|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Writing/Film Dear Aspiring Writers: The Worst Advice You'll Ever Read A Literary Look at I-State Lines Spirited Away: Decay and Renewal An American Poem (Robinson Jeffers) Taoist Chinese Poems The Nelson Touch "It's all about oil, isn't it?" Kurosawa's High and Low A Bountiful Mutiny Howl's Moving Castle Thailand's Iron Ladies Trois Colours: Red The Thin Man: Thoroughly Modern Movies Why My Book Is Better Than the DaVinci Code Iranian Films: The Mirror Piratical Nonsense A Real Pirate Movie: Captain Blood 2005-06 archives 2007 archives Recommended Books American Identity American Identity Literary Contest Winners, 2006 (fiction and essays) Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Your Tattoo in 50 Years The American House and Frank Lloyd Wright Cultural Commentaries On Hatred and Anti-Americanism Anti-Americanism Part 2 Anti-Americanism Part 3 French-Bashing Germany: We All Have Problems, But... Kroika! Chronicles This Blog Sells Out Doom and Gloom Sells The Kroika Mascot-"Auspicious Pet" Wal-Mart and Kroika Kroika and Starsbuck Take a Hit Kroika Ad 1 Kroika Ad 2 Kroika Ad 3 Kroika Ad 4 Kroika Makes Bid for Oreo (April 1) Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Corruption and Avian Flu: China's Dynamic Duo Exporting the Real Estate Bubble to China Is the Bloom Off the China Rose? China Irony: Steel, Marx & Capital Curing The U.S. and China's Dysfunctional Relationship China and U.S. Inflation Trade with China: Making Out Like a Bandit Whither China? Will the Housing Bust Take Down China? China's Dependence on Exports to U.S.; Is China About to Pop? 2005-06 archives 2007 archives Battle for the Soul of America Katrina, Vietnam, Iraq: National Purpose, National Sacrifice Is This a Nation at War? A Nation in Denial Why Is This Such a Tepid Time? That Price Isn't Cheap, It's Subsidized The Most Hated Company in America U.S. Fascists Seek Ban on Cancer Vaccine The Truth About Christmas American Dream or American Nightmare? 2006 Sea Change Obesity and Debt Immigration Ironies U.S. Healthcare: Working Toward a Real Solution A Drug Industry Running Amok Where There Is Ruin 2005-06 archives 2007 archives Financial Meltdown Watch What This Country Needs Is a... Good Recession Are We Entering the Next Age of Turmoil? Why Inflation Appears Low Doubling Down on 5-Card No-See-Um A Rickety Global House of Cards Are Japan and Germany Truly on the Mend? Unprecedented Risk 2 Could One Rogue Trader Bring Down the Market? Worried about Inflation? Stop Measuring It Economy Great? Bah, Humbug Huge Deficits and Huge Profits: Coincidence? Who's The Largest Exporter? Three Snapshots of the U.S. Economy Loaded for Bear Comparing Nasdaq to Depression-Era Dow Who's Buying Treasury Bonds? And Why? Derivatives: Wall Street Fiddles, Rome Smolders Financial Chickens Coming Home to Roost Is the Stock Market on the Same Planet as the Economy? The Housing-Recession-Oil-Healthcare Connection Could We Have Deflation and Inflation At the Same Time? What We Know, What We Can Safely Predict Bankruptcy U.S.A.: Medicare, Greed and Collapse Sucker's Rally A Whiff of Apocalypse Where There Is Ruin II: Social Security 2005-06 archives 2007 archives Planetary Meltdown Watch The Immensity of Global Warming Sun Sets on Skeptics of Global Warming Housing Bubble Watch Charting Unaffordability A Monster of a Housing Bubble A Coup de Grace to the Economy Hidden Costs of the Housing Bubble Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Housing Market Slips Toward Cliff Housing Market Demographics Housing: Catching the Falling Knife Five Stages of the Housing Bubble Derailing the Property Tax Gravy Train Bubbling Property Taxes Have You Checked Your Property Taxes Recently? Housing Bubble: Where's the Bottom? Housing Bubble: Bottom II The Housing - Inflation Connection The Coming Foreclosure Nightmare 1 How Many Foreclosures Will Hit the Market? Housing Wealth Effect Shifts Into Reverse Housing Bubble Bust Will Take Down the Global Economy The New Road to Serfdom: A Negative-Equity Mortgage The Housing-Savings-Recession Connection After the Bubble: How Low Will It Go? After the Bubble: Rents and Housing Values Why Post-Bubble Rents Matter After the Bubble: How Low Will We Go, Part II Housing: 10% Decline May Trigger Financial Ruin How to Buy a $450K Home for $750K Inflation and Housing: Calculating the Bust The Growing Financial Risks of the Housing Bubble Construction Defects: The Flood to Come? Construction Defects Part II Who Gets Hammered in the 2007 Housing Bust Real Estate Bust: The Exhaustion of Debt What Happens When Housing Employment Plummets? One More Hole in the Housing Bubble: Insurance Financial Kryptonite in a "Super-Strength" Housing Market Three Secrets to Unloading Property Today Welcome to Fantasyland: Housing's "Soft Landing" Why Is the Median House Price Still Rising? Why Median Prices Appear to be Rising? The Root Cause of the Housing Bubble Housing Dominoes Fall Twilight for Exurbia? Phase Transitions, Symmetry and Post-Bubble Declines Housing's Stairstep Descent 2005-06 archives 2007 archives Oil/Energy Crises Whither Oil? How much Is a Gallon of Gas Worth? The End of Cheap Oil Natural Gas, Naturally High Arab Oil Money and U.S. Treasuries: Quid Pro Quo? The C.I.A., Oil and the Wisdom of Crowds The Flutter of a Butterfly's Wings? A One-Two Punch to a Glass Jaw Running Out Of Oil vs. Running Out of Cheap Oil 2005-06 archives 2007 archives Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds Geezer Rock Overload Paying for Web Content Light-As-Air Pancake Recipe In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono Happiness for Sale: Jank Coffee Ten Guaranteed Predictions for 2010 Why My Book Is Better Than the DaVinci Code My Brand Management Stinks Design Follies The New Jank Coffee Shop Jank Coffee, Upscale Tropic Style One-Word Titles Complacency Nostalgia Lifespans Praxis Keys to Affordable Housing U.S. Conservation & China Steve Toma, Me & Skil 77s: 30 years of Labor Real Science in the Bolivian Forest Deforestation and Sustainable Forestry The Solar Economy (book) The Problem with Techno-Fixes I Love Technology, I Hate Technology How To Blow off Web Ads and More 2005-06 archives 2007 archives Health, Wealth & Demographics Beauty of the Augmented (Korean) Kind Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Is Obesity an Inflammatory Response? Demographics & National Bankruptcy The Decline of Europe: A Demographic Done Deal? Are the Risks of Obesity Overstated? Healthcare: Unaffordable Everywhere Medication Nation The New Disease We Just Know You've Got Can You Can Tell Which Pill Is Fake? Bankruptcy U.S.A.: Medicare, Greed and Collapse The 10 Secrets to Permanent Weight Loss 2005-06 archives 2007 archives Landscapes Selling the Landscape The Downside of Density Building Heights and Arboral Roots Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Waimea Canyon, Yosemite, Camping & Pancakes Nourishment The French Village Bakery Ideas What Is Happiness? Our Education System: a Factory Metaphor? Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi Splogs, Blogs and "News" "There is no alternative to being yourself" Is There a Cycle to War? Leisure, Time and Valentines Is the Web a Giant Copy Machine? Science Matters Anti-Missile Defense: Boost Phase Vulnerability History The Strolling Bones: Rock of Ages Bad Karma: Election Fraud 1960 Hiroshima: First Use All the Tea in China, All the Ginseng in America Friday Quiz Pet Obesity The Origins of Carbonara Organic Farms Oil and Renewable Energy Human Diseases Wine and Alzheimers Biggest Consumers of Chocolate 2005-06 archives 2007 archives Essential Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So Fewer: How the New Demography of Depopulation Will Shape Our Future The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal The Future of Life Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies The Solar Economy: Renewable Energy for a Sustainable Global Future The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Feeling Good: The New Mood Therapy Revised and Updated Recommended Books More book reviews Archives: weblog February 2007 weblog January 2007 weblog December 2006 weblog November 2006 weblog October 2006 weblog September 2006 weblog August 2006 weblog July 2006 weblog June 2006 weblog May 2006 weblog April 2006 weblog March 2006 weblog February 2006 weblog January 2006 weblog December 2005 weblog November 2005 weblog October 2005 weblog September 2005 weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

