|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Writing/Film Dear Aspiring Writers: The Worst Advice You'll Ever Read A Literary Look at I-State Lines Spirited Away: Decay and Renewal An American Poem (Robinson Jeffers) Taoist Chinese Poems The Nelson Touch "It's all about oil, isn't it?" Kurosawa's High and Low A Bountiful Mutiny Howl's Moving Castle Thailand's Iron Ladies Trois Colours: Red The Thin Man: Thoroughly Modern Movies Why My Book Is Better Than the DaVinci Code Iranian Films: The Mirror Piratical Nonsense A Real Pirate Movie: Captain Blood 2005-06 archives 2007 archives Recommended Books American Identity American Identity Literary Contest Winners, 2006 (fiction and essays) Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Your Tattoo in 50 Years The American House and Frank Lloyd Wright Cultural Commentaries On Hatred and Anti-Americanism Anti-Americanism Part 2 Anti-Americanism Part 3 French-Bashing Germany: We All Have Problems, But... Kroika! Chronicles This Blog Sells Out Doom and Gloom Sells The Kroika Mascot-"Auspicious Pet" Wal-Mart and Kroika Kroika and Starsbuck Take a Hit Kroika Ad 1 Kroika Ad 2 Kroika Ad 3 Kroika Ad 4 Kroika Makes Bid for Oreo (April 1) Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Corruption and Avian Flu: China's Dynamic Duo Exporting the Real Estate Bubble to China Is the Bloom Off the China Rose? China Irony: Steel, Marx & Capital Curing The U.S. and China's Dysfunctional Relationship China and U.S. Inflation Trade with China: Making Out Like a Bandit Whither China? Will the Housing Bust Take Down China? China's Dependence on Exports to U.S.; Is China About to Pop? 2005-06 archives 2007 archives Battle for the Soul of America Katrina, Vietnam, Iraq: National Purpose, National Sacrifice Is This a Nation at War? A Nation in Denial Why Is This Such a Tepid Time? That Price Isn't Cheap, It's Subsidized The Most Hated Company in America U.S. Fascists Seek Ban on Cancer Vaccine The Truth About Christmas American Dream or American Nightmare? 2006 Sea Change Obesity and Debt Immigration Ironies U.S. Healthcare: Working Toward a Real Solution A Drug Industry Running Amok Where There Is Ruin 2005-06 archives 2007 archives Financial Meltdown Watch What This Country Needs Is a... Good Recession Are We Entering the Next Age of Turmoil? Why Inflation Appears Low Doubling Down on 5-Card No-See-Um A Rickety Global House of Cards Are Japan and Germany Truly on the Mend? Unprecedented Risk 2 Could One Rogue Trader Bring Down the Market? Worried about Inflation? Stop Measuring It Economy Great? Bah, Humbug Huge Deficits and Huge Profits: Coincidence? Who's The Largest Exporter? Three Snapshots of the U.S. Economy Loaded for Bear Comparing Nasdaq to Depression-Era Dow Who's Buying Treasury Bonds? And Why? Derivatives: Wall Street Fiddles, Rome Smolders Financial Chickens Coming Home to Roost Is the Stock Market on the Same Planet as the Economy? The Housing-Recession-Oil-Healthcare Connection Could We Have Deflation and Inflation At the Same Time? What We Know, What We Can Safely Predict Bankruptcy U.S.A.: Medicare, Greed and Collapse Sucker's Rally A Whiff of Apocalypse Where There Is Ruin II: Social Security 2005-06 archives 2007 archives Planetary Meltdown Watch The Immensity of Global Warming Sun Sets on Skeptics of Global Warming Housing Bubble Watch Charting Unaffordability A Monster of a Housing Bubble A Coup de Grace to the Economy Hidden Costs of the Housing Bubble Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Housing Market Slips Toward Cliff Housing Market Demographics Housing: Catching the Falling Knife Five Stages of the Housing Bubble Derailing the Property Tax Gravy Train Bubbling Property Taxes Have You Checked Your Property Taxes Recently? Housing Bubble: Where's the Bottom? Housing Bubble: Bottom II The Housing - Inflation Connection The Coming Foreclosure Nightmare 1 How Many Foreclosures Will Hit the Market? Housing Wealth Effect Shifts Into Reverse Housing Bubble Bust Will Take Down the Global Economy The New Road to Serfdom: A Negative-Equity Mortgage The Housing-Savings-Recession Connection After the Bubble: How Low Will It Go? After the Bubble: Rents and Housing Values Why Post-Bubble Rents Matter After the Bubble: How Low Will We Go, Part II Housing: 10% Decline May Trigger Financial Ruin How to Buy a $450K Home for $750K Inflation and Housing: Calculating the Bust The Growing Financial Risks of the Housing Bubble Construction Defects: The Flood to Come? Construction Defects Part II Who Gets Hammered in the 2007 Housing Bust Real Estate Bust: The Exhaustion of Debt What Happens When Housing Employment Plummets? One More Hole in the Housing Bubble: Insurance Financial Kryptonite in a "Super-Strength" Housing Market Three Secrets to Unloading Property Today Welcome to Fantasyland: Housing's "Soft Landing" Why Is the Median House Price Still Rising? Why Median Prices Appear to be Rising? The Root Cause of the Housing Bubble Housing Dominoes Fall Twilight for Exurbia? Phase Transitions, Symmetry and Post-Bubble Declines Housing's Stairstep Descent 2005-06 archives 2007 archives Oil/Energy Crises Whither Oil? How much Is a Gallon of Gas Worth? The End of Cheap Oil Natural Gas, Naturally High Arab Oil Money and U.S. Treasuries: Quid Pro Quo? The C.I.A., Oil and the Wisdom of Crowds The Flutter of a Butterfly's Wings? A One-Two Punch to a Glass Jaw Running Out Of Oil vs. Running Out of Cheap Oil 2005-06 archives 2007 archives Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds Geezer Rock Overload Paying for Web Content Light-As-Air Pancake Recipe In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono Happiness for Sale: Jank Coffee Ten Guaranteed Predictions for 2010 Why My Book Is Better Than the DaVinci Code My Brand Management Stinks Design Follies The New Jank Coffee Shop Jank Coffee, Upscale Tropic Style One-Word Titles Complacency Nostalgia Lifespans Praxis Keys to Affordable Housing U.S. Conservation & China Steve Toma, Me & Skil 77s: 30 years of Labor Real Science in the Bolivian Forest Deforestation and Sustainable Forestry The Solar Economy (book) The Problem with Techno-Fixes I Love Technology, I Hate Technology How To Blow off Web Ads and More 2005-06 archives 2007 archives Health, Wealth & Demographics Beauty of the Augmented (Korean) Kind Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Is Obesity an Inflammatory Response? Demographics & National Bankruptcy The Decline of Europe: A Demographic Done Deal? Are the Risks of Obesity Overstated? Healthcare: Unaffordable Everywhere Medication Nation The New Disease We Just Know You've Got Can You Can Tell Which Pill Is Fake? Bankruptcy U.S.A.: Medicare, Greed and Collapse The 10 Secrets to Permanent Weight Loss 2005-06 archives 2007 archives Landscapes Selling the Landscape The Downside of Density Building Heights and Arboral Roots Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Waimea Canyon, Yosemite, Camping & Pancakes Nourishment The French Village Bakery Ideas What Is Happiness? Our Education System: a Factory Metaphor? Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi Splogs, Blogs and "News" "There is no alternative to being yourself" Is There a Cycle to War? Leisure, Time and Valentines Is the Web a Giant Copy Machine? Science Matters Anti-Missile Defense: Boost Phase Vulnerability History The Strolling Bones: Rock of Ages Bad Karma: Election Fraud 1960 Hiroshima: First Use All the Tea in China, All the Ginseng in America Friday Quiz Pet Obesity The Origins of Carbonara Organic Farms Oil and Renewable Energy Human Diseases Wine and Alzheimers Biggest Consumers of Chocolate 2005-06 archives 2007 archives Essential Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So Fewer: How the New Demography of Depopulation Will Shape Our Future The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal The Future of Life Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies Twilight in the Desert: The Coming Saudi Oil Shock and the World Economy The Solar Economy: Renewable Energy for a Sustainable Global Future The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Feeling Good: The New Mood Therapy Revised and Updated Recommended Books More book reviews Archives: weblog March 2007 weblog February 2007 weblog January 2007 weblog December 2006 weblog November 2006 weblog October 2006 weblog September 2006 weblog August 2006 weblog July 2006 weblog June 2006 weblog May 2006 weblog April 2006 weblog March 2006 weblog February 2006 weblog January 2006 weblog December 2005 weblog November 2005 weblog October 2005 weblog September 2005 weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

|

Are Global Stock Markets Really That Much Higher? April 30, 2007 Amidst the hoopla about record highs in the Dow Jones Industrial Average and many other global markets such as Korea and China (Shanghai Composite), it's worth asking: how are they doing priced in a non-paper tangible good such as gold? Why ask? As frequent contributor Harun I. notes below: "An Asset Is Only Worth What It Will Buy." In other words, if an asset (say a basket of stocks) rises in nominal terms, but it buys less tangible goods, then has it really risen, or was the rise illusory? Let's look at two charts Harun has provided:

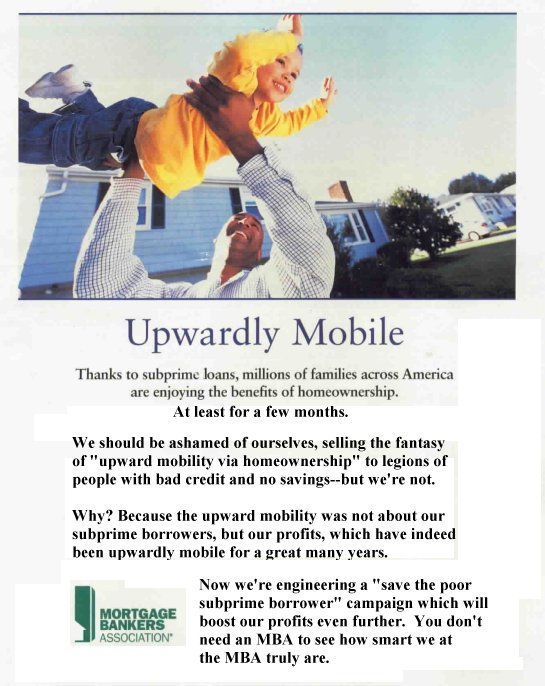

In this "alternative view," the stock market's rise is revealed as being one of numbers rather than actual tangible value. Put another way: if your money buys 20% less than it once did, then a 10% raise isn't an increase at all except in nominal terms. As the calendar turns and the old Wall Street adage to "sell in May and go away" kicks in, the illusion of "record highs" demonstrated above is worth pondering. Thank you R.S. ($30) for your generous and thoughtful donation. I am greatly honored by your support. All contributors are listed below in acknowledgement of my gratitude. This Week's Theme: Disconnect from Reality Waste April 28, 2007 Very few people comment on the tremendous waste built into our lifestyle, governance and culture. Consider food. Having been raised in a simpler time by people whose childhood memories were of the Great Depression, wasting food remains tantamount to a sin. Have you observed how many people (adults and their kids) treat food today? As something of so little value that it can shoveled into the garbage while still warm. This still makes my blood boil--not because of memories of hunger or want, but from the awareness of how hard it is to nurture and harvest the foods we eat. It is not effortless, or free. The level of waste in every sector and every level of our society is staggering. Like everything else we've addressed in "Disconnect from Reality" Week, this truth has been obscured by habit and cultural blindness. Thus we accept as "normal" that vehicles get 20 miles per gallon of gasoline rather than 30, 45 or even 90 m.p.g.--as if petroleum, like food, water and employment, is limitless. If you think that level of fuel efficiency is farfetched, then please read the Rocky Mountain Institute's The Hypercar� Concept about a standard-looking car which achieves 3 to 5-fold increase in fuel efficiency through lightweight materials and other technologies. The RMI site is a revelation, from its slogan--"Abundance by Design"--to its many practical alternatives to wasting energy. In many American homes, the heat or air conditioning is on much of the time; if buildings were designed properly (and a McMansion is not), there would be much less need to burn energy to heat or cool interior spaces. This is a non-trivial issue, for a huge amount of our energy is devoted to just that. The general view in our culture is "let the market handle it." In other words, when gas is $5 a gallon, people will start building and buying hyper-efficient vehicles. Nice, but it takes about 15 years to replace the nation's vehicle fleet. So if Peak Oil strikes with a vengence--as evidence suggests it will--then gasoline could rise quickly to $5/gallon and then move ever higher. So what do you tell the 95% of the citizenry who still own a gashog vehicle? "The market will handle it" sounds pretty hollow. The question will be: why didn't someone anticipate $10/gallon gas and prepare the nation? Consider granite countertops, jacuzzi tubs and oversized appliances. At least 15 million new homes /condos have been built in the current housing boom, and the vast majority feature essentially useless expenses such as huge refrigerators, granite countertops, marble entries, three bathrooms, water-wasting jacuzzi tubs (in the desert, mind you) etc. ad nauseum. These essentially needless "features" cost at least $20,000 per housing unit (a very conservative estimate). What if the installation of $20,000 solar panels had been mandated or encouraged by tax credits, and the marble/granite/Subzero fridge had not been installed? Would the nation be better off with 20% of its electricity being generated by solar panels rather than 2%? Would we as a nation be better off if the funds misallocated into useless McMansion "features" had been invested in energy independence? When the cost of energy doubles, and then doubles again, we will look back not just on the waste but on the misallocation of capital as terrible sins against our children and grandchildren. If you still harbor doubts about Peak Oil, please read Peak Oil: Denial Won't Fill Your Tank (April 12, 2007) and check previous entries in the 2005-2006 archives listed under "Oil/Energy Crises." Waste has another venue--jobs. The level of wasted motion and money in our economy is stupendous and little-noted. Is it really necessary to spend 30% of our healthcare dollars on shuffling paperwork around? No doubt you each have your own stories of insane inefficiency--due to incompetence, habit, union rules, Congressional mandates--the list is endless. Though I can't find the clipping, I saved a "Nobody Asked Me, But..." column from the U.S. Naval Institute's Proceedings awhile ago. Here is the story it told. A Reserve officer recounted how hard he and his mates had to work to maintain the aircraft and sortie rate in his stateside unit. Then the 90s budget cuts lopped away about half the unit's staffing. Lo and behold, the same