. If it can't maintain its value when adjusted for inflation, it is a losing investment. February 10, 2007 More on Pensions, and a Stock Market Correction? First up, some reader feedback which suggests there is a growing "us" and "them" divide in the U.S.: those with publicly funded pensions and healthcare benefits, and the rest of us with Social Security, at-risk 401Ks and IRAs and Medicare when we hit 65. Reader Kevin M. highlights just how rich California public pensions can be: ! enjoyed your blog on the problem of the public pensions. A good friend of mine, who happens to be a retired Major from the San Diego Police Dept. was shocked to learn how little I make a year (I'm an Idaho State Trooper). I was stunned to learn what he makes in retirement, a little over twice what I make a year!! I remember telling him, "now I understand why California is going broke!"We all know California is expensive, but so is Hawaii, and their public pensions are far lower than California's. I suspect the public unions and their members fail to grasp the public's growing resentment of their "gaming the system" and other "wink-wink" legerdemain which boosts publicly funded pensions far beyond the intended scale. The unions would better serve their membership by cracking down on this kind of abuse before the outraged taxpayers take away the entire gravy train. Personally, I think it's already too late. As the recession starts biting deeply into tax revenues, municipalities will be filing bankruptcy left and right, and states will have to choose between raising taxes to fund the pensions (and thereby sparking a taxpayer rebellion) or trimming the "fat" (i.e. abuse, double-dipping, gaming of the system) from the public pensions. For more on fairness and the notion that government workers are underpaid and thus deserving of generous pensions far beyond what private sector workers could ever dream of, here is a commentary from reader Brian H. which reflects what many feel but few express: While the public employee didn�t get any stock options, he also didn't work more than 40 hours. Gets paid overtime, gets a bazillion weeks of paid vacation, real health, retirement and���..I recall a recent open-call for applicants to a major city fire department in which hundreds of people showed up for a handful of positions. Yes, people aren't stupid; everyone wants a job with limited hours from which you can't be fired and a guaranteed generous pension after only 20 years of work. Fellow blogger Fred Roper (Satellite Sky) believes we would be better served with a true national pension plan: Social Security is / was meant to be a supplement to a pension. I think that Social Security could be converted into a pension system if we ended the Social Security and Medicare taxes limitation to the first $120K of income. Then we could fund a full pension and national health care system. The payroll taxes could be reduced for all workers since more would be contributing. The payroll tax is one which wage earners pay. I have never had anyone explain to me why the wage earner under $120K should bear so much of the financial tax burden.Thank you, readers, for your comments on a topic which I believe grows more pressing with each passing day. And before the stock market tanks next week, I wanted to predict its long-awaited "correction." Nothing rises forever, and this Bull uptrend from mid-July has extended into a 7-month stretch which is basically unprecedented in duration. (Bull markets tend to pause every few months for a 3-5% decline called a "correction" in Wall Street Speak.) All good things must pass,alas, and it now looks like the market has crested and the inevitable decline is starting.