|

March 31, 2007 Readers On What Makes a Blogger Engaging Two readers submitted thoughtful commentaries on what makes a blog engaging. First up is Darrell C.: Your latest got me thinking more on what makes a blogger engaging.Fellow writer E.A. addresses authenticity, creativity, and the effects of money on a blog--even donations. In my thank-you to E.A. for donating money to the site, I'd written: "if you have any comments about what you like best about the site, what could be improved, or topics you'd like to see covered, please let me know." His response got me thinking: I think that's just the problem. The donations are already changing your site.This really goes to the heart of several important issues. I've been worrying since starting the donations link about just these issues, and E.A.'s commentary crystallized my hunch that both being prompted for donations and doing the prompting is getting tiresome after 8 days. I think E.A. is right--the sidebar pitch for donations is enough. So unless I come across some amusing bit which lends itself to the donation link, it's in the background (sidebar no one looks at). Since I keep a list of dozens of ideas, links and reader comments which would make interesting posts, I don't think this site's content or perspective has changed. But E.A.'s comments make me realise how subtly money--even in the form of donations--could diminish the very things which have drawn readers to the site. Special note: don't miss our April Fools entry tomorrow. March 30, 2007 Diets, Genes and Health Thank you G.N. ($25), E.A. ($10) and G.S. ($25) for your vote of confidence and kind gifts. I am greatly honored by your support. All contributors are listed at the bottom of the page in acknowledgement of my gratitude. I've received reader feedback on the diversity of human diet, the role of genetics and the common-sense habits of health. I've illustrated the entry with random photos of food I've taken (or made) at home or at friends. First up is new correspondent Michael M. with two fascinating observations on human diet: Here's a diet 'study' for you:

Next, contributor Chuck D.'s commentary on his own experience shows the long-term value of moderation, gradualism, good habits and common sense in exercise and diet: Congratulations! You and Nurse Dorothy have produced the most concise explanation I have seen regarding one of the major problems that contributes to our screwed-up health system in this country. The ideas you two have expressed have been in my mind in disorganized form for quite some time. You have organized them quite nicely for me. Thank you.Contributor K.K. points to the over-arching influence of one's genes in how we fare as we age: We have talked about this before and I think it is unfortunate that we don't talk more about how people are genetically very different. To say anything other than "we are all the same" is politically incorrect and will get you in trouble, but the truth is that we are really different and some people can get away with eating total crap and still look great and be healthy while others can eat nothing but small portions of good food and still look like crap and have health problems.

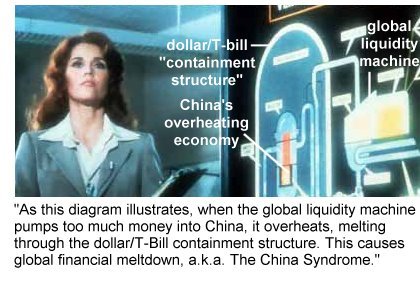

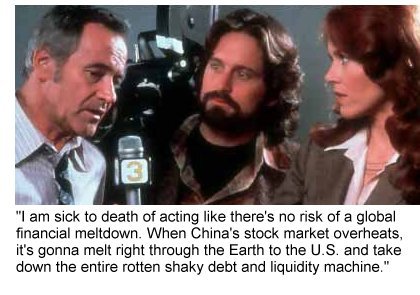

Last up, a story from the Wall Street Journal on how workers "game" plans designed to encourage healthier habits, leaving already-healthy co-workers with no rewards: Wellness Plans Reach Out to the Healthy (3/28/07, subscription required, or find it at your local library) As more employers pay workers to quit smoking, take up exercise or lose weight, a growing number are under pressure to devise ways to reward another group of employees -- those that may already lead a healthy lifestyle.My own suspicion is that disincentives work, too--as in, all visits to the doctor cost you something which you will notice, such as $25-$50, and there is only limited coverage for lifestyle diseases and drugs. (You can be sure that anyone who has to pay $50 for a doctor's visit will not be running down to the clinic when they have the sniffles. I know because my own self-employed coverage requires a $50 co-pay for any visit. With no drug coverage, I am also not exactly pining away for fistfuls of outrageously expensive pharmaceuticals.) I've run out of catchy reasons why you might want to Your readership is greatly appreciated with or without a donation. March 29, 2007 Are Blogs the New Newspapers? Thank you S.F. ($5) for your vote of confidence and kind words. I am greatly honored by your support. All contributors are listed at the bottom of the page in acknowledgement of my gratitude. Are blogs the new newspapers? Reader H.S.K. got me thinking about blogs and media in a new way: Let me say that I have been reading your blog for several months now (as well as a few others). Your site stands out mainly because of the high degree of thought and creativity of content that you provide on a daily basis.Thank you, H.S.K., for the praise and the insightful commentary on the future of media. Here is contributor Paul M.'s assessment of the mass media's weaknesses and the impact of blogs: But I think the overall discourse, given the nature of the Internet and blogging, has this ripple effect that transcends the number of supporters who identify mainly with OfTwoMinds. Quality sites such as yours have a much greater impact than you might realize. So although some of the topics often are presented with highly technical analysis, the issues don't always lend themselves to simple solutions. Think derivatives. Zero discussion in the mainstream media, with the exception of the financial press, which appears to be exuberant cheerleaders one day and somber bears the next. And I am not saying the mainstream is without value. They just don't follow a logical progression sometimes.Astute reader Phil M. comments on what differentiates blogs from the mass media-- the personal touch: (please pardon my reprinting of praise, something I don't do unless there's another point being made by the reader) I forget how I stumbled upon your blog, but I am very grateful that I did. The blog phenomena are fascinating for many reasons, with great content and the allure of an emerging new media type probably chief among them. But what made me hit your PayPal button in an instant (okay, a couple of seconds) was that I've come to regard you as a sort of friend that I like to listen to, that lubricates my own thinking. Usually the loudest or most emphatic guy at the pub gets the most attention, but I wish it was someone more like you: sensible, compassionate, insightful, classy, witty and human.These reader insights made me realize why this site attracts so many of the best and the brightest--it's you. The high quality of the readers' comments insures the quality of the dialog between myself as "editor" and you as reader and contributor is equally high. As HSK put it so well: you have access through other readers to a vast sea of collective knowledge of the highest caliber. It made me ponder the weaknesses inherent in both the mass media and the blogosphere. In the mass media, readers/viewers are shoved aside onto "letters to the editor" unless they're an expert in academia or government who is known as an expert to the media. Anyone without these PR credentials is basically ignored. The only vote readers have is to "vote with their feet," i.e. cancel their subscription. That's a pretty blunt tool for input. As for "pundits," there are only a handful in the entire nation who get paid to pontificate as columnists, and unfortunately they generally are little more than ideological distillers: every topic gets mashed into a "Conservative" or "Progressive" diatribe, and frankly, that's about as entertaining (and useless) as "if it bleeds, it leads" journalism. There's another serious problem with the major media, and many of you have written in to tell me you sense the same thing: the media simply isn't reflecting the realities we see around us. In general, the media coverage suggests everything is rosy with the U.S. economy, even as we see evidence to the contrary "on the ground." Some readers have gone so far as to suggest that they thought they were going crazy, as what they saw did not align at all with what the media "reports." The blogosphere has its own inherent limitations as well. There's the unfortunate tendency towards "cheerleader" sites which attract and reinforce those already possessing the same ideological views. If you "vote" for information which already aligns with your views, then is this truly "democratic"? Are you a better-informed citizen for reading materials which don't challenge your knowledge base or ideological bent? Blogs offer plenty of opportunities for reader input--in fact, too many. Forums for readers to post comments and respond to each other and the host/writer can be interesting, but the problem with these is that they're huge time-sinks. On the rare occasion I read an entire chain of comments, I find myself exhausted by the expense of time and wishing that I could have read something with the same information condensed into a succinct format. None of us has time to read more than a handful of commentaries, so we want them to be succinct and fresh. This is the goal of professional journalism (or should be). Then there's the problems inherent in anonymous blogging, where venomous or just plain idotic comments are posted with the same alacrity as thoughtful ones. As I ponder the positive feedback I've received from so many of you, I am wondering what brings such savvy readers to this site. My guesses: If I am off-base on all this, then by all means let me know. If I am an early adopter, as HSK suggests, then I am indeed fortunate, because I've somehow attracted one of the smartest readership on the web. (insert brilliant marketing line here which instantly causes erudite readers to) Your readership is greatly appreciated with or without a donation. March 28, 2007 The China Syndrome--Financial Meltdown Thank you J.H. ($20) and P.&T. S. ($12, sent via mail) for your generous and quite unexpected donations. I am greatly honored by your support. All contributors are listed at the bottom of the page in acknowledgement of my gratitude.  The 1979 film