number of sorties were flown with half the people. What was left undone: tertiary reports and paperwork, meetings--all the usual non-productive "essentials." Here's another story. I worked for a privately funded non-profit in the late 80s. The staff consisted of about 8 or 9 part-time people, all doing specific jobs: bookkeeper, PR, publications, ad sales, class schedule, registration, manager, etc. There were always meetings to attend, many in the evening because everyone was so busy. The recession of 1990-92 took down much of the center's funding, and by the middle of the decade, virtually all the tasks which had once "required" 8 or 9 staffers were performed by one-full time employee and a single on-call very-part-time assistant. The publication got trimmed, but the number of events/classes offered remained the same, as did the clientele served. My point: there is no way to know just how extremely efficient people can be until there is no choice but extreme efficiency. We have a "full employment" economy now, but if a recession or depression kicks in, as many of us expect, how many of the jobs that will be lost won't ever come back? Once efficiency is required to survive, much of what was once considered "essential" drops away as unnecessary. To consider just one example of hundreds of thousands, here is The Wall Street Journal reporting that companies have "celebration assistants" whose entire job is flitting about heaping recognition on fragile young employees desperate for lavish praise: The Most-Praised Generation Goes to Work (subscription required, but hopefully your library carries the WSJ). Bosses, professors and mates are feeling the need to lavish praise on young adults, particularly twentysomethings, or else see them wither under an unfamiliar compliment deficit.Excuse me while I gag (as are my 20-something readers). We all know the vast majority of American companies have zero loyalty to their employees, and so this "tossing confetti" nonsense is offered up as a painfully bogus simulacrum of actual caring. This kind of phony corporate programming reminds me of the old Soviet joke: "we pretend to work, and you pretend to pay us." The updated U.S. version might be: "You pretend to care about us, and we pretend to care about your product/service." Still, one has to wonder about the current zeitgeist. In my day--not that long ago, really--our supe also had words for us, but I reckon they don't quite measure up to today's standards. If he thought we weren't working hard enough (this is construction), he'd snarl, "I want to see assholes and elbows" ( i.e. us bending over shoveling or lifting lumber, etc.). Would a delicate employee simply dissolve into mush and file a worker-compensation claim, or perhaps a lawsuit alleging abuse, were such words to reach his/her vulnerable quivering ears? If your job is "celebration assistant": look, I'm sure you're doing great work, and you may well be boosting the productivity of the crew immensely. All I'm saying is, in a deep, lengthy recession, people start working to eat, not garner heaps of praise for showing up on time, and the company goal is to survive, not juice up happy-happy praise. The larger question is: if 10 millions unproductive jobs disappear in the coming recession, what new enterprises will generate 10 million truly productive new jobs? In other words, if the 10 million (a low estimate, I wager) unproductive jobs in our economy are cut as no longer necessary, then what productive work will arise for those displaced? Perhaps we should consider the possibility that there will be a structural imbalance in employment in which 10-20 million jobs will be eliminated and no new jobs created. How could this occur? It's not hard to come up with some potential causes: offshoring of expensive tasks, the deflation of debt bubble reduces overall spending by 20%, rising interest payments reduce consumer spending by 20%, as a result government tax revenues fall by 20%, and so on. This is a sobering prospect, and one which should not be discounted as improbable. Thank you K.L. ($5) for your thoughtful donation. I am greatly honored by your generous support. All contributors are listed below in acknowledgement of my gratitude. This Week's Theme: Disconnect from Reality Brave New Online World: Marketing, Advertising and Spin April 27, 2007 Let's put to rest some cherished illusions: The first illusion has been threadbare for some time (decades?), but the wholesale surrender of independent skepticism has become painfully obvious. The quagmire which we were promised would not be a quagmire was marketed to the media and the American public with all the depth and finesse of a multi-million dollar media "buy" (advertising lingo for the integrated purchase of print, broadcast, radio and Internet advertising and PR promotion), and as Bill Moyers has documented, the media bought it hook, line and sinker: Buying the War. Here's a mea culpa from the Washington Post: A Media Role in Selling the War? No Question. You won't see any apologies from Fox News, because they're always right, regardless (pun intended), just as they won't be admitting they led the cheerleading of the housing and stock bubbles which will soon give their viewers a taste of financial "shock and awe." Does anyone actually believe print media's dependence on real estate and retail advertising has no influence on editorial content or spin? Any 12-year old can connect the dots between a media which repeats the wholesale manipulation of reality "spun" by the government's and Realtors' gussied-up "data," and their financial dependence on "healthy" real estate and retail sectors supported by consumers willing to borrow and spend. Here is a bit of inside knowledge sent in by a frequent contributor regarding the April 24 entry, "Media Disconnect": Great post today. You are more correct than you know. Back in 2000 a friend of mine at Army Intelligence (stop chuckling) informed me that the media houses were hiring MI (military intel) (okay you can chuckle a little bit) but the purpose was highly classified. Why would the government classify something the private media is doing? That is all I can say.Correspondent R.D. sent in this equally thought-provoking item: With regard to today's 'Media Disconnect' I would like to share a story: A few years ago, a close friend of mine was stuck at home in Atlanta with a brief illness. He is a Senior Producer at a major news network. I happened to be passing through town and spent the night at his house. In the morning, over coffee, he told me he would let me listen in on his conference call if I promised to stay quiet. It goes without saying, that it is bad form or unethical to allow an outsider to be on the line when other participants are unaware of you presence, but we are close friends and he knew I would find it fascinating. I don't have anything really shocking to share about the experience except to say I found it a bit chilling.Chilling is the word. But sometimes a media "buy" can be so laughably fantastic that one wonders who approved the campaign. I speak of the latest blitz by the loveable folks over at the Mortgage Bankers Association. I've taken the liberty of doing a light edit on a recent full-page glossy ad from the Mortgage Banking Association, adding a slight touch of reality to their self-serving defense of subprime lending:

Now that we've enjoyed a good laugh--those guys at the MBA should be writing for TV, haha-- here is a story which should have been a headline on page A-1 but which got buried or not reported at all: Madrid stock market falls as housing bubble bursts. Author John Kinsella (see links on the right sidebar) reports from the continent: Yesterday as you certainly know the Madrid Stock Exchange practically exploded with housing and construction firms losing up to 13% in one day�s trading.Will the implosion of Spain's housing and stock market bubble have an effect on world markets? Certainly not--because as "bad news," it's not being reported except as snippets on wire services such as Bloomberg. On to the love affair between the blogosphere and advertising/marketing. Although Google currently has a warm and fuzzy rep (don't you just love those crazy young billionaires Sergei and Larry?) as a highly profitable but basically benign juggernaut of search and advertising, I predict that Google will soon be recognized as a force not unlike Microsoft: uniquely profitable and uniquely pernicious. Lest you think I should be adding (rant) tags here, please consider the implications of this story from the Wall Street Journal (subscription required but you can read it at your local library--I hope): Search Engines Seek to Get Inside Your Head. Search engines have long generated the same results for queries whether the person searching was a mom, mathematician or movie star. Now, who you are and what you're interested in is starting to affect the outcome of your search.Where do you think the default will be set on your permission to "let Google track it"? Hmmm... boy, this is a tough one. Sure, you can opt out--if you can find the "opt out" button or link. I don't care if they keep "the consumer's" (that's you) identity "protected"--the issues are: what if you don't want individualized ads? Who benefits from this barrage of advertising aimed at you? And what does enabling that barrage do to the source's credibility--i.e., the blog hosting the Google ads? Now the general view is: ads on "corporate" sites--bad. Ads on blogs--benign. Wait a minute. How can ads on corporate sites be pernicious and the same ads on blogs be benign? Lest you think there is no chance of us noble, unsullied-by-ubiquitous-marketing blogger types being influenced by evil corporate marketing and spin, read this from BusinessWeek: "Polluting The Blogosphere: Bloggers are getting paid to push products. Disclosure is optional." "You can't believe anything you see or read," complains Ted Murphy. "You think those judges on American Idol want to drink those giant glasses of Coke?"The piece goes on to say bloggers are paid $5 to $10 for "praising" the object of a media "buy"--without disclosing they were paid to do so. Hey, I will denounce, decry, mock and belittle any ad campaign for free! And if you don't believe me, well, you need a prescription of Zombiestra (TM) The Marketing Machine views all media outlets, even a small blog, as a pipe to channel their "message" and every citizen as a "consumer" of media and their products/services. Google is a profit-making juggernaut because it pipes ads directly to millions of pages and tracks tens of millions of "consumers" web "experience." Combining seemingly benign "search" to the trillion-dollar frenzy to pipe directly into consumers' eyes, ears and minds is not benign. You've been "assimilated" if you discount the pernicious effects of marketing on credibility and the "web experience" of visitors. What if you don't want your "web experience" cluttered with a bunch of hidden marketing and all-too-visible advertising? Sorry--you don't have that option. The usual excuse--and make no mistake, it is an excuse--is, "oh, we all just ignore the ads." If this is so, then why is Internet advertising exploding? Are marketers and spin-meisters dumb enough to expand what isn't working? I think not. What surprises me is how little resistance is offered to this worldview that relentless spin, marketing and advertising--and please note all three are simply shades of the same color--green--have no effect on the experience of those visiting those sites. To reiterate what is posted elsewhere on this page: I accept no advertising or marketing. I post links to books and films I recommend on Amazon.com, and if you buy said film or book on Amazon I receive a small slice (1-3%). (You can usually borrow the book at the library for free, but you'll have drawn some benefit--for free--by reading other readers' reviews and comments.) I receive no money for you clicking on the link. A thousand readers can scan the online readers' reviews (the feature I value) and I receive nothing. Amazon provides a forum for other readers' opinions and that is worth the link in my opinion. I also provide a link to Amazon gift certificates because I have found these to be an easy-to-send and well-received gift. I also receive a small slice (3%) of these sales. In a similar fashion, I have a link which enables buying physical gold, something else I believe in. That I get a commission should you buy something via these links is clearly stated. I also provide links to buy my novel I-State Lines which I also believe (despite a complete lack of evidence) has some merit. Does posting these links and recommendations make me part of The Machine? Perhaps to some visitors it does; in my view, these are services which I value and recommend, and that's quite different from serving up ads from Google which are selected by Google to match the profile of the site's content or the visitors' "preferences," and being paid to do so whether I value the product or service being marketed or not. What I would welcome is a flinty-eyed look at marketing's reach and influence on the Web. If that skepticism extends to my own site, fine. If my readers worry that the links to books I recommend on Amazon are affecting my choice of topics and coverage, then I would blow off the links. What's important is the dialog between "media source" and its "consumers," and the willingness of the "media source" to forego advertising as a way of protecting credibility and the experience of its visitors. There are two alternatives to selling advertising or hidden marketing: subscriptions (usually called "premium content") or donations. Since I don't have any "premium content" (if I could tell you how to make a million bucks, I would just make the million bucks myself and give you the secret for free), I have--at readers' suggestions--tried the donation alternative. If you like what you find here, then you can donate the equivalent of a subscription (cost of one movie and a medium popcorn at a theater: $12)--or you can read it for free. Either way, your readership is appreciated. Thank you A.C.H. ($15) for your generous donation. I am greatly