The general mood of the market is very bullish and very complacent--the perfect setup for a major decline. All the news has been good, month after month, with no flies in the ointment. But then what happens when all the good news is out? February is typically a poor month for the market, and uninterrupted uptrends don't last past 7 months (gee, it's been 7 months almost to the day!) It's certainly something to ponder. February 9, 2007 Recession Warnings Frequent contributor Aaron K. (and proprietor of the fabulous The Mortgage Lender Implode-O-Meter sent in a cogent commentary on the scale-invariance evidence for a recession in his region of the country. I find his evidence very persuasive, as it coincides rather eerily with what I see myself here in the "hot housing market" "prosperous" S.F. Bay Area: I agree with the point about scale-invariance, and that basic insight has given me a lot of insight about the economy in the past year. Further, I live in Atlanta, which would probably win a contest for the best "Everytown, USA", so I take note of what goes on around here. Here are some things I've noted:Knowledgeable reader John M. gently took issue with my broad-brush indictment of public-employee pensions. I should have qualified my focus by saying that the problem is not the majority of hard-working public servants who toil away for decades, but a minority who "game the system" or simply lie/cheat/deceive with no penalties or indeed, no disincentives to cheating the taxpayers. My main point was: regardless of the merit of public employee pensions and medical benefits, they are unaffordable and will drive cities into bankruptcy. Here are John's comments: I'm a long-time reader of your column and I have to take issue with your characterization of public employees. I agree that there are some egregious examples of greed in some of the public sector - and you didn't even get into the perks that politicians and office holders grant themselves - but there are many public employees that don't fall into that category.For those interested in Chapter 9 bankruptcy (a special catagory reserved for municipalities), blogger/attorney Fred Roper (Satellite Sky) was kind enough to send this link. I recommend reading it, for then you'll understand why Chapter 9 bankruptcies will soon be news all over the country. Distressed Cities See No Clear Path. February 8, 2007 Will "Creative Destruction" Save the U.S. Economy? The topic of a politically powerful minority raking off oversized benefits from the public at large drew this commentary and recommendation from knowledgeable reader Peter on the fascinating work of American economist Mancur Olson: (emphasis added) The central argument is, a minority group can find it to its advantage to impose on society as a whole costs which are many hundreds or thousands of times the benefits the group itself gets.In other words: periods of peace enable political and financial stultification. One of the glories of Capitalism, we're often reminded by pundits, is Creative Destruction, in which industries (such as buggy whip manufacturers) are destroyed in favor of more productive and therefore more profitable industries (such as the auto industry). Similarly, when foreign producers make a product so much cheaper than domestic companies--hey, it's Creative Destruction. The workers in the old industry lose, but the consumer wins. The only way to keep an uncompetitive industry (such as the British auto industry in the 1960s) alive is with subsidies which eventually impoverish the entire nation. So will the U.S. economy--engorged by debt, run by spendthrift wastrels, and slowly slipping toward recession--benefit from some Creative Destruction? Many look at the coming recession with fear, as if the collapse of the debt and derivatives bubbles will launch an avoidably awful time. It will undoubtedly be painful, but perhaps the best analogy is the forest, where all attempts to forestall fires simply guarantee a massive, uncontrolled blaze which burns all the deadwood and underbrush. Once the fire has burned all the deadwood, then a true rejuvenation begins. Until then, the inevitable firestorm's delay only burdens the forest with heavier loads of unhealthy dead underbrush and branches. The instruments and debt of financial speculation are the deadwood which must be burned to ashes before the economy can return to health. I may have misunderstood Olson's concepts in proposing this analogy, but it has a certain logic--the logic of "the business cycle," in which unsupportable debt is blown off and consumers save up capital rather than borrow and spend it. Thank you, Peter, for introducing me (and hopefully you, dear reader) to a key series of insights. Here are two of Olson's best known books (as yet unread by me): Power and Prosperity: Outgrowing Communist and Capitalist Dictatorships The Rise and Decline of Nations: Economic Growth, Stagflation, and Social Rigidities February 7, 2007 Public Employee Pension Greed and the Gutting of Downtowns Readers responded to yesterday's entry on the unsustainable nature of public employee pensions,and guess what: it's even worse than I thought: the greed, the corruption, the political power plays to protect the fat retirements of the few, regardless of the cost to the many. We've got great posts today, so please read them all. Let's start with San Diego, which faces bankruptcy due to its pension obligations: City must take tough action on pension debt: Bankruptcy May Be Answer Between 2004 and 2010, the voracious costs of San Diego's municipal pension fund are expected to almost triple -- from $85 million a year to $242 million. That additional $157 million in taxpayer contributions to city retirees is more than enough to wipe out the entire annual budget of the Fire Department.Next up: a longtime contributor's tale of just how easy it is for public employees to plunder the public: I have a friend who became a firefighter at 20 after taking a few classed at the College of San Mateo. He �works� for a department in the East Bay (I put work in quotes since in his suburban district with �paramedics� the �firefighters� rarely go on a call and he will often go a full month without going on a call).It will make you sick, unless you're one of the "public servants" ripping off the public like this guy: In 2000, the 57-year-old CHP employee was awarded a $39,000 settlement (for his stress claim), medical care for life for his injuries, and a state industrial disability pension of $106,968 a year - half tax-free.Isn't there a nice cold prison cell awaiting anyone pulling this kind of out-and-out thievery "in the real world"? Our U.K. Correspondent (who triggered my initial meditation on the finances of my own city, which thanks to runaway pension costs, are perched on the precipice of doom) contributed this report on the hollowing out of urban shopping districts in his part of the world. Be sure to read how the city is so desperate for revenue that they drive potential shoppers away with absurd parking fees: Great post today - I like the way you extrapolated the scale invariance concept. We have much the same issues in the UK with the public service getting inflation linked, gold plated, cast iron, copper bottomed pensions.Thank you, contributors, for information on a brewing public pension problem (and thus a tax problem) set to explode--apparently all over the developed world. February 6, 2007 Scale Invariance: Is Your Neighborhood Sliding into Recession? Our U.K. correspondent recently sent in a brief description of scale invariance, which is one of the traits of fractals: (emphasis added) The thing about most complex systems is that they are scale invariant so an understanding could also offer insights into smaller systems. For example, in an economy you see the same interactions on the scale of a neighborhood, city, region, country and internationally. The scale of the interactions varies with the size of the system - but the pattern remains the same. Think of a simple line drawing of a coastline. Without some sort of reference, it would be very difficult to tell whether the map was of 1 mile, 10 miles or 100 miles of coastline. Scale invariant.  This got me thinking: how's my neighborhood/city doing financially? Well, let's see:

This got me thinking: how's my neighborhood/city doing financially? Well, let's see:

Poor firefighters; they only get to retire at 50 with a pension equalling 90% of their highest lifetime salary. Meanwhile, the city's pension contributions have risen 384% in a few years: In fiscal year 2005, $15 million of Berkeley�s $115 million general fund will pay for contributions to the California Public Employees System (PERS). Last year, the city spent $8 million on retirement benefits. The year before, the city spent only $2.8 million.This means 13% of the city's general fund is going to pensions, and it's slated to inexorably rise--and that's counting on the existing pension fund being able to generate 8% returns far into the future. What if the pension fund takes a string of 8% losses? Nobody even mentions that as a possibility. Do you see a pattern here? Municipal unions secure gold-plated pensions and medical benefits for life, while the source of all those tax revenues--old-line businesses--are failing left and right. These businesses are irreplaceable; a new ink cartidge refilling outlet (just about the only new retail operation in downtown) does not provide anywhere near the same payroll or sales tax revenues as the large, established retailers who have called it quits. I have long predicted that a showdown between public employee unions and residents (taxpayers) is brewing and will explode once the recession drives down pension fund returns and city tax revenues. The firefighters are already gearing up to protect their fiefdom and their pensions; if they care so much about the fire stations staying open, how about working a few extra hours for no more pay or benefits that they already receive? You won't hear any talk of sacrifice from public unions, though; it's all about the money, and preserving pensions and lifetime benefits which are unmatched in the private sector. Before any irate firefighters reach for the keyboard, let me disclose that my cousin is a cop, my business partner was a cop, and several of my oldest friends are cops--(detectives and up). If you know any cops, you know the drill: the firefighters union sets the pace, and the cops try to catch up. How many cops do you know that have the leisure and energy to run lucrative side businesses? None. How many fire dept. employees have side businesses? Plenty. Nuff said. As for danger on the job: your basic private security guard gets shot on a regular basis, and they get paid about a fourth of a union city employee. Sure, they're not cops, but it's always a good idea to take a look at what the private sector is paying for risking your life. For the record: if any municipal employees deserve 90% pensions, it would be police officers, but only with 30 full years of service, and only starting at age 55. Police work burns out people, because you're dealing with the dregs of humanity, a messed-up judicial system and constant human tragedy, day after day, month after month, year after year. You don't get paid 8 hours for 4 hours' work; you get paid for 8 and work 10 or 12. {RANT ON} My sympathy for criminals, crazies and buyers of hard drugs: zero. Sorry. We pay humongous taxes to lavish money on our public schools, our own city health department, including a good mental health clinic, and an array of social services for the homeless. But if you can't be bothered to make an effort in school despite all the resources available to you, or you refuse the social services we offer and don't take your meds, or you need meth or coke just to get through the day, then exactly why should the rest of us suffer as a result of your self-generated plight? I live in a near-ghetto; come live in my neighborhood for a couple years and see how much sympathy you have left.{/RANT OFF} The firefighters, of course, want the city to slash somewhere else--like social services, or the Library, which has seen its budget gutted by skyrocketing pension costs, too. So the public will see library hours cut and fire stations closed so its city employees can retire at 50 with pensions of $80,000 a year and up, and gold-plated (fully paid) healthcare benefits for the next few decades. And before any irate city employee touches the keyboard, let me also disclose one of our old friends retired from the city at 52--maintenance department. He'd suffered a work injury, but he readily admits he could have worked for years longer on "light duty." As it is, he's been tapping the pension fund longer than he worked for the city. How can any employer, municipal or otherwise, afford to pay retirement cash and benefits for a longer period of time than the employee actually worked? It simply doesn't pencil out, and telling us (citizens and taxpayers) "I deserve it" doesn't alter the unsustainable math. We have another friend who worked part-time for the city in a routine clerk position for about seven years and then quit over personal conflicts at 54 years of age. The next year, he turned 55 and started drawing a modest pension--after 7 years of 25 hours per week work. He's in good health, and there's no reason why he won't collect his pension for 25 or 30 years--a pension "earned" after a mere 7 years of part-time labor--and well-paid labor ($18/hour, about double what a clerk would earn "in the real world," i.e. the private sector). Is this kind of largesse sustainable? Quite obviously not. If the situation is so dire now, what happens in a recession? Tax revenues plummet, pension fund returns plummet, and then the city has to cover the shortfall in investment returns. So how much of city revenues will be going to gold-plated pension plans then? 25%? 35%? No one knows, but there will be a showdown: either the public unions give back some of their ill-gotten pension gains, or the cities will have to raise taxes substantially, or basically eliminate entire departments of heretofore "essential" services. And if established retailers are closing their doors in "prosperous times" (bitter laugh), how many more will close in the upcoming recession? And so where will the cities turn to raise new tax revenue when their independent business sector has been effectively gutted? Property owners, who are watching their home values drop every month? Generally speaking, municipalities don't go bankrupt, so they're locked into paying the pensions regardless of what other services get slashed. The solution will be a public so incensed by their reduced services that the state Legistature will be forced to act. It will be a battle royale, though, for the public unions are the Democratic Party's largest contributors, along with the Trial Lawyers lobbying group. The Legislature will have to act against their largest donors--something they won't do unless their defeat at the polls is certain. That will only happen when the public is so enraged that Party affiliations no longer have much meaning, i.e. Throw the Bums Out! The 2008 Election, when the nation is mired in a recession which only deepens by the day, will be very interesting. February 5, 2007 Really Simple Recession Since the U.S. savings rate has fallen to a 74 year low of minus 1% (matching the low during the Great Depression), it's clear the U.S. consumer continues to spend with unparalleled abandon. To capitalize on our heedless spend-spend-spend era, I'm trying to interest publishers in a new magazine. Here's my first cover design:

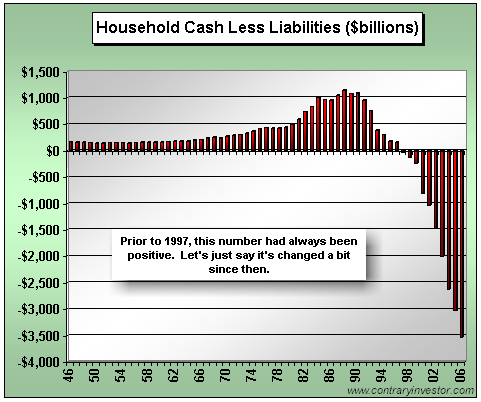

How much longer can U.S. consumers keep borrowing cash against assets and spending the cash? Frequent contributor U. Doran sent in a cogent Consumer Status Report from contaryinvestor.com which suggest the seemingly endless rise of the debt/asset bubble is topping out. This chart from the report says volumes about the sustainability of rampant consumer spending.

But Americans are "so much richer" due to the rise in their homes, stocks and pensions that a little extra debt is no big deal. While that appears true when all assets are rising, now that house prices are declining (and recall that a 0% price change is a 2% decline if inflation is 2%) and the stock market is nearing the final blow-off stage of a 5-year long Bull run, what happens if all asset classes start dropping? "But bonds will rise," the answer comes; maybe, but the vast majority of bonds are held by the top 1% of the populace. Average Joe and Jane don't own any bonds, so a modest rise in bonds (which is by no means guaranteed) does nothing for their sinking asset base. Maybe it helps their pension fund or 401K, but since they can't borrow against those assets, that's still no prop for further consumer borrowing and spending. So what's the future? It's "Really Simple": less borrowing, less spending, and a normal business cycle contraction. Contraction, recession--choose your favorite label, but the results will be the same: spending drops, savings rise, businesses shrink, tax revenues plummet. February 3, 2007 Readers Respond on Nukes, Iran, Healthcare  As you know, there is no anonymous "comments" page here, and as a result the quality

of reader feedback is excellent. It does require me to play editor, but I edit with a very

light hand, posting most comments in full. When you hit a "comments" link with 200 entries,

then you appreciate having an editor who goes through them all and presents the best.

As you know, there is no anonymous "comments" page here, and as a result the quality

of reader feedback is excellent. It does require me to play editor, but I edit with a very

light hand, posting most comments in full. When you hit a "comments" link with 200 entries,

then you appreciate having an editor who goes through them all and presents the best.