The China Syndrome

The 1979 film

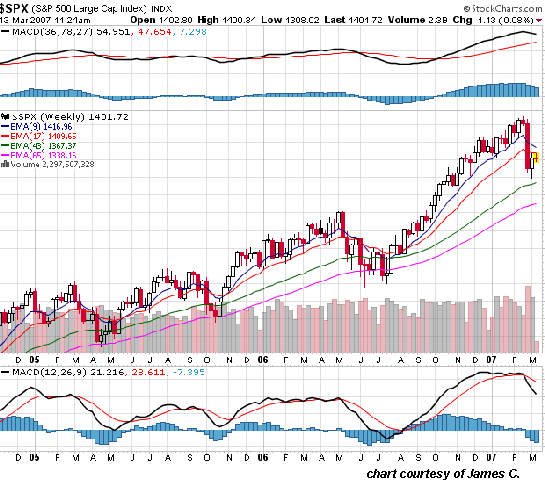

The China Syndrome(wikipedia entry on The China Syndrome) Nowadays, the idea that a consumer-spending meltdown in the U.S. could trigger a subsequent slowdown in China's red-hot economy is a given. But perhaps "The China Syndrome" works both ways, and a meltdown of China's speculative financial bubble will trigger a meltdown in the U.S.'s debt-driven speculative bubbles. To give you a taste of just how frenzied the Chinese stock market has become, consider this Bloomberg story sent in by frequent contributor U. Doran:

March 21 � Bloomberg (Luo Jun / Simon Pritchard):This chart illustrates the stupendous (and recent) rise of the Chinese stock market. It also poses three questions. 1. Is this sustainable? 2. How soon will it drop? 3. What effect will a sharp decline have on global financial markets? Question Three is easy to answer, for the late February swoon in the Chinese markets immediately sent global markets tumbling.

As for Question One, here's an article submitted by frequent contributor Albert T.: Hong Kong's stock market romance turns sour: "We like to buy shares, but when the nanny starts to give out investment tips, you know things have got a bit irrational," said Allan Chan, who like many Hong Kong residents likes to dabble in the market.Oh really? This statement is a laughably absurd denial of reality, for February's drop amply proved that China's markets can and will influence global markets. The reason is not the size of the Shanghai market or any technical reason; it's simply that the entire world knows that China has been the engine of global growth, sucking up vast quantities of raw materials, machine tools, consumer goods and capital. It has also been (along with Japan and the OPEC countries) the primary supporters of debt-loving American consumers' 6-year buying spree via the purchase of hundreds of billions of dollars of U.S. Treasury bonds, which has kept U.S. interest rates low and kept the dollar from plummeting even lower than it already has. If the party stops in China, it stops everywhere. All the strident babble in the media and in Congress about the dollar-yuan exchange rates fails to consider how deeply intertwined the U.S. and Chinese economies have become. It is nonsensical to think that an adjustment in the exchange rate is going to change much of anything; that would be the equivalent of moving a pawn one square forward on a 3-D chess board. While American politicos have focused on the trade imbalance to score easy points with confused constituents, they seem to have forgotten that the Chinese central bank owns at least $600 billion in U.S. Treasuries as well as other U.S. debt--including residential mortgage-backed securities: China's money woe: Where to park it all:

Most central banks have invested them in U.S. securities, mostly Treasury bonds, but sometimes mortgage-backed securities as well. In recent years, these giant purchases have helped hold down interest rates that American home buyers pay for mortgages and the U.S. government pays to finance its budget deficits.Albert T. also sent over this link to a story on China's slowing economy: Pace of Chinese growth 'to slow' The pieces are in place for a meltdown of China's speculative market. A speculative bubble in which people are betting credit card debt on a market which has jumped 200% in less than two years is clearly vulnerable to reversal. Underneath the speculative bubble, the real economy is slowing as officials seek to restrain risky lending and inflation. For an in-depth analysis of Chinese policy-makers' moves to control the runaway stock market, see The Shanghai Bubble by Gary Dorsch, courtesy of correspondent U. Doran. As China has expanded its U.S. debt holdings to include mortgage-backed securities, it has unwittingly exposed those holdings to the meltdown currently underway in the U.S. housing and mortgage-backed securities markets. Its vast horde of U.S. dollar-denominated Treasuries further exposes it to a decline in the dollar. And the entire $1.3 trillion portfolio is managed by woefully underpaid civil servants. On the U.S. side, our speculative markets are vulnerable to the slightest tremors in the Chinese markets, and to any re-shuffling of their dollar and Treasury holdings. It may come down to whose speculative financial "reactor" melts down first. The idea that one country's debts and bubbles can melt down without effecting the other is wishful thinking.