honored by your support. All contributors are listed below in acknowledgement of my gratitude. Hey, you tipped the guy behind the bagel counter a buck, why not Your readership is greatly appreciated with or without a donation. This Week's Theme: Disconnect from Reality The "No Bad News" Market April 26, 2007 In honor of the Dow Jones Industrial Average crossing 13,000, we look at a market fully disconnected from its exposure to risk. What characterizes this disconnect? There can literally be no bad news. For example: Consumer spending drops. Excellent! The Fed will have to lower rates. Consumer spending rises. Wonderful! Corporate profits will continue rising, too. Fewer jobs were created last month. Outstanding! Weakening job market will push Fed to lower rates. More jobs were created last month. Super! Rising employment will drive higher spending and profits. Inflation drops. Wow! Corporate profits will rise as borrowing costs decline. Inflation picks up. No worries. The "core" rate (i.e. everything which increases in price has been subtracted) is still basically zero. Party on! Housing starts rise. I'm lovin' it! The "softness" is done, housing is strengthening, the boom continues. Housing starts fall. Great! With fewer houses being added to inventory, then the inventory will get worked off quickly, setting the stage for--you guessd it, another boom! This could easily be extended to cover any news whatsoever: Los Angeles leveled by giant quake. Construction boom will drive commodities and sales ever higher--this will be a fantastic boost to employment. Saudi Arabian government overthrown, radical Clerics in charge. The doubling of oil to $150/barrel will drive energy company profits and boost spending on alternatives--profits will abound. China's economy falls off cliff, social unrest widespread. This will reduce that pesky trade deficit and cut oil demand in China, lowering prices for U.S. consumers. This could be a board game: the "no bad news" stock market. You draw a "disaster card" and then have to spin it into good news which boosts "market prospects." But before we start believing the game is actually real life, let's look at some charts:

Note how the DJIA swings from the top to the bottom of its channel. It has punched through the upper band decisively, suggesting a reversal is in order. Note how the VIX has retraced, setting up a potential "third spike" eerily similar to what unfolded last July. As for market sentiment--there is only one word to describe it: euphoria. There can never be any bad news, so it can only run up. The only danger is being out of the market. Does this strike you as an extreme of bullish sentiment? As a market disconnected from an economy in which foreclosures are rising by double-digits every month? Join the party if you must, but keep an eye on the punchbowl--it's looking like it was spiked with a vintage March 2000 elixir that packs a real hangover. One last note: Technical Analyst Rick Ackerman over at Rick's Picks has long identified 13,045 as an important top in the DJIA, and now that the DJIA has blown past that to close at 13,088, he has raised his target a couple notches. Various bullish pundits are already touting Dow 14,000, saying it's only 7% higher; the fact that a thousand points is now considered a modest step suggests to me that the bullish fever is about to break. Thank you A.B. ($20) for your generous donation in support of this advertisement / marketing garbage-free website. I am greatly honored by your support. All contributors are listed below in acknowledgement of my gratitude. This Week's Theme: Disconnect from Reality The American Diet: Manufacturing Ill Health April 25, 2007 This chart shows how the U.S. stacks up against other nations in citizens over the age of 25 with a body mass index (BMI) of over 30:

If you're not sure what the BMI measures, or what your own BMI is, go to the National Institute of Health BMI calculator. The basic idea is that weight and height are relational: the taller you are, the higher your weight. The criticism of the BMI is that very muscular or stout people end up with a high BMI number even though they are fit. There is a weakness in any simple metric, of course, but the BMI is a generally accurate assessment of "healthy weight." As expected, developing nations like Egypt and Asian nations with low-fat, low protein cuisines like Japan have few obese adults. The surprise is that European nations with high-fat diets rich in chocolate and cheeses like France are relatively low. (Switzerland, though not shown, was just above Japan despite a very high per capita intake of chocolate.) This suggests that fat alone (or sweets alone) cannot be singled out as the "cause" of obesity. Now please don't take this entry personally if you are overweight. By the NIH standards of what constitutes "normal weight," some 2/3 of American adults are overweight or obese. Since this wasn't the case 40 years ago, we have to ask what's different now. Could it be the genetic composition of U.S. citizenry? While immigration has brought an influx of Hispanic and Asian peoples into the U.S. in those 40 years, there is no evidence to support the notion that an influx of obese people or people tending toward obesity has skewed the genetic pool to the point that fully 1/3 of the adult population is unhealthily heavy. Here are the usual suspects: declining physical activity, growth of fast food, hurry-up meals and harried parents who have given up control of their children's diets. There is of course some truth in each of these assertions, but the elephant in the room nobody seems to talk about is this: Consuming the American food industry's products inevitably lead to obesity and poor health. Now before you freak out and start emailing me about "personal responsibility" and related issues, allow me to relate my own struggle to find food products which aren't basically deadly. Yes, we are each responsible for our own food purchases and intake. But to narrow the diseases of obesity down to an individual failure to control caloric intake is to miss this point: There is virtually no healthy food available in any American supermarket beyond the produce, bread, dairy/soy and fresh meat/fish aisles. As you may recall from earlier posts, I discovered I have high blood pressure last year--not super-dangerous like 180/100, but readings in the 130-140 / 90 range. My doctor explained that if there is anything we know for sure, it's that high blood pressure greatly increases the risks of stroke and heart disease. Slam dunk, no debate, end of story. He recommended that I start taking medications to lower my blood pressure. As long-time readers know from Zombiestra and other drug parodies I've created here, I am not a big fan of medications, especially those with side-effects and those whose interactions with other meds have been poorly studied, i.e. all of them. My BMI is 21.8, well within the "normal weight" range of 18.5-24.9, so my weight obviously wasn't the key factor. Though my doctor cited genes as the primary cause, I suspected lifestyle might have some wee