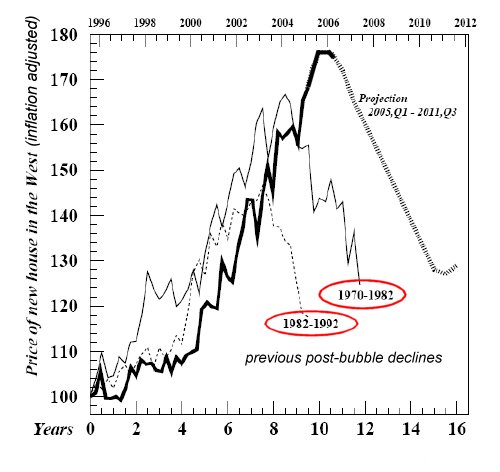

As for question Two, How soon will the Chinese market drop? Consider this chart of an eerily similar bubble--the NASDAQ circa the dot-com era. If this had any value to you. . . Your readership is greatly appreciated with or without a donation. March 27, 2007 An Ounce of Prevention Is Worth...? I'd like to thank K.K. ($20), C.S. ($15), T.T. ($10), R.SJ. ($10), A.I. ($15), I.D. ($5) and J.M. ($20) for their unexpected and generous donations. I remain deeply honored by the support being offered by readers. All contributors are listed at the bottom of the page in acknowledgement of my gratitude. Knowledgeable correspondent Nurse Dorothy had this thought-provoking response to a recent entry on managed care in the U.S.: This is in response to the March 14th blog about managed care. In particular I would like to address the issue of preventive care. It is not really our lifestyle that needs to change but our culture. Culture is what drives lifestyle. As an example, being a nurse I meet many people from all walks of life, rich to poor. Whether poor or rich, both sides tend to work long hours, have high stress, lack exercise, and eat poorly all of which leads to chronic disease. Why, because whatever extra money Americans make is spent on stuff.Dorothy gives voice to something I felt but could not express as well as she has here: that the obsession with who's going to pay for the skyrocketing costs of marginally effective drugs, operations and care is sidestepping the real issue, which is becoming healthier as a nation. What we should be obsessed with is the prevention of every disease which is preventable via lifestyle changes and diet-- i.e. a significant percentage of the disease we suffer. The revolution would have to be of values, specifically, personal responsibility. It would no longer be the role or responsibility of society or medicine to "fix" the damage which we inflict on ourselves. We live with a curious paradox of values: if you drink yourself silly and smash your car into someone, you will be arrested and charged with a crime. No one steps up to pay for your "cure" or for your attorney. Those are your responsibilities. But if you smoke and get lung cancer, or drink excessively and destroy your liver, or eat to excess and end up carrying 187 pounds on a 5-foot, 5-inch frame and are prediabetic at 21 years of age, then "somebody" is supposed to "fix" you, and pay for it, too. Does anyone else notice the disconnect here? Just because we can be struck down with diseases over which we have no control, such as brain cancer or mental illness, then we're off the hook entirely for all the diseases we can influence or control? It doesn't make sense. Human beings respond to incentives and disincentives. If you know someone will magically save you from the consequences of your actions, you respond differently than if you will suffer the consequences, and you will respond in yet another way when the consequences start hitting home. This story by a 21-year old prediabetic is a real eye-opener: Sugar isn't sweet for her anymore; She's one of 54 million with prediabetes. When connected to the trend of obesity, these plague-level stats are enough to make news headlines regularly. It's hard to ignore a figure like 74 million, the total number of Americans with prediabetes, Type 1, and Type 2 diabetes.There is another way of living, of course, a healthier way, and it appears to be centered around exercise. While we obsess over diet, the active, alert 90-year old I know ate a standard mid-century European diet of white bread and sausage. What differentiates him from millions of others is not some astonishingly complicated "healthy" diet and dozens of obscure supplements but his daily routine of long, vigorous walks. Here's an article which substantiates this view: You Can Stop 'Normal' Aging; New research reveals surprising facts about our changing bodies. So where do we stand on personal responsibility and health? The young writer with prediabetes mourns the loss of her "carefree" self who could binge on junk food and guzzle six cans of soda a day; when did self-destruction become confused with freedom? When did visibly unhealthy excess become "normal"? Did you really feel great after the 5th or 6th can of sugar-water? Somehow I doubt it. Perhaps what the writer mourns is her loss of the current hallmark of being American: the ability to indulge in excess without consequences. I can't be the only one who sees a direct link between "judgment-free" debt binging and "judgment-free" food binging, for the idea is the same: I should be able to get everything I want and eat everything I want now, without future consequences, without discipline, without limits and without judgment, i.e. being challenged. Our health constantly challenges us all. None of us are immune from temptations and the various conditions we are dealt by genes and our environment, and I certainly don't want to minimize the difficulties in staying healthy and fit. I had to lose 10 pounds last year and need to shed a few more because I have borderline high blood pressure (which I've lowered via lifestyle changes, as described here before). I won't bore you with a roster of my aches, pains, chronic conditions, etc. because that's just normal life. We all have to manage our physical and mental well-being, and adopt routines which get us where we want to go rather than create roadblocks and more problems. It's like all the other disciplines required by life. If it was easy we'd all look like models, just as we'd all be millionaires if making money in the stock market was easy. It is a stunning indictment of our culture that fully 25% of our entire population of 300 million people is at risk of what is largely a preventable lifestyle illness. Throw in heart disease (ditto), smoking (ditto), abd various other addictions and the total easily exceeds 50% of the population. And we wonder why medical costs are skyrocketing? It is difficult not to conclude that the loss of wealth and health we face is an unfortunate but apparently necessary step we must collectively get through to restore some semblance of common-sense values to our culture. Oh, and there's one more tiny little problem. We are rapidly approaching the end of the line in our ability to pay for the nation's bloated, inefficient and mal-adapted medical care. When the money runs out--that is, when the Chinese central bank and the Saudis stop loaning our government hundreds of billions of "free money" via buying Treasury bonds, then we'll rediscover the one great truth of prevention--it's so very much cheaper than any cure. If the site hasn't annoyed you too terribly yet. . . Your readership is greatly appreciated with or without a donation. March 26, 2007 The Subprime Mess: A Personal Account First let me thank P.W. ($5), C.M. ($30), S.V. ($10), S.H. ($30), J.D. ($5), K.C. ($12), R.H. ($20) and T.R. ($5) for their generous donations. I've listed all contributors at the bottom of the page to reflect my ongoing gratitude. I received the following personal account from J.M. about the demise of their subprime mortgage and impending loss of their home. We all know this is an increasingly common story. I have illustrated this account with an actual mortgage ad I scanned last year--the key phrase in the ad is "It's almost impossible not to qualify!"--and a graph of the probable shape of the housing bubble decline. I suspect this chart might be generous, as my own past analyses suggest a full retrace to 1996 prices is entirely possible. (Please see the "Housing Bubble Watch" entries in 2005-6 archives).

Here is J.M.'s unfortunate story: I happened to catch the Senate Banking hearing last night on C-SPAN and I am writing as one of the unfortunate homeowners caught in this Subprime nightmare. I thought I heard mention of assistance being offered to help homeowners stay in their homes and I am seeking some assistance if there is any assistance being offered. I am days, possibly weeks (if I am lucky) away from eviction from my home which I have owned for less than 2 years. I have filed for bankruptcy protection and my life is in shambles; no money, credit trashed, savings gone, low paying job . . . a mess.  Before I begin my own response, I'd like to reprint another reader's suggestion for

a topic, which can be expressed as one of personal responsibility:

Before I begin my own response, I'd like to reprint another reader's suggestion for

a topic, which can be expressed as one of personal responsibility:

Got a topic suggestion for you. Why do we now reward the losers as a society? Didn�t buy insurance? That�s ok, gov will make it up. Made a poor financial decision? That�s ok, gov will make it up. Spent 10 years on college loans to get a degree in anthropology and wonder how you are going to pay that back? Don�t worry, gov will make it up. Meanwhile, those of us who make smart decisions, save our money, live cheap, etc. continue to pay more and more in taxes to make up for the people who made poor decisions. And of course, the poor decision people never have to face the consequences.My response to J.M. was more or less as follows. Buck up--many of us have been wiped out financially and we recovered by keeping our expenses lower than our income and saving money for a few years. I too am 53, and am paying down debt and accumulating savings/assets in order to buy real estate at bargain prices in the 2011-2014 timeframe. My income is low (though I'd be delighted for it to rise) and I pay horrendous self-employment taxes, humongous health insurance premiums and astonishingly high property taxes, even though we bought this property 15 years ago. The self-employed among you are very likely nodding your head saying, "Me too!" The list of "entitlements" forgone to be self-employed is long, but to those of us who choose this path the trade-off is worth it. So, no complaints. But next time you want to complain about taxes, try paying 13% of your net right off the top for Social Security. Then pay the Fed and State taxes, the property taxes, the local taxes, and see how much is left. Amen, Brothers and Sisters, it isn't much. Many hardworking people were wiped out in the Great Depression, as were many wealthy people. Both types survived and eventually prospered. I knew guys who'd lost it all in the 1959-61 downturn. Many people were wiped out in the 1981-83 recession (me being one of them). Others were wiped out by the dot-com bubble bursting in 2002-2001. I know many stories of honest, hardworking people sinking their entire 401K retirement nestegg into the NASDAQ right near the top, and having their savings from decades of labor wiped out. In other words, getting wiped out financially is part and parcel of capitalism. This may sound brutal to those of you with a certain ideological bent, but business and investing is and will always be Darwinian. I also suggested that a bailout wouldn't work because the discrepancy between J.M.'s income and expenses was simply too great. Over the course of just a few years, the discrepancy would total tens of thousands of dollars. This is what is called "Putting good money after bad." In other words, when you make a poor financial investment, you just have to exit the position, and learn from your mistake. I think it's also important to be honest that buying a house in those circumstances was a form of speculation--speculation that income would quickly rise to meet expenses, and that the house would rise in value fast enough to pay the mortgage with equity extraction. Like many speculations, this was a long shot, and it didn't come in. As someone who's been burned with margin (borrowing against stocks in one's portfolio) and the inevitable margin calls, I know the appeal of speculative fevers "when everybody is else is making money effortlessly." (Note: I don't use margin anymore, though judging by statistics that total margin debt now exceeds its peak in 2000, not everyone agrees that it's risky.) I also told J.M. that I may not be the best person to ask, because compared to the loss of one's health or mental health, then financial losses just don't seem that bad--and I speak from experience in all three categories, as no doubt do many of you. I'm also very upbeat about being 53, and don't think being 60 is that old. So working 7 years and saving money and clearing a bankruptcy doesn't seem too onerous to me. I like working and have no expectation of retiring, and no desire to retire per se. Even retiring at 75 would be OK with me, and that's 22 years away. A lot can happen--and be saved--in 22 years. So in all sincerity, J.M., as someone who's on occasion been down to less than $100 to my name, who's lost all his money and been left in debt on two occasions, I reckon the lesson learned is worth the loss, and you can bounce back in short order if you simply keep expenses lower than income--whatever that may be. I have a sneaking suspicion that many readers of this site have experienced financial travails in the past, and overcome them with hard work, some ingenuity and a bit of creative scrimping and saving. I know this because financially successful people contribute gardening and other tips to save money and eat healthier on a regular basis (see entries on March 21 and 24 below) not because they have to but because it's what they value. And though it may sound sappy to those who've never been wiped out, I personally found periods of loss to be great learning experiences. And I don't mean some brief period of modest poverty in youth, I mean losing hundreds of thousands and selling off my house to make good on debts incurred by my business--serious hurt and serious money. But I paid off my debts--a close thing, until we got a contract which allowed us to make a few bucks--and exited stage left with the moral satisfaction that no one ever lost money in trusting us or doing business with us. Since one of my many jobs was property manager, I also reassured J.M. that with some positive personal references, she'd be able to find a small landlord with dogs (or who likes dogs) who would rent to her, regardless of bankruptcy. Landlords just want a responsible, quiet tenant, and if you can show some evidence that you're that person, you'll always find a landlord willing to rent to you--in my experience. As for the institutions which failed to rein in this rampant excess of lending, and the companies which profited from selling subprime and Alt-A loans--of course there will be no redress. The menagerie has left the barn, and closing the barn door now--to the accompanying moral indignation of politicos who stood by doing nothing back in 1996-2002, when they could have made a difference--will accomplish next to nothing. In other words, politics as usual. I am a poor dumb writer who continues to learn from losses, financial and otherwise. Would I trade the wisdom gained for the riches lost? No, for without wisdom the riches will always be lost sooner or later. So what happens to those who will lose their houses? I suggest, with all due respect for the pain of financial losses, that they will declare bankruptcy, learn a lot from their mistakes, and move on to better decision-making in the future. (Granted, bankruptcy is now far more costly and onerous thanks to the reforms shoved through by the banking industry.) I don't think there is any other way to go about rebuilding one's prospects, and I say this as someone who has lived through both the loss and the rebuilding. But if you're down on your luck, then by all means, keep your money to eat and enjoy the site for free. You're sure to find something of interest in our 2007 archives. Your readership is greatly appreciated with or without a donation. Bonus joke of the day: A homeowner seeking a fixed-rate mortgage was about to enter the banker's office when the banker's assistant took the homeowner aside. "Mr. Graves has a glass eye, and I advise you not to stare at it." The homeowner shifted nervously, asking, "How can I tell which is the glass eye?" The assistant whispered, "It's the one with the glimmer of warmth in it." March 24, 2007 Saturday Pot Pourri: Ads, Donations and Gardening Now that I've accepted donations--thank you, A.B. ($15), P.H. ($50), M.A. ($20), S.K. ($25), P.M. ($12), C.G. ($15), P.G. ($15). P.V. ($25) and A.C. ($20) for your gracious support--I've also been thinking about advertising and free markets.  Advertising and marketing are so ubiquitous that we seem blinded to their pernicious

effects on our quality of life. It used to be there were ads in supermarket windows;

now there are ads on the shopping carts, on the floors, and even on the small plastic

dividers used between customers' groceries at the checkout.

Advertising and marketing are so ubiquitous that we seem blinded to their pernicious

effects on our quality of life. It used to be there were ads in supermarket windows;

now there are ads on the shopping carts, on the floors, and even on the small plastic

dividers used between customers' groceries at the checkout.

Websites and blogs have followed commercial television in the strategy of interweaving "content" with distracting ads. The "user" or viewer has supposedly agreed to this trade-off: we get the content for free in exchange for sitting through (or being bombarded with) ads. In the alternative "pay per view," you buy content such as The Wall Street Journal--and you still get bombarded with ads. Hmmm. The general view is that web surfers just ignore the ads, so "everybody wins"--the advertisers get their service/product in front of millions of eyeballs, the blogger gets a few bucks for splashing ads all over their page, and the viewer gets content for "free." My view is: everybody loses. The advertiser's ads are ignored, the blog is cluttered with ads which distract from the content and the "customer" / user / visitor gets another dose of marketing, whether they like it or not. (Yes, there are programming tricks which delete the ads; I've described some here before.) There is a cost to cluttering our lives with advertising and marketing--it just doesn't carry a price tag in dollars. In a truly "free market," wouldn't we all have the opportunity to pay for ad-free content? Yet we don't. Even content we pay for is smothered in ads.

The Third Way is the PBS model, in which ads are clustered between programs and customers/users are cajoled/badgered into donating to the station twice a year. While I understand the necessity of "pledge drives" in this model, I also truly loathe them. In lieu of the programming I like--NOVA, etc.--I am subjected to aging pop rockers or some "financial expert" or "diet guru" extolling some terribly obvious common-sense for hours on end. Yikes! Here's another take on the "free market" in websites and blogs. I am free to post content which I reckon has value, and if no readers find any value in the content, then I have no regular readers. That's about as free as you can get. If I sell ads, then you the reader have no choice (without using some programming tricks) but to have your reading--the reason you visit the site in the first place--cluttered by ads you did not choose to view. Even if you ignore the ads, in placing ads I have removed a key freedom from you, the customer/reader: the freedom to choose ad-free content. But any original content takes time and money to create and host. We all know this, so there is an unspoken contract which you are free to honor or not: in exchange for the content, the customer/visitor offers something in exchange. You visit or not, based on your assessment of the value of the content. If the value is high enough to spark your goodwill, then you choose to honor the content with a donation, the size being entirely up to you. If you can't afford to donate or choose not to, the site remains free to you and everyone else with an Internet connection. This model puts the onus on the "business," i.e. the site/blog creator, to not only provide content which visitors will find valuable enough to spark their desire to honor the value of the content, but to ask the visitors to do so. It's the model used for shareware software, and it relies on this unspoken contract that enough users/customers will decide of their own free will to honor the content with money that the programmer/creator can survive to create more content/software. Whether this model is sustainable remains an open question. Believe me, the easiest thing for a content provider (what a clunky phrase!) /creator to do is put some ads up. You don't need your customers/visitors' approval, and you're saved from the indignities of asking for visitors to honor your content with hard, cold cash, even if it's one dollar. But I've decided I like the direct honesty of this approach. I can't see charging for "premium content" or a "for paying customers only" model, though I understand the appeal to creators seeking a steady income. Why? Because then I might hesitate to post some worthless absurdity like a 1,000-foot bamboo tower being built by an imaginary Chinese cookie company, or a review of a 40-year old film or a goofy ad spoof. And I need the freedom to create the variety of content which interests me--and hopefully, you. In conclusion: that's why this site will remain ad-free, and why I will humbly continue posting this "tip the poor dumb writer" link, should any of you choose to honor the content with a donation. For some of you, $5 is a lot of money; for all of you, $12 or $20 (or Lordy-Lord, $50) means foregoing something else of value which you could have bought for yourself. Knowing this, I am both humbled and honored. For those not moved to send in a donation, that's okay, too, because it's a free market here: you don't have to visit, and I don't have to create content. If I don't originate any content, I miss out on the joys of that process; and if you don't donate, you miss out on the satisfaction of participating and on the gratitude of the recipient. In other words: the world is a tiny bit better place because this is an ad-free zone, and because readers/contributors are an integral part of its success as a forum for ideas: as contributors of topic ideas, comments and questions, and also as contributors of their hard-earned money. On to another gardening book recommendation, this one by knowledgeable reader Brian H: Regarding gardening and self-sufficiency: All it takes is time.Thank you, Brian, for the recommendation. As for myself: I better get some seeds in the ground before the weeds get started. Hi, I'm Charles, and I'll be one of your servers of content today. . . Your readership is greatly appreciated with or without a donation. March 23, 2007 My Sincere Gratitude, and a Look at Gold When I posted a Paypal donation link yesterday, I reckoned one or two generous souls might send in a buck or two as a gesture of support. But holy moly, over a dozen of you surprised the heck out of me by sending in serious donations. I am humbled by your generous and unstinting support of this modest site. To maintain privacy I am listing only the initials of my kind benefactors. Many have also contributed essays and information to the site, for which I am doubly grateful: A.S. $20 W.H. $30 P.M. $12 D.E. $5 C.A. $24 V.P. $12 C.M. $10 L.N. $12 B.M. $50 R.T. $20 R.D. $12 K.M. $20 S.T. $12 K.G. $15 D.P. $12 R.S. $12 J.A. $15 D.S. $20 Thank you, spontaneously supportive benefactors. It's wonderful to have readers, and even more wonderful to have correspondents and benefactors. According to my weblogs, this site is visited about 50,000 times a month (and rising), and on occasion I receive so much email I can't respond promptly. I have learned so much from you, esteemed readers--and I say this most sincerely. As a footnote, I also take your financial support as a vote of confidence in the mix of eclectic subjects covered here, and in an ad-free environment. My wife says nobody looks at web ads anyway, but I find them a distraction and always breathe a sigh of relief when I happen upon an ad-free site. This is and will remain an ad-free site (except for my own spoofs, of course). And now on to today's subject: gold. Glittering, beguiling, an ancient store of wealth--and a remarkably consistent store of value since late 2000:

Just at first glance, we notice that gold remains in a strengthening uptrend. We also note that it tends to stay in a channel or wedge formation for a year or so before breaking out to a new high. We have to be careful here, of course, for wedges can break to the downside, too. One of my old friends asked me last year: are you a gold bug? I answered no. Meaning, I am not particularly wedded to the notion that gold is the only investment to have, or the best hedge against inflation or deflation, or any other "story." But anyone looking at the 10-year chart has to ask: what changed in the financial world in late 2000 which caused gold to enter a multi-year uptrend? I don't have an answer, but I suspect it was a sense of unease with global imbalances in trade, debt, monentary expansion, energy and the election of an aggressively neo-conservative President backed by both houses of Congress. Now let's look at a one-year chart:

What we see is a compression of the 50-day and 200-day moving averages and an uptrend in the MACD. Now conceivably the HUI could break the wedge to the downside and drop back to support at 280--or it could finally vault through the triple-tested resistance at 363. We would be remiss not to note--but not over-stress--last year's seasonal strength in the April-May period, which lies just ahead. As usual, this is not investment advice; do not base your decisions on what others say, make up your own mind up based on all available evidence and your own financial situation, etc. etc. etc. These are charts, dang it, not advice. There is a difference. Charts can be interpreted various ways, and these are offered in the spirit of a beginner's observations. Your donation, however small, is an honor, a recognition of value and a vote of appreciation. Thank you to everyone who has sent their hard-earned dough as a tip. Your readership is greatly valued with or without a donation. March 22, 2007 Sub-Prime Meltdown and the Derivatives Fiasco To Come  This is a tall order, but I'm going to try to explain how the sub-prime meltdown will

trigger a fiasco in the $360 trillion global derivatives market--with unknown consequences.

This is a tall order, but I'm going to try to explain how the sub-prime meltdown will

trigger a fiasco in the $360 trillion global derivatives market--with unknown consequences.

You experts out there may find some fault in my simplifications, and I do not claim to be anything but an interested amateur. But since the coming derivatives fiasco will affect us all one way or another (your 401K blowing up, your pension fund blowing up, etc.), then it behooves us to try to understand a purposefully obscure and arcane subject. For a window into the making and marketing of derivatives, please read the book Fiasco: The Inside Story of a Wall Street Trader For a description of the mortgage derivatives market, I recommend Barrons Just How Sub Is Subprime? (a good explanation of mortgage derivatives). Here's how it works. Let's say you're an "investment" banker type (little inside joke there--"investment," hahahahaha, because your real job is palming off risky speculative bets as if they were low risk "investment-grade" securities) and you've been offered some real garbage sub-prime mortgages--the real toxic stuff that everybody knows will go into default sooner or later. Hmm, this presents a problem, doesn't it? Who will be dumb enough to buy a loan which is destined to blow up and vaporize a big chunk of assets? How about a big dumb insurance company, state pension fund or non-U.S. yield-chasing behemoth in Japan, China or Europe? OK, so now that we have the mark (grifter-speak for sucker) in our sights, we need some serious lipstick to dress up the pig. Here's why we make millions, folks--because we're so danged smart! First, we get some AAA-rated mortgages--the gold standard stuff, 30-year fixed-rate from low-risk borrowers--and then we mix in some toxic sub-prime garbage into a "trust" which collects the principle payments into one income stream (called a tranch) and the interest payments in another. Now we get a credit rating outfit like Moodys to give the trust a AAA rating because hey, the majority of the mortgages packaged into the trust are AAA. (Another ploy is to get the principle rated AAA and leave the interest--which everyone knows will never be collected in full--unrated.) This is important because the marks--the pension funds, insurance companies, and bond funds-- can only buy AAA paper--at least on the books which are shown to investors.  Congratulations--we've created a residential mortgage-backed security (RMBS). Now the

real fun begins. Next, we create a CDO, a collateralized debt obligation, which buys

up whatever sub-prime, Alt-A or otherwise risky garbage mortgages we weren't able to palm

off in the RMBS. CDOs are credit based, of course, as are some spin-off derivatives called