effect as well. Thanks to polymath contributor U. Doran, who sent me some links on salt and blood pressure, I discovered that just as we've been told for decades, salt is the key factor (along with weight) in controlling blood pressure. Stress and diet are of course also factors, but it's harder to measure the impacts of these complex metrics. Here is a long-term study which supports the connection between lowering salt intake and lowering the risk of heart disease: Scientists prove that salty diet costs lives; "Eating less salt reduces the chances of suffering a heart attack or stroke, the first long-term study of salt�s impact on health confirms today." The usual image of a high-salt diet is someone shaking loads of salt on their steak or veggies. Too bad it's not this simple. A careful study of standard American manufactured foods has led me to conclude that even if you don't add a single grain of salt to a single morsel of food, you are eating far more salt than is healthy. And by manufactured foods I don't mean just frozen dinners; I mean canned beans, prepared salads, packaged noodles, sausage, snacks, etc. Everything which isn't fresh produce, bread. dairy/soy or fresh meat/fish, i.e. foods which require some preparation. The "recommended salt intake per day" is about 2300 mg (milligrams), which in terms of limiting your risk of dying prematurely should be viewed as a maximum best avoided--about half that would be a better target. So let's "eat healthy"--low fat and low sugar--and see how we do: Breakfast: Wheat Chex: 420 mg of salt and a low-fat Aidells sausage: 300 mg Lunch: Trader Joe's mushroom rice noodle soup bowl: 700 mg one bag of low-fat chips: 600 mg dinner: organic garbanzo beans, 390 mg, salad with blue-cheese dressing with bacon bits (500 mg), frozen low-fat enchiladas (750 mg.) Total salt content of "low calorie, restricted fat" diet: 3660 mg. What can we say about this level of salt intake? It raises the risk of stroke and heart disease. Put simply: it will very likely take years off your life. So next time you're in a fast food outlet or a supermarket, try to find something you can eat that won't kill you. It will be a challenge, I guarantee you. I have lowered my blood pressure to 117-128 / 72-81 by following a modest regime of stress reduction, salt reduction, slightly increased exercise and substituting fresh ginger tea for caffeinated black or green tea (which I still drink in small quantities). To reduce my salt intake, here's a short list of what I no longer eat: In other words, literally everything in the supermarket except the fresh produce and the meat counter (with rare exceptions like frozen blueberries, which are essentially produce anyway). If you want to locate the cause of American obesity and poor health, look no further than the label on virtually every item in the American supermarket. One last story on deceptive labeling: I was looking for some plain old peanut butter, a product you'd think you could find somewhere which hasn't been adulterated with added sugar and hydrogenated oil (to keep the natural peanut oil from separating.) I happened upon some "organic peanut butter" in Costco and my hopes were raised that here was a genuine unadulterated jar of peanut butter (OK, with some salt added). No way. The "organic" peanut butter was loaded with hydrogenated palm oil. Is this dollop of goop also "organic" and therefore "good for you"? If this isn't deceptive, shall we call it misleading, or purposefully confusing? Whatever label you choose, it's clear that the American food products industry neither manufactures healthy products nor enables consumers to make healthy choices. Thank you R.H. ($25) for your generous donation in support of this advertisement / marketing garbage-free website. I am greatly honored by your support. All contributors are listed below in acknowledgement of my gratitude. This Week's Theme: Disconnect from Reality Media Disconnect April 24, 2007 What are the odds of you seeing an honest headline like these in a major U.S. publication: Real Inflation 7.5% a year, Phony "Core" Rate 2.5% or Gov't Beancounters Create 80,000 Phantom "Jobs" Last Month or Analyst: Stats Guarantee Recession in '07 The odds of blunt honesty in a major media outlet are near zero.

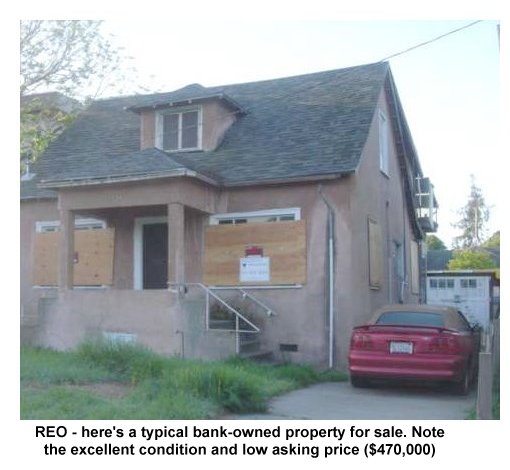

As newspapers shrink in readership and viewers leave network television in droves, the media is desperate for ways to stem the losses. One heavily hyped idea in the print media (newspapers) is to focus on "local coverage" which is unavailable on the Web. Another heavily hyped "solution" is to focus on "new media" such as the newspapers' free websites and podcasts as a way of building Web ad revenue. But what virtually no one identifies as the problem is lack of credibility. Maybe young people are abandoning newspapers because they think YouTube and Yahoo are "news." Perhaps--or maybe the idea of paying $200 a year for a "delivered daily" hard-copy newspaper doesn't seem worth it. Or perhaps the reality is much uglier: the major media can no longer be trusted as a source of non-corporatized, non-government-massaged information. As a free-lance contributor to major media (newspapers) for 20 years, I am far from the centers of decision-making within the industry; nonetheless, I retain a feel for the tenor of what editors are seeking and pick up various signals on the issues and directions being explored. As a reader, I routinely read a variety of newspapers, including The Wall Street Journal and other "top 10" U.S. newspapers, as well as The Economist, Atlantic Monthly, The New Republic, Foreign Affairs, Scientific American, National Geographic, Proceedings of the U.S. Naval Institute, BusinessWeek, Smithsonian and MAD. (Hey, I spend a lot of time with teenagers.) What I am picking up is full-blown panic. The advent of free online classified sites like craigslist has gutted what was once the mainstay of print media advertising. Now the print media is rushing into the online "new media" world, hoping to build an audience large enough and stable enough to support charging high rates for Web ads. Here is a typical story (from The Wall Street Journal, subscription required) Papers' Web Hopes Dim a Bit; Ad Growth Online Slows as Sources For News Burgeon: One major issue for many newspapers online: Roughly 70% to 80% of their online revenue is tied to a classified ad sold in the print edition -- known as an "upsell," says Paul Ginocchio, a newspaper analyst at Deutsche Bank. And as newspapers see a sharp erosion in classified advertising for real estate and jobs, their Web sites are being hit as well.What I am not picking up is any sense that the media grasps that it has become little more than shills for government spinmeisters and corporate interests. In case you don't follow these things: the major media (print, radio and broadcast TV) is mostly owned by a handful of global corporations. With Google buying YouTube and Doubleclick, the same sort of aggregation of power is also occurring online. Old Media conglomerates are buying flash-in-the-pan sites like MySpace for billions, desperately trying to extend their dominance online. Old-line newspapers like The New York Times are being pressured to generate more profit, or be sold off. The Los Angeles Times is on the sales block--not profitable enough!--and entertainment billionaire David Geffen is a likely buyer. In other words: it's all about the money. The traditional media gets very defensive when accused of blurring the line between advertisers and marketing and the "content" or "editorial" news desks; but just because marketing doesn't choose the stories doesn't mean they aren't running the paper. Here's how it works. Corporate (i.e. top management) sends down word that revenues are sinking and "we need to do more online and more local news." So editorial resources (i.e. journalists, photographers and editors) are assigned or told to generate "soft news" fluff like movie review podcasts, features on local fashion designers, and "man on the street" coverage about neighborhoods. Nice, but did anyone notice that the nation is at war, the economy has been propped on a teetering volcano of debt which is about to explode and that justice is routinely being subverted at the highest levels of our government? Maybe "corporate" isn't noticing, but readers are, and that explains why websites like Financial Sense, Prudent Bear, Minyanville and many others are attracting readers hungry for the truth or at least a skeptical view of the official cheerleading treacle reprinted and broadcast as "fact" by the major media. With the paper's (or magazine's or network's) resources thus siphoned off to cover fluff, then there are few if any resources left to cover stories which go to the heart of the rot weakening the nation. There are occasional hard-hitting stories coming out of those media outlets which still maintain investigative staff, and sites like patrick.net helpfully aggregate this "real news" from the cheerleading garbage reprinted/broadcast by second-tier media. But I invite you to analyze the story placement of major media. Where did the piece on subversion of justice by the Imperial Branch--oops, I mean the Executive Branch-- appear? On page A-6? Were skeptics' views quoted in order to be shot down by "experts"? Was there any graphic or photo accompanying the story, or was it buried and made "dry" with a boring headline and back-page placement? This kind of weak, subtly biased coverage allows the paper (or broadcast outlet) to say they're really covering this topic hard, but a close look reveals they've softened it to the point of forgotten mush via subtle cues of placement, headlines, art and editorial bias in the selection of "experts" and framing of the context. I also invite you to add up column inches or online screen space given over to celebrities, fashion, popular music, food/diet, travel, wine, luxury goods and sports and that devoted to actual reportage (i.e. not wire service reprints). There was a time in recent history when the nation was slipping into crisis and the media dropped the ball: the Vietnam era. Nowadays, you tend to hear about the blunt coverage of Vietnam by Walter Cronkite and the heroic Watergate investigations of Woodward and Bernstein. But what's forgotten is the soggy cheerleading that typified most of the coverage. This is not partisan politics. The Democratic Party held Executive Branch power from 1961 - 1968, and that's when the lying, prevarication and obfuscation of reality by government agencies became the norm (along with domestic spying and manipulation of "justice"). The Republicans held Executive power from 1968 - 1976, and were by and large delighted to build on the lies and misrepresentation which characterized the Johnson administration's handling of Vietnam. Many of the distortions still being deployed (like the phony "core rate" of inflation) were created in this time frame, for the express reason they are deployed today: to con/lull the public into acquiescence. The book I recommended last week, Reminiscences of a Stock Operator When the markets are sound and rising, insiders are buying and saying nothing. Why drive the price up before you've bought cheap? But as the economy weakens and stocks, real estate and bonds are set to roll over and decline, then insiders need to convince the public to keep buying so they can unload their assets at top prices. Have you noticed the shrill ubiquity of "reassurance" lately? Everyone from Ben Bernanke down to your local real estate board is issuing daily, if not hourly, reassurances that the economy is fine, housing is fine, stock markets are fine, bonds are fine, and really, everything is fine--just keep buying! This proves the exact opposite is true: things are not fine, and all asset classes are set to collapse once insiders and those in the know have sold. Astute reader R.Y. reminded me that the best analysis of corporate control of the media (or one of the best) is Manufacturing Consent: The Political Economy of the Mass Media The book was the basis for an excellent documentary which has aired on PBS: Manufacturing Consent - Noam Chomsky and the Media Note: one reason I will never accept advertising on this site is because I will never allow my readers' web viewing to be tracked by Google or any of its tentacles. Think about it: are all those "ads by google" and the hidden tracking which generate the various display ads really so benign? I think not. If you'd like to support content which is not supported by advertising or the marketing of Google-selected garbage, then perhaps you'd like to Your readership is greatly appreciated with or without a donation. This Week's Theme: Disconnect from Reality Real Estate Disconnect April 23, 2007 Let's launch "Disconnect from Reality" Week with that perennial favorite, real estate. And as a poster child of that disconnect, how about a boarded-up 100-year old "fixer-upper" in a mediocre neighborhood for $470,000?

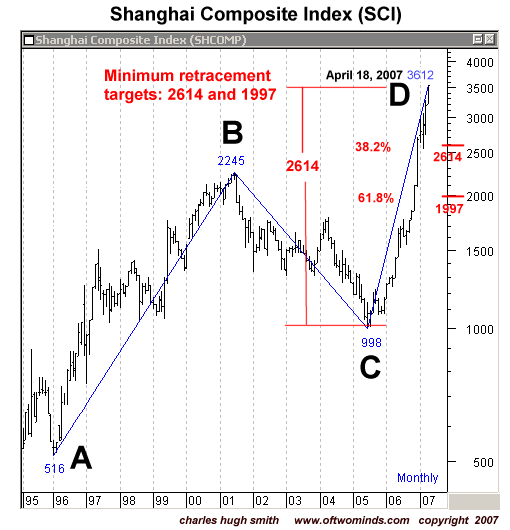

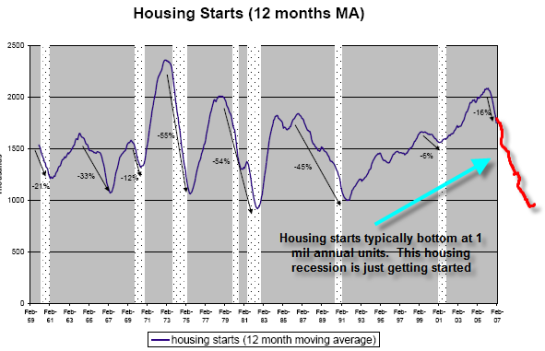

Here are the vital statistics from the listing: List Date: 04/16/07 Location: 1734 BANCROFT WAY, BERKELEY, CA 94703 Bedrooms: 3 Bathrooms: 1+ Price: $470,000 Approx Square Feet: 1315 Approx Lot Feet: 4120 Approx Lot Acres: .09 Approx age: 103 MLS#: 40258589 EBRDI Disclosures: First Right of Refusal, Rent Control, REO/Bank Owned Here's what this beauty would cost the proud new owner (mortgage estimate as per the listing): Assuming 10% ($47,000) down: Mortgage of $423,000 at 6.2% fixed-rate 30-year term: $2,591/month Insurance: ~ $110/month; subtotal = $2,700/month Property taxes (high-tax Calif) $1,000/month, subtotal = $3,700/month $100,000 equity line of credit to fund remodeling ($200K is a safer bet, but we'll assume new owner is handy): $600/month until re-sets kick in Total reasonable estimate of core monthly expenses: $4,300/month total rental income (if house were to be rented out): $2,000/month monthly cash loss: $2,300 (before depreciation, etc.) (Note that the value of the building permit gets added on to the purchase price, so the total assessed value after the renovation would be about $700,000. Oh, and don't even think about lowballing the renovation cost--the building department will insert their own "estimate of fair value" for you, regardless of the actual cost. Hint: it will be high, very high.) As a business proposition, this is a lousy deal. Assets are supposed to generate cash profits, not "tax shelter losses" and "gee, on paper, after depreciation, it's only..." losses. I didn't even include maintenance. Please note this is 103-year old structure on a crumbling brick foundation in an earthquake zone. Just fixing the foundation and plumbing/electrical would cost $100,000. Actually bringing this house up to modern standards would cost about $200,000. I know this sounds insane to those living in areas where you can still buy a house for $60,000, but the building permits alone will cost over $10,000. Yes, construction and remodeling are now the "cash cows" of many California cities, and $10,000 might not be enough to cover all the permit fees. An architect friend of mine tells me he's designing a modest addition in the Berkeley Hills, and the budget is $300,000. Kitchen remodels in excess of $100,000 are now common. Note that this is an REO: "real estate owned" by a lender. As this becomes more common (see links below), we can anticipate more such "distressed properties" being listed at absurd prices. Frequent contributor Jed H. recently outlined the probable chain of events as reality rudely intrudes on fantasy: Just the "First Inning"--Very interesting Graph of Housing Starts:Excellent summary, Jed. Here are a number of recent links which bolster this outlook: 34 percent of homeowners are clueless about their mortgage Home Prices Worst Since '94 S&P Housing Index Shows Housing Prices Fall in January Year-Over-Year, Worst Since 1994 Homeowners hit with harsh realities when payments spike Home equity delinquencies rise 7% in 4Q Here are a selection of incisive comments drawn from Credit Bubble Bulletin, by Doug Noland, 3/23/07: (Prudent Bear website) March 22 � Bloomberg (Jody Shenn): �The subprime credit crunch is beginning to ensnare even borrowers with good credit. Lenders are increasingly refusing to lend to homebuyers who can't make a down payment of more than 5 percent, especially if they won't document their income. Until recently such borrowers qualified for so-called Alt A mortgages, which rank between prime and subprime in terms of risk. Last year the category accounted for about 20 percent of the $3 trillion of U.S. mortgages, about the same as subprime loans, according to Credit Suisse Group. �It�s going to be very difficult, if not impossible, to do a no-money-down loan at any credit score,� said Alex Gemici, president of� mortgage bank Montgomery Mortgage Capital Corp. Companies that buy the loans �are all saying if they haven�t eliminated them yet, they�ll eliminate them shortly.��And for a cogent summary of the coming housing debacle/decline, frequent contributor U. Doran sent in this story from the Pimco website, and one from Safe Haven: U.S. Credit Perspectives--"Still Renting": We know from the NASDAQ bubble that once risk appetite changes, prices can shift violently in the other direction. Housing is different from equities because it is much less liquid; therefore price adjustments take more time. In a down housing market, the gap between buyers and sellers widens, and volumes fall. Buyers pull back and sellers take time to realize their listing prices are too high.Recession Imminent (from Safe Haven, by Paul Kasriel) As homebuilders' stocks rise--"the worst is over" yet again--and as inventory of unsold houses piles up, we are witnesses to a grand disconnect of hope/perception from reality. It is merely an observation, not a value judgment, that reality eventually overwhelms perception. April 21, 2007 Corporate Rot--Readers Respond The April 5 entry on "Corporate Rot" drew a number of thoughtful responses from readers, some supporting the thesis and others contesting it. While I understand how fluid labor markets contribute mightily to the "productivity" and adaptability of the U.S. economy, I am not persuaded that an obsession with short-term financial results, human-resource software filters and an atrophying of long-term experience are healthy trends. The facts are that corporate profits have risen to post-World War II highs ($1.3 trillion a year, fully 10% of the entire GDP) while wages have remained flat except within the top tier of wage-earners. Is this imbalance justified in a Darwinian way, i.e. corporations have successfully adapted to post-industrial globalization while 90% of American workers have not? The larger question is: have U.S. corporations eaten their seed corn by throwing off long-term employment as a profit-diminishing yoke? Here are six (very different) commentaries contributed by readers. In order to keep this page's file size managable, I've placed all the commentaries on a separate page. I think you'll find the variety of viewpoints most interesting. Author's Week A Stock Operator's Intuition April 20, 2007 At reader/analyst Harun I.'s recommendation, I just read Reminiscences of a Stock Operator While I hesitate to summarize such a rich source of stock market wisdom, it's worth noting that Livermore observed price data (the ticker) and gleaned patterns from price data alone which tipped him off to probable future movements. He was also a firm believer in "don't fight the tape," i.e. don't bet against a trend. His basic trading strategy was to identify the general market trend and then ride it up or down for all it was worth. But he also relied on his intuition to identify when a trend was about to change direction. Though he reported that he couldn't pin down the proximate cause of his strong feeling, he nonetheless acted on his sense that the top or bottom was in. This intuition enabled him to buy into the market just before the trend changed direction, maximizing his profit. At the risk of making a fool of myself (yet again), my intuition is the stock market is on the edge of breaking down. How far it will drop I won't even guess, but we can establish Fibonacci-derived targets. Let's start with the bubblicious Shanghai Composite Index, which just fell 4.5% yesterday and quickly bounced back 3.9% today:

Livermore noted that stocks tend to rise to round numbers. Is it just coincidence that the Dow Jones Industrial Average just topped 12,800, and the Shanghai Index clicked above 3,600? But having reached that summit--some 26% higher than a mere 6 weeks ago--how much juice is left? Enough to reach 4,000? I think not--though the Dow Jones might power on to 13,000 because, well, it's a big round number. I've noted how the SCI has traced a classic A-B-C-D move (one leg up, a retrace, then a larger upleg) and is thus poised for a major retracement. Fibonacci targets suggest a minimum 1,000 point drop with a 1,600 drop also a likelihood. Since everyone is suddenly aware that inflation could be an issue in China (Gosh, I thought inflation was vanquished globally, forever!), let's look at a chart of the U.S. 10-year bond overlaid with China's dollar reserves.