Synthetic CDOs, which are synthetic because they have nothing to do at all with the

underlying debt (i.e. mortgages). Now we sell the CDOs to the marks because the yield is a point or two

(1% or 2%) higher than low-risk paper. And the marks are happy to buy. Why?

Congratulations--we've created a residential mortgage-backed security (RMBS). Now the

real fun begins. Next, we create a CDO, a collateralized debt obligation, which buys

up whatever sub-prime, Alt-A or otherwise risky garbage mortgages we weren't able to palm

off in the RMBS. CDOs are credit based, of course, as are some spin-off derivatives called

Synthetic CDOs, which are synthetic because they have nothing to do at all with the

underlying debt (i.e. mortgages). Now we sell the CDOs to the marks because the yield is a point or two

(1% or 2%) higher than low-risk paper. And the marks are happy to buy. Why?

Let's say you're the fund manager at a municipal or other public pension fund, either in the U.S. or elsewhere. All of you have the same problem globally--low yields on safe investments like U.S. T-Bills and other high-rated bonds. Most of your assets are in Treasuries and TIPS and low-yield corporate bonds--stuff paying 4%. Now you can buy something with a 6% yield, effectively raising the yield of your portfolio by 50%. Hey, you're now a superstar. Your managers love you--look at these returns! Wow, if we can keep this up, maybe our underfunded assets will actually keep ahead of our pay-outs. Our political bosses will love that because they can then divert tax dollars from the pension fund to their pet pork projects. Everybody wins. At least for a while. But we're not done making money off all the toxic garbage mortgages we packaged and sold. Now we sell you, our favorite marks, some derivatives to protect you from the risk we just sold you. Like a nice credit default swap: for a fat premium, you're protected against a default in the RMBS we just sold you. Buying some "insurance" against defaults looks smart, and we pocket a fat fee. But wait-- there's more. Since you can own derivatives "off balance sheet"--hey, everyone does--then we also sell you some interest rate contract derivatives, because hey, what happens if interest rates rise? Then the book value of all those mortgages we sold you goes down. Did we mention that if interest rates drop your derivative melts to zero? I'm pretty sure we disclosed that to you in that 128-page document you signed. Our lawyers say it's in there somewhere, and do you really want to take on a huge Wall Street firm over a lousy $10 million loss? Suck it up, pal, you knew what you were doing--didn't you? Because you did notice that you were making a complicated bet that the yen would drop along with the dollar, and that the euro would rise, didn't you? And we did explain how you earned 6% instead of 4%, right? A little thing called leverage. Well, on the downside, now that those sub-prime mortgages blew up, taking some Alt-A and supposedly AAA-rated FHA and VA loans with them, well, your $100 million CDO is worth exactly $30 million. Sorry about that. Will it ever go back to being worth $100 million? Hahahaha. Now you can paper over the gigantic loss for awhile--after all, these assets are not traded on any exchange, so who even knows what they're really worth?--by keeping the book value at $100 million. And the derivative losses are "off-balance sheet" so it will take a full audit to find them, and you can quit and take another job before that happens. And that, folks, is how billions are being lost and the losses are being papered over even as I type. But the real losses will come out in the wash, and the scale of the losses will be staggering. For more on the sub-prime mess, check out this Wall Street Journal piece (subscription required): Subprime Mortgage Woes Are Likely to Spread. And for a spirited defense of just how wonderful and secure derivatives are making the financial world, read this article recommended by contributor Cheryl A.: Why the Economy Needs Vastly More Derivatives, Not Less. Was this explanation worth $1 to you? What, you think it's chopped liver? Much to your dismay, no doubt, a kindly reader who took pity on my impecunious stupidity suggested I accept donations via Paypal. I am suggesting $12 a year for the reasons listed in the right sidebar. Now if 100 of my most loyal and amused readers were generous enough to slip a $12 tip into the pot here, then I'd had the annual income of. . . a poor dirt farmer in central China! And that would be tremendously exciting. So be a part of the excitement and click on this link to donate $1 or $12 or whatever spare change is rattling around in your checking account. Or keep reading the extra-special valuable information here for free. Your readership is greatly appreciated with or without a donation. March 21, 2007 How Does Your Garden Grow? Responding to the theme of self-reliance, several readers offered gardening-related contributions. To illustrate the topic, I offer a photo of newly budding cherry trees in Brentwood, Calif., a prime orchard area which is rapidly being paved over with stucco McMansions. First up is long-time correspondent Victoria S. on what it takes to reclaim depleted soil--and a culture depleted by a "buy and flip" speculative fever: There may be many housing developments where the soil is SO barren (or even toxic to plants) that it is not worth the effort to attempt a garden. I grow some plants in containers and buckets, but I've learnt from experience at this location that getting a new type of plant from the garden shops and putting it in the ground generally fails. The limited amount of sunlight is a factor, but...

Contributor Cheryl A. offers a description of gardening suitable for an urban setting: After seeing the 0.8% increase in food prices last month, I thought I would pass along the following - I didn't know if you pass this type of information to your readers. Some background first: We both have "black" thumbs, and tried for years to grow things. We even managed to kill a cactus. We couldn't grow corn when we lived in Iowa, even after spending enough money to feed a family of four for a year. Then last year we stumbled upon the Earthbox..a miracle. We placed it on the deck of our townhouse and by the end of the summer we had over thirty pounds of tomatoes. My husband was more excited than when he received his medical degree.And for a general-purpose book on gardening, Our U.K. Correspondent provides a recommendation: If any of your readers would like to get up to speed on gardening and increase their self-reliance I can recommend the bookThank you, readers, for a variety of excellent resources/stories on growing food. There is a primal satisfaction in growing and harvesting even modest amounts of one's own food, and I've recently spent quite a few hours working on our own small patch of dirt. The travails of our peach tree--badly damaged by leaf curl last year--will await a future entry. March 20, 2007 The Financialization of Oil BusinessWeek ran a short but critically important interview back in January which I excerpt below on the Financialization of Energy Markets. What this means is a stupendous proliferation of trading financial instruments (derivatives and futures) which are based on the actual commodities (oil and natural gas). There has long been a futures market for oil, but now that the large investment banks and hedge funds have "financialized" the market, there are trillions in derivatives being written which carry vast amounts of risk. As Mr. Fusaro explains below, this financialization is just in the first inning. The current energy derivative market which he pegs at $3 trillion could expand up to an $80 trillion market--20 times the market for physical oil and gas. One energy-trading hedge fund blew up a few months ago, losing $6 billion in a matter of days. This kind of speculative trading is now heavily influencing the price movements of oil. To illustrate this, I've marked up a chart of a major energy ETF (XLE). Note that there have only been two crises which had the potential to affect markets: the Iraq War starting in early 2003 and Hurricanes Katrina and Rita in late 2005. The rest of the time, there was a background noise of "geopolitical tensions." Note how oil moved up with modest volatility until 2005, at which point wild swings in price became the norm. Yet other than the hurricanes--which affected perhaps 2% of global oil production--there were no events in the physical world to explain or trigger such wide swings in price.

Here are some excerpts from the interview: A Fast New Financial Game Called Energy: Energy consultant Peter C. Fusaro, chairman of New York-based Global Change Associates Inc. and co-founder of the Energy Hedge Fund Center, was among the first to notice the growing role of hedge funds and other financial players in the energy sector two years ago. He talked to Washington correspondent Lorraine Woellert about how the trend is contributing to price fluctuations and where it's going next.I also drew some green lines on the chart to show the long-term uptrend in price, and the diverging downtrends in MACD and RSI. This should give us pause about the sustainability of the uptrend. Beneath all the price swings in the chart lies the issue of Peak Oil. Production is peaking, creating the inevitability that supply will not meet demand in the near future, causing massive price increases. Analyst/contributor U. Doran has supplied a number of in-depth stories on the decline in both Saudi and Mexican super-giant oil fields. I recommend all these links. The BusinessWeek story accompanied the above interview; the rest of the links are courtesy of U. Doran: Barrels Of Confusion: Where crude prices go next is anybody's guess, so companies are learning to live with volatility--and Wall Street is cleaning up (BusinessWeek) Association for the Study of Peak Oil & Gas-USA--list of papers from Oct. 06 Sample ASPO-USA presentation--the Hubbert Awards for 2006 Author Matt Simmons presentation-- Is The World�s Energy Supply Sustainable? (www.simmonsco.com) Best summary of global energy realities I've ever seen in only 40 slides Low Oil Inventories Ease Opec�s Job and Add Further Upside Oil Price Risk (UBS Investment Research) A Nosedive Toward the Desert (saudi oil production decline) (www.theoildrum.com) Saudi Arabian oil declines 8% in 2006 (www.theoildrum.com) Pemex celebrates 69th anniversary, but problems loom Depleted reserves, crumbling pipelines, outdated technology and billions of dollars in debt.... (Houston Chronicle) Peak Oil Update--February 2007 (www.theoildrum.com) March 19, 2007 The Healthcare Solution: A Proposal  Long-time readers have seen this chart before, for it perfectly captures the

pressing need for true, long-term reform of the U.S. "healthcare" system.

(Long-term readers know the quotation marks indicate my view that it is actually a

system which profits not from preventive medicine but from ill-health.)

Long-time readers have seen this chart before, for it perfectly captures the

pressing need for true, long-term reform of the U.S. "healthcare" system.

(Long-term readers know the quotation marks indicate my view that it is actually a

system which profits not from preventive medicine but from ill-health.)

New contributor Peter sent in a cogent summary of the possible solutions which I encourage you to read all the way through. This is perhaps the best analysis I've read of national healthcare systems: There are actually three models of health care used in the developed world: the HMO model, of which the UK model is a variant, the US model, and the European model or social health insurance. They fall neatly onto a two by two matrix, like surprisingly many things in life. One dimension is who provides insurance, the other who provides the actual care.Thank you, Peter, for the careful analysis of various healthcare models. March 16, 2007 Self-Reliance II Yesterday's entry on self-reliance and life skills drew a number of remarkable responses from readers. Since I'm too lazy to find any art to illustrate the theme of self-reliance, I've thrown in two photos of a fence I built a year or so ago--a simple enough project, but carefully planned and assembled. I cut all the gate pieces with a Skilsaw because I'm a Skilsaw kind of guy (i.e. not a craftsman). First up is mechanic/remodeler/correspondent Anton L.:

I'm 34 years old. Born in the nadir of the 'baby bust' in 1972, I have fewer peers than most who came before and after. One thing that they have in common with the older generation is the (more of less) ability to DO things.

Next up is polymath reader Darrell C.: Your latest on self-reliance really resonated, Charles. That was me in high school in the late '60s, taking shop because it was what I enjoyed and broke up the rest of the day's math, history, etc. (I disagree with dropping shop from schools that are trying to be only academic.)Astute reader David recalls a childhood of extreme poverty, and speculates--as I do, and perhaps you do, too--on what will happen should hard times ever spread across our fair land: Charles - Cook, clean, repair something............please that is all beneath me! I pay people to do 'those things'! I am kidding but that is the attitude of most of the people I know. I have seen adult men call a tow truck to have their flat tire changed.Correspondent Mark P. checked in with a short commentary on parental responsibility: From my experience as a parent, I believe that many parents are abdicating their responsibilities to teach children about how to do things. People of my generation know how to do these things. but they have given up on many of these things due to either modern day conveniences or just plain laziness. They let their kids run wild and barely even discipline them properly.Frequent contributor Mark. D. provided an insider's experience of the decline in craft: My stepson Jeremy works for Milguard windows. In 3 mos, he went from a know-nothing punk to reinstaller, QC (quality Control inspector. There are basically two companies who do most of the windows in construction in the Bay Area, milguard and anderson. Jer says NO ONE knows how to frame what used to pass for square, since it really costs about 30% more to make things square. But these days it isn't even close. On his word, windows are yanked and windows and doors reframed. Lawsuits are common due to workmanship and the sealer used even when a disclaimer is signed by the construction company. Special extra workmanship is required on some windows, yet the builders waive it. He even reinstalls windows after they are stucco'd because they are popping.As a former builder, a number of causes come to mind: many houses are framed with green lumber which warps as it dries; the stucco is simply not as thick as it was in the 20s-40s; as the flat land got covered, then housing moved to sites with fill (as Mark notes, often not compacted), and lastly, the overall quality of the framing is so poor that settling/separation affects the stucco. Knowledgeable correspondent Cheryl A. (to whom I am indebted for recommending the book Fiasco, described in my March 9 entry) provides a valuable point of view: that of mate/family member: I read today's blog with feelings of happiness for myself and sorrow for others. My husband is a self-made man. He paid for all his own schooling, sometimes holding down up to 5 part-time jobs simultaneously. His father taught him how to wire a home, do plumbing, etc. He also helped his mother cook. (Such things are often an indication of men who make good husbands.) As a result, he does many of the repairs around our home - I draw the line at the roof! In addition he is a fabulous chef!! I feel sorry for others who are at the mercy of repair people and dining establishments.And correspondent Chuck D. offers a wide-ranging response to both life skills and literature: Loss of craftsmanship. This is been going on for a long time, particularly through the second half of the 20th century. I suspect both the cheapening of materials being used and the loss of skilled craft in handling them reflect two things - the development of mass markets where everything becomes fungible "product", and the attempt to hold down the price of materials and labor in the face of rising costs.Thank you, guys and gals, for an amazing range of commentaries. Thank you, Bill M., for suggesting the themes of quality, self-reliance and popular literature. March 15, 2007 Zen and the Art of Motorcycle Maintenance Correspondent Bill M. recently penned the following observations about the demise of quality, and referenced a book of the mid-70s which found its way into practically every adult readers' hands at that time, Zen and the Art of Motorcycle Maintenance: An Inquiry Into Values Bill is a craftsman, carpenter/builder and artist. As an example of his work, here is one of his recent creations, the U.S. Constitution Chime of which he has made a set of 13 (the number of the original states). Other chimes are displayed on his website. Long-time readers will anticipate that Bill's comments on craft and self-reliance resonated very strongly with me: