|

|

| articles | forbidden stories I-State Lines resources my hidden history reviews | home | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Writing/Film Dear Aspiring Writers: The Worst Advice You'll Ever Read A Literary Look at I-State Lines Spirited Away: Decay and Renewal An American Poem (Robinson Jeffers) Taoist Chinese Poems The Nelson Touch "It's all about oil, isn't it?" Kurosawa's High and Low A Bountiful Mutiny Howl's Moving Castle Thailand's Iron Ladies Trois Colours: Red The Thin Man: Thoroughly Modern Movies Why My Book Is Better Than the DaVinci Code Iranian Films: The Mirror Piratical Nonsense A Real Pirate Movie: Captain Blood 2005-06 archives 2007 archives Recommended Books American Identity American Identity Literary Contest Winners, 2006 (fiction and essays) Hapas: The New America Can You Tell What I am? Part I Can You Tell What I am? Part II Only in America Self-Reliance Your Tattoo in 50 Years The American House and Frank Lloyd Wright Cultural Commentaries On Hatred and Anti-Americanism Anti-Americanism Part 2 Anti-Americanism Part 3 French-Bashing Germany: We All Have Problems, But... Kroika! Chronicles This Blog Sells Out Doom and Gloom Sells The Kroika Mascot-"Auspicious Pet" Wal-Mart and Kroika Kroika and Starsbuck Take a Hit Kroika Ad 1 Kroika Ad 2 Kroika Ad 3 Kroika Ad 4 Kroika Makes Bid for Oreo (April 1) Unfolding Crises: Asia China: An Interim Report Shanghai Postcard 2004 Corruption and Avian Flu: China's Dynamic Duo Exporting the Real Estate Bubble to China Is the Bloom Off the China Rose? China Irony: Steel, Marx & Capital Curing The U.S. and China's Dysfunctional Relationship China and U.S. Inflation Trade with China: Making Out Like a Bandit Whither China? Will the Housing Bust Take Down China? China's Dependence on Exports to U.S.; Is China About to Pop? 2005-06 archives 2007 archives Battle for the Soul of America Katrina, Vietnam, Iraq: National Purpose, National Sacrifice Is This a Nation at War? A Nation in Denial Why Is This Such a Tepid Time? That Price Isn't Cheap, It's Subsidized The Most Hated Company in America U.S. Fascists Seek Ban on Cancer Vaccine The Truth About Christmas American Dream or American Nightmare? 2006 Sea Change Obesity and Debt Immigration Ironies U.S. Healthcare: Working Toward a Real Solution A Drug Industry Running Amok Where There Is Ruin 2005-06 archives 2007 archives Financial Meltdown Watch What This Country Needs Is a... Good Recession Are We Entering the Next Age of Turmoil? Why Inflation Appears Low Doubling Down on 5-Card No-See-Um A Rickety Global House of Cards Are Japan and Germany Truly on the Mend? Unprecedented Risk 2 Could One Rogue Trader Bring Down the Market? Worried about Inflation? Stop Measuring It Economy Great? Bah, Humbug Huge Deficits and Huge Profits: Coincidence? Who's The Largest Exporter? Three Snapshots of the U.S. Economy Loaded for Bear Comparing Nasdaq to Depression-Era Dow Who's Buying Treasury Bonds? And Why? Derivatives: Wall Street Fiddles, Rome Smolders Financial Chickens Coming Home to Roost Is the Stock Market on the Same Planet as the Economy? The Housing-Recession-Oil-Healthcare Connection Could We Have Deflation and Inflation At the Same Time? What We Know, What We Can Safely Predict Bankruptcy U.S.A.: Medicare, Greed and Collapse Sucker's Rally A Whiff of Apocalypse Where There Is Ruin II: Social Security 2005-06 archives 2007 archives Planetary Meltdown Watch The Immensity of Global Warming Sun Sets on Skeptics of Global Warming Housing Bubble Watch Charting Unaffordability A Monster of a Housing Bubble A Coup de Grace to the Economy Hidden Costs of the Housing Bubble Housing Bubble? What Bubble? Housing Bubble II Housing Bubble III: Pop! Housing Market Slips Toward Cliff Housing Market Demographics Housing: Catching the Falling Knife Five Stages of the Housing Bubble Derailing the Property Tax Gravy Train Bubbling Property Taxes Have You Checked Your Property Taxes Recently? Housing Bubble: Where's the Bottom? Housing Bubble: Bottom II The Housing - Inflation Connection The Coming Foreclosure Nightmare 1 How Many Foreclosures Will Hit the Market? Housing Wealth Effect Shifts Into Reverse Housing Bubble Bust Will Take Down the Global Economy The New Road to Serfdom: A Negative-Equity Mortgage The Housing-Savings-Recession Connection After the Bubble: How Low Will It Go? After the Bubble: Rents and Housing Values Why Post-Bubble Rents Matter After the Bubble: How Low Will We Go, Part II Housing: 10% Decline May Trigger Financial Ruin How to Buy a $450K Home for $750K Inflation and Housing: Calculating the Bust The Growing Financial Risks of the Housing Bubble Construction Defects: The Flood to Come? Construction Defects Part II Who Gets Hammered in the 2007 Housing Bust Real Estate Bust: The Exhaustion of Debt What Happens When Housing Employment Plummets? One More Hole in the Housing Bubble: Insurance Financial Kryptonite in a "Super-Strength" Housing Market Three Secrets to Unloading Property Today Welcome to Fantasyland: Housing's "Soft Landing" Why Is the Median House Price Still Rising? Why Median Prices Appear to be Rising? The Root Cause of the Housing Bubble Housing Dominoes Fall Twilight for Exurbia? Phase Transitions, Symmetry and Post-Bubble Declines Housing's Stairstep Descent 2005-06 archives 2007 archives Oil/Energy Crises Whither Oil? How much Is a Gallon of Gas Worth? The End of Cheap Oil Natural Gas, Naturally High Arab Oil Money and U.S. Treasuries: Quid Pro Quo? The C.I.A., Oil and the Wisdom of Crowds The Flutter of a Butterfly's Wings? A One-Two Punch to a Glass Jaw Running Out Of Oil vs. Running Out of Cheap Oil 2005-06 archives 2007 archives Outside the Box How to Make a Favicon Asian Emoticons In Memoriam: Winky Cosmos The Wheeled Vagabonds Geezer Rock Overload Paying for Web Content Light-As-Air Pancake Recipe In a Humorous Vein If Only Writers Had Uniforms Opening the Kimono Happiness for Sale: Jank Coffee Ten Guaranteed Predictions for 2010 Why My Book Is Better Than the DaVinci Code My Brand Management Stinks Design Follies The New Jank Coffee Shop Jank Coffee, Upscale Tropic Style One-Word Titles Complacency Nostalgia Lifespans Praxis Keys to Affordable Housing U.S. Conservation & China Steve Toma, Me & Skil 77s: 30 years of Labor Real Science in the Bolivian Forest Deforestation and Sustainable Forestry The Solar Economy (book) The Problem with Techno-Fixes I Love Technology, I Hate Technology How To Blow off Web Ads and More 2005-06 archives 2007 archives Health, Wealth & Demographics Beauty of the Augmented (Korean) Kind Demographics and War The Healthiest Cold Cereal: Surprise! 900 Miles to the Gallon Are Our Cities Making Us Fat? One Serving of Deception Is Obesity an Inflammatory Response? Demographics & National Bankruptcy The Decline of Europe: A Demographic Done Deal? Are the Risks of Obesity Overstated? Healthcare: Unaffordable Everywhere Medication Nation The New Disease We Just Know You've Got Can You Can Tell Which Pill Is Fake? Bankruptcy U.S.A.: Medicare, Greed and Collapse The 10 Secrets to Permanent Weight Loss 2005-06 archives 2007 archives Landscapes Selling the Landscape The Downside of Density Building Heights and Arboral Roots Terroir: France & California L.A.: It's About Cheap Oil The Last Redwood Airport Walkabouts Waimea Canyon, Yosemite, Camping & Pancakes Nourishment The French Village Bakery Ideas What Is Happiness? Our Education System: a Factory Metaphor? Understanding Globalization: Braudel Can You Create Creativity? Do Average People Know More Than Their Leaders? On The Impermanence of Work Flattening the Knowledge Curve: The "Googling" Effect Human Bandwidth and Knowledge Iraqi Guangxi Splogs, Blogs and "News" "There is no alternative to being yourself" Is There a Cycle to War? Leisure, Time and Valentines Is the Web a Giant Copy Machine? Science Matters Anti-Missile Defense: Boost Phase Vulnerability History The Strolling Bones: Rock of Ages Bad Karma: Election Fraud 1960 Hiroshima: First Use All the Tea in China, All the Ginseng in America Friday Quiz Pet Obesity The Origins of Carbonara Organic Farms Oil and Renewable Energy Human Diseases Wine and Alzheimers Biggest Consumers of Chocolate 2005-06 archives 2007 archives Essential Books The Misbehavior of Markets Boiling Point (Global Warming) Our Stolen Future: How We Are Threatening Our Fertility, Intelligence and Survival How We Know What Isn't So Fewer: How the New Demography of Depopulation Will Shape Our Future The Coming Generational Storm: What You Need to Know about America's Economic Future The Third Chimpanzee: The Evolution and Future of the Human Animal The Future of Life Beyond Oil: The View from Hubbert's Peak The Party's Over: Oil, War and the Fate of Industrial Societies Twilight in the Desert: The Coming Saudi Oil Shock and the World Economy The Solar Economy: Renewable Energy for a Sustainable Global Future The Dollar Crisis: Causes, Consequences, Cures Running On Empty: How The Democratic and Republican Parties Are Bankrupting Our Future and What Americans Can Do About It Feeling Good: The New Mood Therapy Revised and Updated Recommended Books More book reviews Archives: weblog April 2007 weblog March 2007 weblog February 2007 weblog January 2007 weblog December 2006 weblog November 2006 weblog October 2006 weblog September 2006 weblog August 2006 weblog July 2006 weblog June 2006 weblog May 2006 weblog April 2006 weblog March 2006 weblog February 2006 weblog January 2006 weblog December 2005 weblog November 2005 weblog October 2005 weblog September 2005 weblog August 2005 weblog July 2005 weblog June 2005 weblog May 2005 What's New, 2/03 - 5/05 |

|

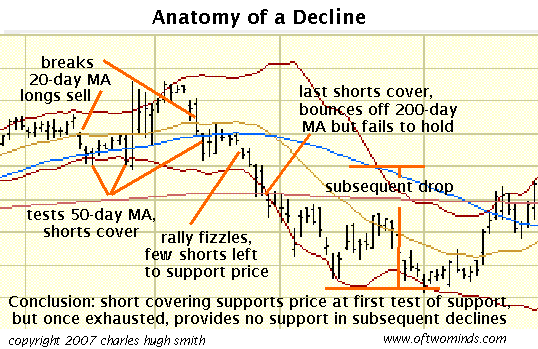

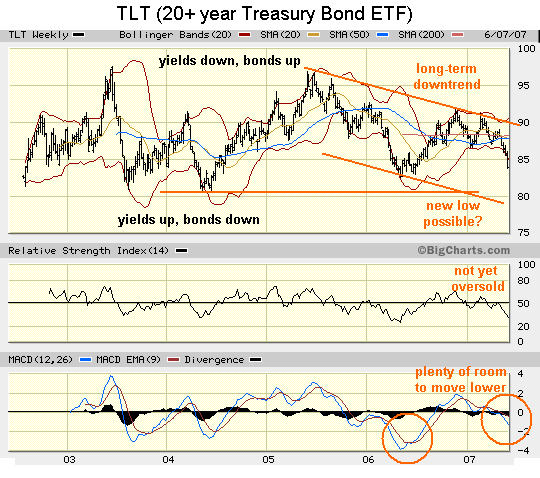

Lyrics/Poems for Our Age June 30, 2007 Frequent contributor Bill Murath sent in a song recommendation whose lyrics, he suggests, "are so fitting of the time now." Have a read/listen and see if you agree; I certainly do. The percentage you're paying is too high priced While you're living beyond all your means And the man in the suit has just bought a new car From the profit he's made on your dreams But today you just read that the man was shot dead By a gun that didn't make any noise But it wasn't the bullet that laid him to rest was The low spark of high-heeled boys If you had just a minute to breathe and they granted you one final wish Would you ask for something like another chance? Or something similar as this? Don't worry too much It'll happen to you as sure as your sorrows are joys And the thing that disturbs you is only the sound of The low spark of high-heeled boys If I gave you everything that I owned and asked for nothing in return Would you do the same for me as I would for you? Or take me for a ride, and strip me of everything including my pride But spirit is something that no one destroys And the sound that I'm hearing is only the sound The low spark of high-heeled boys The Low Spark of the High-Heeled Boys by Steve Winwood/Jim Capaldi and recorded by Traffic in 1972. My own recommendation is justifiably famous but has never seemed more accurate than in our "house of mirrors and lies/The Emperor has no clothes" era: Turning and turning in the widening gyreShall we hazard a comment and suggest the falconer is our better sense, and the falcon our nation, running out of control on so many levels, loosing a blood-dimmed tide? As for the worst being full of passionate intensity--look no further than your nearest ideologue pounding the podium for the next war, culturally or geopolitically, insulting and deriding any and all opposition with any means at hand (wishing John Edwards had been killed in a terror attack, such a thoughtful, reasonable political comment, the true voice of unmuzzled right-wing purity). As for the ceremony of innocence--a belief that no one is above the law, and that the law is above political meddling--it has indeed been drowned by Executive privilege, the last resort of liars and thieves. Yet the nation dances in the street of "endless prosperity," mindless of everything but what can be purchased, consumed or displayed in a show of self-absorbed pride. As things fall apart--and certainly the center is not holding--perhaps mere anarchy will soon be loosed on our built-on-the-shifting-sands-of-lies world. Science Matters: Global Warming--Read These Two Essays June 29, 2007 I am not a scientist by trade, but I believe most science is accessible to anyone with a high school education and a willingness to learn. For example, the vast majority of the articles in Scientific American are accessible to the layman/laywoman, as that is the intended audience. I say this as someone with only high school chemistry and physics in my formal-education science folder, and as a 25-year subscriber to Scientific American. Science is like medicine: if you don't want to learn anything yourself and you just want to trust "the experts," prepare to make some very bad choices. Like agreeing to a needless or risky operation and promptly dying, if not on the operating table, then of an infection you picked up in the hospital. Or taking an ineffectual drug and erroneously thinking you're being "cured." Frequent contributor U. Doran recommended a fascinating dismantling of Big Pharma's (the big drug makers) statistical legerdemaine (slight of hand) The crucial health stat you've never heard of. The article describes how drug companies tout a "relative risk reduction" of 31%, which sounds impressive, but in reality the "absolute risk reduction" is only 2%--meaning, only 2 out of 100 people are going to see any results of the "wonder drug." Not as impressive sounding, right? If you look into the Phase 2 and 3 drug trial data which is used to approve drugs, you will find multiple layers of obfuscation and data-finagling. In other words, flaky data is used to get a drug approved, and flaky statistics are used to sell an ignorant public on the supposed benefits of the (expensive, immensely profitable) drug. Speaking of finagled data: here are two of the best, most clearly presented essays on Global Warming you'll ever find, and they are exclusively here at Of Two Minds. We've all read about global warming, and here we have two articles which explain the basis (data) for the global warming thesis, and how it all stacks up. You really owe it to yourself to read these this weekend. Global Warming: Our Story So Far by Michael Goodfellow The Hockey Stick Breaks (Global Warming Data refuted) by Protagoras I think we as a society have absorbed the negative view that science is "too hard to understand," which makes for a handy excuse to "trust the experts." Yes, at very high levels, say, senior-college level classes, then chemistry, biology and physics are technically challenging because you need a large foundation of knowledge to understand "state of the art." But as Scientific American and other science magazines show, even the highest-level science can always be explained in a way that virtually anyone can understand should they desire to do so. As someone who is blessed to count working scientists as longtime friends, I have learned that data collection is the name of the game; if you don't have good data, i.e. data which hasn't been tainted, and which can be repeated in other labs or locales, then you have nothing. Here is an excerpt from Protagoras's look at the validity of the data being used to support the "humans are causing Global Warming" thesis: A truly dramatic event in contemporary intellectual history occurred unnoticed in April. To understand it, you have to understand the history of the famous Hockey Stick climate chart, which has decorated IPCC documents since the late nineties, appeared in lots of Green publications all over the world, and has been used as vivid proof that human caused global warming (AGW) is real and an imminent threat to human life and civilization.And here is an excerpt from Michael Goodfellow's summary of the evidence pro and con for the "humans are causing Global Warming" thesis: Like it or not, real or not, global warming is a huge problem for the world. Serious debate is going on about what to do, government action on this is already affecting us all, and will continue to do so. The potential effects of legislation on the world economy, the politics of trade and on our lifestyles are all huge. So it makes sense to follow this debate as closely as you follow any other big issue, from the housing bubble to the Iraq war. The problem, as usual, is getting some context and separating the facts from the political bias.Both essays provide numerous links to other sources, so you can explore the topic further with just a few clicks. I am deeply indebted to these writers for investing so much energy and time to bring a clear-eyed, well-reasoned perspective to the most important topic of our era. Please take advantage of this opportunity and read these two wonderfully written, well-researched essays. Thank you Roger H. ($20) for your generous donation to this humble site. I am greatly honored by your encouragement, and your readership. All contributors are listed below in acknowledgement of my gratitude. China's Brand and the Product Liability Lawsuits to Come June 28, 2007 Correspondent Cheryl A. recently alerted me to an issue which may well affect China-U.S. trade: defective products and tainted food. here are two links to the Wall Street Journal (subscription required), but the stories are available from many other sources. Accident Raises Safety Concerns On Chinese Tires China Shuts 180 Food Plants Amid Food-Safety Concerns The two big questions are: Is this merely an anomaly, or the tip of an iceberg of defective, dangerous products? and, Can China fix its quality control problems, or are they endemic to its political/economic structure? The Chinese government's first response was to impound some dried fruit from the U.S. and proclaim it dangerously tainted. In other words, "See, you make tainted products, too! So lay off already!" This face-saving gesture went over like a lead balloon, so their next step was to shut a few dozen plants (out of tens of thousands) for a few days. This is the public-relations equivalent of a bulldozer crushing a few thousand pirated DVDs while the cameras roll. Meanwhile a few kilometers away the piraters are making new copies by the millions. Given the vast quantities of foodstuffs such as farmed seafood now being imported from China, the possibility exists that the next tainted-food deaths will not be pets but humans. As various news agencies have reported, humans in other countries have died from consuming Chinese-made drugs which were adulterated with cheap (and poisonous) fillers. As for seafood, consider this recent article from the San Francisco Chronicle: Domestic farmed fish go under the microscope: "Most of (the seafood) we eat that's farmed is coming from China. We have little idea of what's happening in China," said Peet. Food and Water Watch reports that the United States imports 80 percent of the seafood we consume, most of it from Latin America and Asia. The aquaculture practices in many of these countries damage the environment, and many enterprises use additives and antibiotics banned in the United States.Are you still willing to put a Chinese-made tire on your car or truck? I didn't think so. How about when you read about somebody getting sick from some imported seafood which happened to be grown in China? Will you start asking where that jumbo shrimp came from? China has no lock on unregulated industries, of course; there's no way to know what might be in the food which is imported into this country because inspections and testing are virtually non-existent. Exactly how are you going to insure the quality of every jumbo shrimp and tomato? It boils down to trust. In this sense, every nation is a "brand." Back in 1965, Japanese products consisted of cheap toys and transistor radios which were widely mocked as "cheap" and poor in quality. Fifteen years later, the Japanese were challenging American and European auto manufacturers with vehicles a leap ahead in quality and durability. (The Volkswagen Beetle's demise can be correlated to the emergence of the Toyota Corolla and Datsun cars.) It's been fifteen years since China emerged as a manufacturing power, and what they're producing is defective tires, bikes, etc. Various financial pundits with no knowledge of China are fond of saying it will follow the same path to fanatic quality control trod by the Japanese and Koreans (why? Because they're Asians), but this thesis doesn't take into account the following conditions in China which were not present in Japan or Korea: 1. China is deeply and pervasively corrupt at all levels. If you deny this, you simply don't know any Chinese citizens well enough to hear the truth. Your kid doesn't do well on an entrance exam? Some "help" can be arranged. Your factory is dumping toxic pollutants into the air? You can "arrange" to close for a few days and then start running it at night, when the toxic plume isn't visible. The stories are as varied as they are endless. Thus the idea that the quality of anything can be regulated by a trustworthy, uncorruptible agency within China is simply impractical. 2. The dynamism of the economy and its entrepreneurs makes quality control difficult. Entrepreneurs in China often change businesses and locales quickly; thus a fish farm which is closed for over-using antibiotics will close and the owner will enter another business. The bike manufacturer will close if the market dries up and start making something else. While this dynamism is great for employment and growth, it makes external quality control basically impossible. The global corporations can of course control quality in their own factories, but much of the industry in China is localized production of parts and goods made by small businesses. Where did that tainted pet food come from? It took a major investigation of the convoluted, poorly documented supply chain to find out. 3. Quality is not Job One. Those of you who have a religious faith for the "endless growth of China" story will balk, but again, you need to talk to actual real live people, Big Noses (Caucasians) and Chinese, about actual business practices in China. Sure, if you tour a computer parts factory owned and operated by Taiwanese (yes, I have), it all looks great. If you work for a global corporation in a clean little cubicle and frequent watering holes in fancy Shanghai hotels, it probably all looks great to you, too. But what about the silk suit manufacturer down the road, who sold the French guy based on a high-quality silk product and then delivered 50,000 lower-quality suits? Or the pharmaceutical plant which closed over in the business park because their product packaging was quickly pirated and filled with sugar pills, thus destroying the brand? These are real stories, and they're not from 15 years ago. 4. The idea that U.S. agencies can monitor, document and test for quality is a non-starter. Which of the thousands of containers coming from overseas are you going to inspect? How many bottles of medications are you going to laboriously test to make sure it actually contains what the label says it should? It's impossible. It comes down to trust. At some point, let's be original and call it a tipping point, a country's "brand" will fall into distrust. And as any company knows, once the public has lost trust in your brand, it is very difficult to get it back. Could China's "brand" become irrevocably tarnished? It may depend on how many lawsuits get filed and how much publicity is generated--for instance, Wal-Mart prevails in suit over defective bikes made in China. It's no surprise that Wal-Mart would win; they'll probably always win. But if enough suits get filed, they may lose anyway--by losing their customers. I asked fellow blogger and attorney Fred Roper for his take on product liability, and his comments are insightful: My knowledge regarding products liability cases is pretty limited. The rule is: if a merchant sells a product to a user or consumer that is unreasonably dangerous and causes harm then that merchant is liable for the injuries to that user or consumer. Because of the nature of the distribution chain, a plaintiff and sue anyone or everyone in the chain of distribution. The reason for this is that the merchant is presumed to be in a better position to know the potential dangers that the product poses for an unsuspecting consumer. Therefore, the defense of "comparative" or "contributory negligence" is not normally available to defendants in these kinds of cases.Okay, so actually proving negligence on the part of Chinese manufacturers or U.S. distributors and retailers is going to be near-impossible. But the publicity generated by these cases may slowly cause American consumers to start asking where this tire or bicycle was made, and ask where this jumbo shrimp was grown. If they start making decisions based on where these products came from, trade between the U.S. and China could take a direction few expect. Thank you James D. ($25, third donation) for your generous and encouraging donation. I am greatly honored by your continuing support of this humble site. All contributors are listed below in acknowledgement of my gratitude. Does Short Interest Really Support the Market? June 27, 2007 To those of you who tire of financial and stock analysis--my apologies. The reason why I am concentrating on this topic this week is the market may be poised to move dramatically-- which provides an opportunity for us small-fry to profit, should we guess the direction of the move, or hedge our bets properly. Disclosure: I took a short position via puts yesterday in CFC and FNM, two stocks I discussed in the Monday entry. I anticipate them skyrocketing, now that I am short. One reason to suspect the market is posed to move dramatically is all the major indices are hugging their 50-day moving averages; this suggests indecision. The high volume on major down days like last Friday suggests weakness/distribution, i.e. "smart money" selling to those willing to "buy on the dips." Let's consider one cliche you read again and again: record short interest places a strong bid under the market, providing key support in the event of a sharp decline. As this chart shows, this works at the first test of support; but once the shorts have covered, there's no longer any floor under the stock.

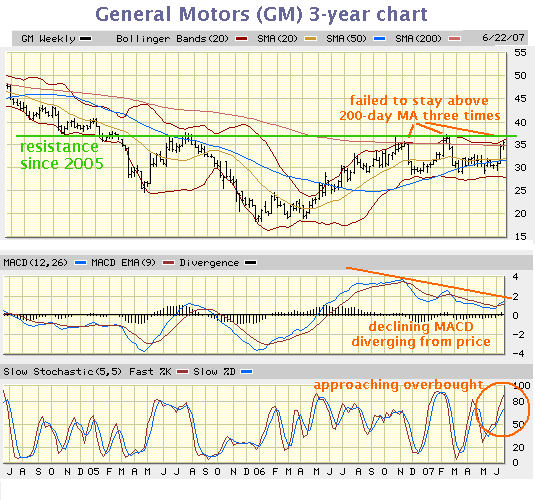

Here's the basic idea: let's say a hedge fund manager owns a million shares of Google; he or she is thus "long" Google. To protect the long position against a sudden drop, the manager sells a million shares short, or buys put option contracts on a million shares. This "short position" fully hedges the million "long" shares against losses. So if GOOG drops $10 per share, the portfolio drops $10 in value on the long side, but gains $10 on the short side--i.e. the shares held short have a $10 gain, as do the puts. Recall that selling short means you received the current price for shares you don't yet own; when you buy the shares later (hopefully for a price lower than you received), then you've "covered your short." The difference between what you sold them for and what you paid to buy them is your profit. Headlines blare that "short interest is at new highs." So guess what percentage of NYSE (New York Stock Exchange) shares are short. Drumroll, please: 3.3%. Yes, the "record high" short interest is not even 4% of all outstanding shares--about 12 billion shares, or four days' trading volume. This is an awfully small percentage of shares to support the idea the market can't decline very much. Let's stand in the shoes of the hedge manager for a moment. Let's say you sense GOOG is weakening--say it's dropped below the key technical level of the 20-day moving average. Why would you hold your long shares if you detected a downtrend in the making? You'd sell (distribute) your long shares, and hold your short shares or puts until the dust settles. Guess what: every other manager with a long position is thinking the same way. So as everyone dumps their long shares, the selling accelerates the price decline. At some point--again, perhaps the 50-day or 200-day moving average, some managers will "cover their shorts" by buying shares of GOOG. This does provide a temporary "floor" under a stock's decline--but what happens when the shorts have all covered and the price is still dropping? There is no longer any shorts to provide a bid/buying. As this chart (the stock is CFC) shows, once key technical levels which trigger short covering are violated, then the stock continues dropping. You may recall reading contributor Harun I.'s comments on the Pareto Principle in Hedge Funds and The Pareto Principle (February 19, 2007). The principle is often called the 80/20 rule, and it has an adjunct: the 64/4 rule. Hmm, isn't it interesting that short positions are about 4% of the market. The principle suggests that small number of shares can have an effect far larger than their percentage would suggest, causing major shifts in 64% of all shares. Proponents of the "short covering will support the market" idea are convinced the 4% covering will support the 64% of stocks declining; they may be right for awhile, but when the 4% have covered, the effect might be to remove the last leg of support from a market which then goes into a free-fall. Why is short interest rising? There may be two reasons. One is the growth of hedge funds, which hedge long positions by going short. (Many mutual funds are restricted from having large short positions.) The other might be that those who tend to go short--i.e. professional managers and traders--are making sure they will profit should a sharp downtrend occur. To summarize: take all assurances that "record shorts will support the market" with a hefty grain of salt/skepticism. Hedge funds may unwind both long and short positions in a hurry, further draining the pool of shorts which need to be covered. Thank you John G. ($26.26) for your generous and interestingly numerated donation. I am greatly honored by your support of this humble site. All contributors are listed below in acknowledgement of my gratitude. If you found value here perhaps you'd like to Your readership is greatly appreciated with or without a donation. The 9 Biggest Mistakes Investors Make June 26, 2007 NOTE: Readers Journal and essays have been updated. A certain investment service has been buying full-page ads in major U.S. newspapers touting their free report, The 8 Biggest Mistakes Investors Make. Ha, I sneer at their mere 8, and handily trump them by offering The 9 Biggest Mistakes Investors Make. 1. Investors purchase stocks, bonds or real estate in the months of January, February, March, April, May or June. 2. Investors purchase stocks, bonds or real estate in the months of July, August, September, October, November, or (horrors) December. 3. Investors base their decisions on investment newsletters hyped in full-page ads or on the "financial" TV channels rather than on their own analysis. 4. Investors rely on "hot tips" from blogs and websites rather than sweat through their own analysis. (Yes, blogs like this one) 5. Investors confuse goateed raving lunatics providing free entertainment in the form of "investment advice" on TV with trustworthy expertise. 6. Investors buy Kraft Foods (ticker KFT) because they like Cheez-Whiz, e.g. "buy what they know." 7. Investors obsess over high-falutin' math (standard deviations, etc.) and obtuse technical signals (The Titanic Signal, etc.) while ignoring the most basic formula of investing: Hope + Greed + Ignorance + Fear = Losses. 8. Investors focus on the "buy" button but forget to hit the "sell" button until it's too late. 9. Investors actually give credence to investment banks and buy-side analysts' recommendations--for instance, the recommendation yesterday to "buy General Motors." Now this must be right, because it comes from Goldman Sachs, right? Goldman Sachs analyst Robert Barry upgraded General Motors (GM) to buy from neutral in what he described as a "tactical trading call." He also raised his price target on the shares to $42 from $29. GM's stock price "implies little to no downside and potentially large upside from the real possibility concessions end up even larger than what is priced in," he said in a note to clients.Count me skeptical, but even though this analyst from the fine firm which provided us our current Treasury Secretary says there is "little to no downside" in GM, let's look at a simple chart:

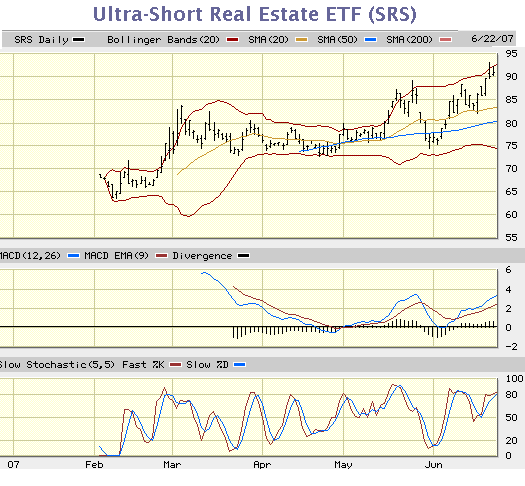

"Little to no downside"? I guess a drop from $37 to $20 doesn't count? A target of $42, when $37 has been ironclad resistance since early 2005? What alternative Universe does this analyst think GM inhabits? Never mind that a purely technical view suggests this stock is a beautiful short (i.e. primed to drop significantly)--take a gander at the MACD divergence, if you will--what about the fundamentals of the company's business? Is the consumer in fine fettle and raring to take on even more auto loan debt? Does GM have a profitable small-car line as gasoline retrenches at $3/gallon on its way to $4/gallon? Do they manufacture a hybrid lines of vehicles to compete with Toyota and Honda? Is there any published analysis which proves modest "concessions" from the UAW will transform an essentially bankrupt corporation (its pension and retiree healthcare liabilities far exceed its assets) into a viable firm? Allow me to sumamrize: there is absolutely no technical reason to believe GM is heading to $42, and much evidence it's heading to $20, if not $ .20. There is absolutely no evidence that GM is not a technically bankrupt company heading for formal bankrupty in the next recession (scheduled to begin in October 2007). Yet here we have "reputable analysts" from "reputable firms" (gag!) telling suckers, I mean "retail investors," to gamble their hard-earned money on a high-risk bet. Why? Probably so Goldman Sachs and its big clients can distribute/dump/unload their doomed shares of GM onto poor suckers naive enough to believe their "recommendation" isn't purely self-serving. Is there no shame? None whatsoever. Caveat emptor, Baby. Let the buyer beware. NOTE: At the time of posting this entry, I did not have any position in GM. However, I did profitably buy puts on the stock the last time it hit $36. That is disclosure, not advice. EXTRA SPECIAL BONUS NOTE: "The Titanic Signal" is a fabrication/satire. It is my invention. Oh, and by the way, it's flashing a huge gleaming red "sell". Thank you Cheryl A. ($25.00, third donation) for your generous and quite unexpected donation. I am greatly honored by your continuing support of this humble site. All contributors are listed below in acknowledgement of my gratitude. Profiting from the Housing Bubble Popping June 25, 2007 Is there some way to profit from the deflating housing bubble? Perhaps. Let's get one thing straight: the following is not investment advice. It is merely a series of "if-then" statements with which you may or may not agree. IF you believe that the real estate industry is losing steam/trending downward/dropping in value, THEN note that the Ultra-Short Real Estate ETF (exchange-traded fund) rises 2% for every 1% drop in the ETF's constituent stocks--hence the descriptor "ultra-short." ETFs trade like stocks. Here is a chart of the fund, which only started this year; note that it rises in value as the ETF drops in value.

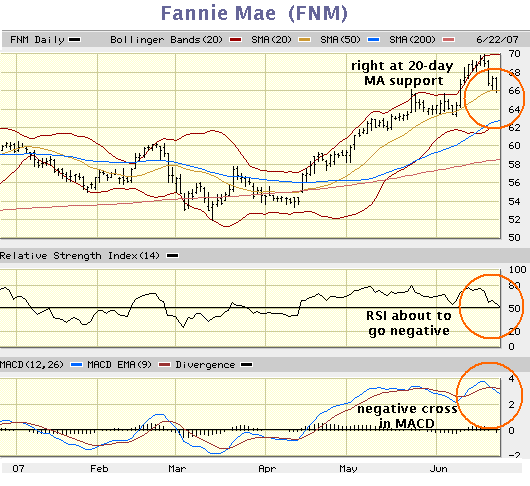

IF you believe that Fannie Mae, the quasi-government mortgage outfit, holds a lot more risky mortgages and debt than Wall Street reckons, THEN note the negative indicators on this chart which support the notion that this stock is about to drop through its 20-day moving average support:

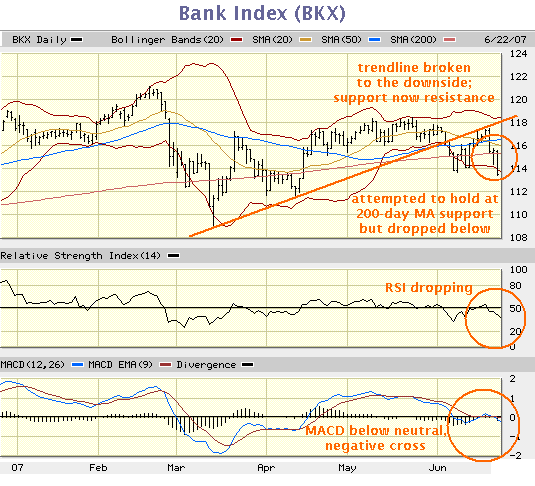

IF you believe that the entire banking/lending sector holds a lot more at-risk debt than Wall Street reckons, THEN note the negative indicators on this chart; this ETF has dropped below the critical 200-day moving average support:

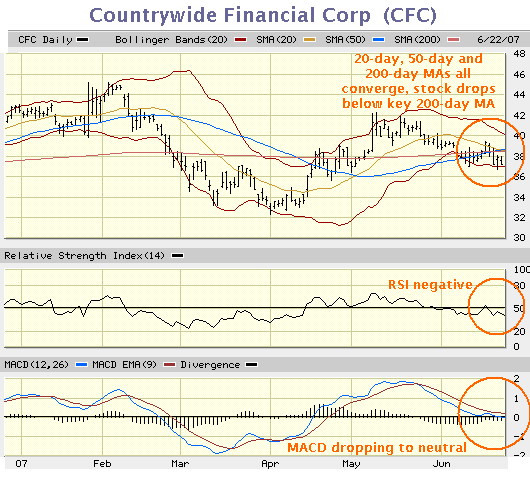

IF you believe that lenders such as Countrywide Finance Corp. hold substantially more at-risk (subprime, ALT-A, ARM) mortgages than Wall Street reckons, THEN note the negative indicators on this chart; this stock has dropped below the critical 200-day moving average support:

IF you believe that a stock/ETF will drop in price, and you want to gain from that drop, THEN you either sell the stock/ETF short or purchase put options on that stock/ETF. IF you aren't familiar with these terms, THEN please do some Web searches to find out more. TO REPEAT (sorry for shouting): none of the above, or anything on this site, is investment advice. It is a series of if-then statements with which you are free to disagree, ponder, ignore, explore, etc. NOTE: at the time of this posting, I have no position in any of the securities mentioned above. If you found value here at "an ad-free, rigorously civil exchange of ideas and knowledge," perhaps you'd like to Your readership is greatly appreciated with or without a donation. This Week's Theme: Context On-The-Ground Reporting in China June 23, 2007  Longtime correspondent Martin recently recommended an article on China

The Empire of Lies by French free-lance journalist Guy Sorman.

Longtime correspondent Martin recently recommended an article on China

The Empire of Lies by French free-lance journalist Guy Sorman.

What separates Sorman's report from the typical China story is his on-the-ground journalism with people and places rarely visited by Western media types. In case you didn't know, the Chinese government employs a vast army of people to manage/spin news, not just for its own citizens ("The Great Firewall of China" to censor the Web) but for the outside world as well. It takes some real digging to get past the bogus government statistics, cover-ups and lies. Sorman does a fine job, one which can't be denied or dismissed by cheerleaders. Here's a taste of his reporting: It had taken me several months and many intermediaries before I could finally meet with this self-effacing, frail 75-year-old, branded an enemy of China by the Party�a label it gives to anyone with the temerity to oppose the regime.Here is his report on the central government's response to AIDS: The government�s initial reaction was to deny any problem, isolate AIDS-affected areas, and let the sick die (a pattern that initially repeated itself when SARS broke out in the country).To extend our theme of Context with a Capital C, let's consider how little understanding of Chinese culture goes into the standard U.S. financial analysis. To take but one example, financial analyst John Mauldin is recommending a book by PIMCO (bond fund) manager Paul McCulley and veteran reporter Jonathon Fuerbringer, Your Financial Edge. From Mr. Mauldin's review, the book seems to have much good analysis of big issues; but the authors' lack of understanding of Chinese culture is striking. Here is a quote: "Ultimately, though, China will switch from a mass production economy to a mass production and mass consumption economy and have the courage and ability to free its exchange rate and shift away from its mercantilist model."I wonder if either of the writers actually knows any mainland Chinese people. Why do I wonder? Because every one of our many Chinese friends has paid off their house mortgage within a few years of its purchase. This is true regardless of which city they came from in China (central, coast, Nanjing, etc.) and regardless of their salaries: those with substantial incomes bought more expensive houses, and those with more modest salaries bought less expensive houses. How many non-Chinese Americans do you know who pay off their mortgage in 5 years? Again, these are not big-bucks doctors and lawyers or people who inherited wealth or trust funds; these are average folks with median incomes. Do you know how they achieved this monumental goal? Scrimp and save. Minimum consumption. No frills lifestyle. And once the mortgage is paid off, do they then begin spending lavishly? No, they buy another property or add on to their house--paid in cash.

If you examine the lifestyles of everyone beyond the few million Shanghai-Beijing-yuppies, you will find a nation, and more importantly, a culture, of prodigious savers. If you know anything about Chinese culture or if you know even a few dozen mainland Chinese people well, you know China will not transition to a culture of consumption in this generation. A very good anthropological case could be made that China will never leap from a culture of savers and investors to one of borrowing and consumption. Not in five years, 20 years or even 100 years. Economies may change quickly, but cultures do not. Yes, Proctor and Gamble is selling Crest toothpaste to residents of small villages in western China. Chinese people will buy TVs, meat, seafood, and a variety of other consumer goods. But to claim that China's culture and economy will seamlessly transform from a mercantilist export-driven model to a consumerist clone of the U.S.--based on what evidence? A few million free-spending yuppies out of a nation of 1.2 billion? If you think that's a sound footing for an analysis of an enormous nation, then do you base your prognostications for the U.S. on the top-income residents of Manhattan? If so, your analysis will be fatally flawed. Yet financial writers continue to accept the most breathless extrapolations for Chinese consumption based on the spending of an equivalent handful of rich, top-of-the-heap free-spenders who can be seen in hotel bars and fancy restaurants in Shanghai and Beijing--the kind financial journalists apparently base their "research" on. If you haven't read my own attempt at providing a broad context for China's economy, here it is: China: An Interim Report. For more on Chinese patterns of consumption and saving, please read the June 5 entry, Can the U.S. Go Down and China Stay Up? Thank you Matthew N ($10.00) for your generous and quite unexpected donation. I am greatly honored by your support of this humble site. All contributors are listed below in acknowledgement of my gratitude. This Week's Theme: Context Little Miss Sunshine and American Optimism June 22, 2007 Is the incredibly wicked satire of last year's independent film hit Little Miss Sunshine Do other cultures breed a hyper-competitive drive for "number one" rankings in everything from piloting USAF jets to talent contests to wealth and recognition on the motivational circuit to academic studies of Proust? Do other cultures quickly label everyone who competes but doesn't win "a loser"? Do other cultures heap such lopsided praise on "winners" and offer so little to the "rest of us" that suicide (at least in this film) seems like a better alternative than slipping in the rankings? I honestly don't know, but I suspect not. In the event other cultures may be mystified by the dark humor and rapier-like parody in this film, I offer up the following as context for understanding this justifiably popular movie. I am not immune to competitive juices, so I say this not as a smarmy putdown of competition but to draw the distinction between the honor implicit in competing and the pathological emphasis now placed on "winning" "the top spot" in American society. I played on basketball teams for five years in junior and high school and a year of football in 10th grade (hard-working talentless benchwarmer, but hey, I had fun being part of the teams), and I was a contractor/carpenter in the deep recession of the early 80s. You want a "Darwinian fight to the death?" That was the "interest rate is 16%, nobody's building anything" reality then. And if you want a competition where winning is literally one shot in a million--try writing. 30 million blogs (or is it 300 million?), 5,000 novels published each year, 100,000 books in print, blah blah blah. The point is: has our society veered into a pathology of winning, in which parents are punching Little League coaches and screaming at little kids for not scoring more than their opponents? This film says yes, definitely, categorically, yes. Critics generally describe this as a comedy about a dysfunctional family. It isn't that at all; it's a biting critique of a dysfunctional society. The family is actually the only source of support and solace available to the beleagered individuals depicted in the film as they each strive--and painfully fail to reach--the pinnacle of the American Dream: success through hard work and meritocracy. The banality of this goal is ruthlessly satirized as the movie progresses. Every conceivable form of American Success with a Capital S is savagely revealed as distorting and empty. The daughter's painfully bawdy routine--a searing exaggeration of the contest's subtext of pushing adulthood onto little girls--draws predictable howls of outrage from the contest authorities, and rallies the family to her side. Though other bits of American life get similarly skewered, the key satire is of The American Dream: wealth and recognition achieved via hard work and "pursuing your dreams." As the wheels fall off the U.S. and global economies, I have to wonder how Americans will adapt to the narrowing of opportunities and the ever-tightening strictures of debt and job losses. I wonder if they will begin to understand the myths they bought into and clung to so tenaciously as their plight deepened, ("the Ownership Society funded by leveraged debt", for instance) and realise that if they bothered to vote (recall that U.S. voter turnout is a miserable 40% compared to 80% in France and other well-established democracies), they might regain the political power which they have so passively ceded in their individual obsession with competitive triumph and public recognition. Thank you Jaimi A. ($10.00) for your generous and entirely unexpected donation from the country so many Europeans would like to retire to. I am greatly honored by your international support of my humble efforts. All contributors are listed below in acknowledgement of my gratitude. My sincere thank you to all 124 readers who have contributed money, art, music and food in the 3 months since I began accepting donations to this humble site. This Week's Theme: Context Sword of Doom June 21, 2007 Normally you could safely assume an entry entitled "Sword of Doom" refers to some financial meltdown, but today we refer to a classic samurai film. This week's theme of context requires at least one cultural entry, for there are few more dangerous minefields than context-free cultural misunderstandings. "Why can't they be more like us?" A universal plea, to be sure. Since movies can offer an uncannily accurate window into a culture, let's consider a 1966 Japanese classic of the samurai genre, The Sword of Doom

As those of you familiar with the genre might expect, Sword of Doom depicts tremendous violence. Most of the swordplay is highly stylized, but if seeing 20+ swordsmen cut down is not your cup of tea, you might decide to pass on the film. In a way, that would be a shame, for this film speaks not just to Japanese culture and history, but to universal themes of evil and revenge. The movie stars the incomparable Tatsuya Nakadai as a heartless--some might even say sociopathic-- samurai who has mastered a non-standard, unorthodox style of kendo or fencing. Perhaps it is his unorthodox style, or his ruthlessness, or both, but he has been kicked out of his kendo school. This establishes him as a ronin, or masterless samurai--in our nomenclature, a lone wolf. The movie is set in a time of social dissolution and turmoil, the early 1860s, when the feudal order which had held sway over Japan for over 200 years was breaking apart. The Meiji Restoration of 1868 restored social order by dissolving the Shogunate in favor of the Imperial household. (In practical terms, a ruling-class oligarchy was established.) Thus later in the film, Nakadai's mistress bemoans his lack of standing, commenting that in earlier time, he would have had his own kendo school and they could have lived comfortably. Instead, Nakadai is forced to hire himself out as a political assassin for a pittance; he consoles himself by drinking prodigious quantities of sake (rice wine). Early on, Nakadai dispatches an unarmed elderly man and shortly thereafter, an opponent in what was supposed to be a non-lethal match. (In exchange for her favors, he'd secretly agreed with his opponent's wife to throw the match. Alas, the cuckolded husband tried to dispatch him, forcing Nakadai to kill him.) These unsavory scenes establish Nakadai as ruthless, amoral and maddeningly difficult to kill. Nonetheless, the outlines of his own unorthodox code of conduct are visible. The elderly man had been praying to be released from this life; overhearing the gent's plea to Buddha, Nakadai took it upon himself to grant the man's stated wish via his sword. And Nakadai held to his bargain with the other samurai's wife, allowing the match to be a draw, until his opponent tried to kill him with an illegal move. But there is a karmic consequence of these needless killings, and a subplot of revenge is set in motion, building our anticipation of a classic showdown in the final reel. But our expectations are foiled. I won't give away the ending, except to say it is not the one-on-one "good guy versus bad guy" showdown we are led to expect, but a harrowing melee in a burning Japanese house in which Nakadai takes on the entire clan who'd engaged him as a sword-for-hire. Online sources say this "unsatisfying" ending results from the film originally being planned as the first of a trilogy. I respectfully submit that the filmaker designed this movie to stand on its own, and deliberately chose a very 1960s "anti-expectation" ending. This final climatic sword battle--truly one of the great action sequences of world film, in my humble view--is unleashed by a betrayal (the clan tries to kill Nakadai) and a ghostly visit by Nakadai's victims, who haunt him to the edge of madness. One online reviewer scoffed at this haunting (shall we also then dismiss Shakespeare's Hamlet?), but ghosts (obake, spirits, etc.), animism and various superstitions are key elements of Japanese culture. That Nakadai's descent into madness begins with a haunting is essentially Japanese. Those of you who are Japanese or who have lived in Japan for years may disagree, but I see this film as a critique of the Japanese reverence for mastery--an unplanned, subconscious critique or a conscious one, I can't say. Acting legend Toshiro Mifune plays the master of another kendo school, and in a meeting with Nakadai he proclaims that "The sword is the soul. Study the soul to know the sword. Evil mind, evil sword." For his part, the Nakadai character exclaims, "I trust only my sword in this world. When I fight, I have no family." That is, he has no loyalty to anyone but himself and his mastery of the sword. Mifune's comment--the sword is the soul--embodies the ideal of mastery; in Japan, masters of craft are revered as Living Masters. Mifune is proclaiming a moral truism: if the heart is evil, so too will be the mastery. But Nakadai's character also expresses an ideal of mastery--that of one unbound from loyalty and obligation to anyone or anything but the mastery itself. Perhaps the theme many Japanese viewers would identify is this: mastery without loyalty and duty is inherently unstable and ultimately dangerous. In American Westerns, such as the 1960s Clint Eastwood films A Fistful of Dollars and For a Few Dollars More (which were based on Kurosawa's samurai classics, Yojimbo and Sanjuro), the anti-hero is a higher-order hero, wreaking a justice which the orthodox lawman could not pursue. In this 1966 Japanese anti-hero classic, the Nakadai character is not a source of justice or righteous vengence, but a "loose cannon" who is dangerous to all around him, an uncontrollable force so evil that his own father wants him killed. Can we view this film in a cultural vacuum, knowing nothing of Japan's history and culture? Of course we can; but without such context, key themes of the movie may well be indiscernible, just as much of Japan will remain hidden to the casual visitor. Critic's Disclosure: I studied Japanese language (and therefore a bit of written Chinese as well, as kanji are Chinese characters), geography, history and literature, as well as Korean poetry and Chinese philosophy at university. I have visited each country for extended periods but remain a mere student of these cultures. Sadly, my limited Japanese language skills have been reduced by time to rubble. Thank you Susan P. ($20.00) for your generous and entirely unexpected donation. I am greatly honored by your support. All contributors are listed below in acknowledgement of my gratitude. This Week's Theme: Context How the Housing Bubble/Credit Bubble Will Pop June 20, 2007 When 2008 rolls around and the U.S. economy is sinking with frightening momentum into a bottomless quagmire, you'll be glad you read this entry. Why? Because you anticipated every step of the implosion and warned your friends who were still floating complacently down that river in Egypt (de-nial). In keeping with our theme of context, let's begin by noting that the proper context for the housing bubble is the all-encompassing global credit bubble which has inflated every asset class. With this fundamental firmly in mind, let's follow Deep Throat's advice from the classic film All the President's Men Let's first dispense with "the real estate market". Yes, supply and demand and housing starts and zillow.com and neighborhood sales and all the other market stuff play a part in the coming implosion, but all that noise is more a sideshow than the Main Event. Why? Follow the money. The main event is the credit market, because if you can't borrow money, or can only borrow it at a premium and under tight conditions, then how many houses are for sale in your neighborhood or the median price paid, etc. shrink to near-meaningless. Real estate sales and valuations depend solely on credit. Everything else is secondary. Next, let's dispense with the notion that the implosion of housing-based lending can be "quarantined" and won't affect the economy. The reason is that mortgage-backed securities, and the CDOs and other derivatives which have been piled in untold trillions onto them, are one leg of an increasingly wobbly three-leg stool. The second leg is so-called "junk bonds" and other commercial paper (which has ballooned to astounding levels--see chart), and the third is government bonds in all their flavors. Once the MBS leg snaps, the entire debt stool collapses.

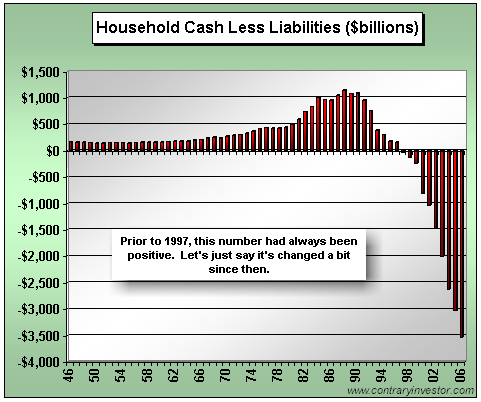

Third, let's note the critical role real estate ownership, sales and high valuations play in funding local and state governments. Government at all levels is about 25% of the U.S. economy, though in many locales it's more like a third. As mortgage rates rise and credit tightens, real estate sales fall, cutting transfer taxes; as prices fall, homeowners demand lower assessment values, further reducing tax revenues. And as frequent contributor Harun I. noted in submitting this link, local governments desperate for property tax payments are rushing the foreclosure process, dumping the foreclosed (and often trashed) home back on the lenders or builder, who then has to pay the taxes themselves before they can even auction the property off to a new buyer: Hundreds delinquent on taxes: In the Village I No. 2 district, between 5 and 6 percent of homes are delinquent while about 14 percent are late in Fairview Village. In Patterson, the delinquent taxes make up 16.43 percent of what residents in the subdivisions owe.Let's say you're a lender or builder on the edge of bankruptcy. (Yes, there are many more than you might imagine. Please see Aaron Krowne's Mortgage Lender Implode-O-Meter site for more.) You suddenly get hundreds of overdue property tax bills to pay, in cash, before you can even put the distressed houses on the auction block. Might these hundreds/thousands of property tax bills be the straw that breaks the lender's back? Believe me, the bills in California are humongous; multiply $10,000+ a year by thousands of foreclosed McMansions and you come up with some serious money due the local governments. And who, pray tell, will pay the tax lien when the lender (owner of last resort) goes belly-up? Sure, the bankruptcy court will pay the liens, but only if there's enough money left to do so. But what if the lender is well and truly stripped of cash/assets? Then what? The local government eats the taxes due--unless they try to collect in escrow when a new owner buys the property. This may work if you're talking about a $500,000 property with a $10,000 tax bill, but what happens if the process drags out, and the tax bill grows ever larger? The net proceeds from the eventual sale (assuming a buyer can be found) might well be most or all of the proceeds, leaving the holder of the mortgages with a mere fraction of the principle and none of the interest. But isn't the value of all those trillions in mortgage-backed securities based solely on the income streams generated by mortgages? What's their value if those streams dry up? That's right, the value of those MBS and all the derivatives downstream drops--a lot. And when that happens, a credit contraction or crisis occurs. For an excellent description of exactly how this can unfold, I reprint (with permission) a commentary by Karl Denninger, proprietor of the insightful Market Ticker and several other sites. I think people have been trying like hell to keep the credit market bombs quiet, and they succeeded - until this evening, when it came out that Merrill seized $400m worth of Bear's Hedgie bonds.To summarize: Say I'm a pension fund manager seeking higher yield (alpha) so I buy $100 million tranch of a mortgage-backed security, which a rating agency has, in its infinite wisdom, rated AA. My fund isn't allowed to buy less than AA, so everyone's happy. Until the underlying mortgages slip into default. Oops, the income stream is drying up. Now what? Well, there's no market for this security-- no "mark to market"--so I can hide my little mistake in the portfolio, keeping the $100 million value on it (and not coincidentally, my job). But alas, all good things come to an end, and when the rating on the MBS is dropped to BB, I have to sell it--or try to sell it. A frenzied calculation is made. Hmm, it seems the open-market value of this risky security is $5 million, tops. Not only do I lose my job, but the pensioners depending on the fund growing and producing income are in for a shock. The fund just plummeted in value and can no longer meet its pension obligations. Sorry, folks; I was just seeking alpha. Let's check the quarantine. Foreclosed homeowners: financially destroyed. Bankrupt lenders and all their employees: ditto. Local government: facing sharply reduced tax income. Since 80% of local government costs are for employees, then the only choice is lay-offs. Pension funds: income and value drop, causing pensioners to accept cuts or current employees to pony up much higher contributions--or both. Credit markets: in full panic, new loans and mortgages made only to the very lowest-risk, premium customers--in other words, a big chunk of potential home buyers can't borrow money at any price. And let's not forget how precariously perched the U.S. household is on the threshold of insolvency:

I'd say the quarantine was a failure, as the disease seems to be spreading like wildfire. There's one last critical context: the Treasury.

As I have endlessly explained, the Treasury's job is not to keep mortgage rates low; that's up to the bond market. The Treasury's job is to sell government debt via bonds--at whatever the market demands. As I have said many times, there is no Plan B. If no buyers take the bonds off the Treasury's hands at 5%, then they raise the yield until buyers appear. So everyone who is absolutely sure interest rates will drop as the economy plummets is off the mark. Rates might drop, if there's a panic "flight to quality" to Treasuries. But if there is no longer hundreds of billions in easy money sloshing around the world--i.e., the credit contraction is global, and there is no reason to think it won't be--maybe there won't be enough cash laying around to fund our government's enormous appetite for deficits/more debt. That thought is completely alien to a market which assumes the world will forever be awash in cash seeking a return. But when the credit markets turn, and fear replaces panic, then cash dries up--not just cash for mortgages, but even for Treasuries. Since there is no Plan B to fund the government debt, rates will rise, regardless of the impact on the U.S. housing market. The U.S. housing market is a sideshow; the main event is the global credit market. If you'd like more context on real estate bubbles, knowledgeable reader John Brennan recommended this insightful academic paper from 2002 Bubbles in Real Estate Markets by Richard Herring and Susan Wachter (Wharton School). If you found value here, perhaps you'd like to Your readership is greatly appreciated with or without a donation. This Week's Theme: Context What Makes a Bubble? June 19, 2007 New Readers Journal: Nurse Dorothy on sleepless hospitals. Here is an excellent description of the present: Shares rose faster than at any time during the century. House prices were also climbing sharply, producing a boom in the construction of suburban mansions. The Republic lost some of its Calvinist austerity as its people became a nation of consumers, mixing their love of display with an avidly speculative pursuit of wealth.The present it describes is Holland in 1635, at the height of the Tulip Mania. With some very minor editing, this is a quote from Devil Take the Hindmost: A History of Financial Speculation The key context for manias, bubbles, crashes and financial panics is of course the human mind. To quote again from this book: Speculators were, in Vega's words, "full of instability, insanity, pride and foolishness. They will sell without knowing the motive; they will buy without reason." Vega's speculators exhibit many of the features associated with the full range of manic-depressive behavior. A manic-depressive experiences violent and uncontrollable mood swings. As his expectations grow increasingly unrealistic, the manic becomes careless and this precipitates his downfall. Unable to see the broader picture, he becomes fixated on insignificant details.That's a very good description of the psychology of greed and fear--emotions shared by all humans. But what other characteristics of previous bubbles might provide context for our own stock and asset bubbles? Here are three which seem under-reported:

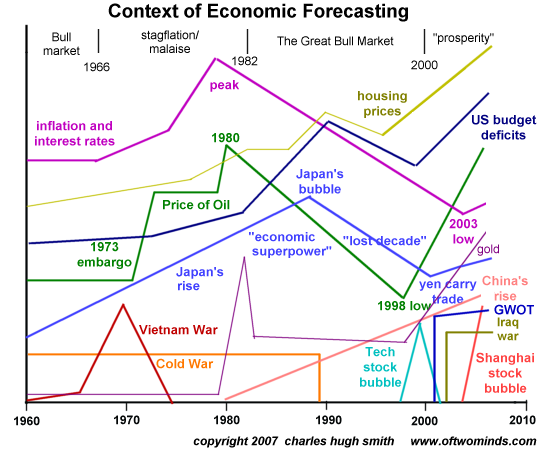

Speaking of insignificant details: Does anyone remember the book-to-bill ratio? During the 1990s tech boom, the semiconductor industry's book-to-bill (orders/shipments) ratio could trigger massive movements in the NASDAQ each month; the report was awaited with breathless anticipation. Now it's merely an artifact of that bubble. Our current insignificant details include phony, manipulated measures of inflation and GDP growth. The initial number is inevitably wide of reality, more a wild guess than truth, yet the invaribaly inflated number moves the market ever higher, even as later downward revisions are utterly ignored. Let's hear a cheer for stock buy-backs! The South Seas bubble of 1720 was based on a variation of the current private-equity/stock buy-back bubble. In our present bubble, it works like this: you borrow $1 billion based on company assets--the value of its outstanding shares--and then you buy $1 billion of shares back and retire them, effectively reducing the float (supply) of stock. This reduced supply means any demand moves the price of the shares up, boosting the value of the company, which can then support another $1 billion loan. Rinse and repeat. Do you see the circularity of this "Bull market"? Rising prices feed more borrowing which raises values even higher which enables more borrowing which... hmm, is this "value investing"? It's more like crass manipulation by insiders--all perfectly legal and even hyped as a "good thing for current stockholders." As for mountains of derivatives and credit swaps built on tulips which can't be delivered--how about all those CDOs and other mortgage-backed securities? All those instruments are based on the delivery of income and/or principle from tranches of pooled mortgages. If the homeowners stop paying the mortgages, then there's nothing to deliver, and the house of trading cards falls. The same also holds true if the homes are foreclosed and sold "as is" for a mere slice of the mortgage; the promised principle comes up short, and all the promises made to holders of CDOs melt like an icecube dropped in the Sahara. In other words, the "value promised"--the interest and principle--become undeliverable. This triggers demands for payment on holders of upstream contracts (CDOs, credit swaps, you name it) who can't deliver, either. As the bottom layer defaults--the homeowners--so too does the next layer, and the next layer and so on to the very pinnacle of the derivative mountain. This is how you get a crash. All the same machinations were in play in 1635 and 1720. Global trade was extraordinarily vigorous and profitable then, too. "Prosperity" was just as limitless as it is now. But the endgame wasn't decades more of wealth-creating machinations; it was financial ruin for everyone who played until the end. Thank you Adrian and Debby G. ($100.00) for your astoundingly generous and extremely unexpected donation. I am greatly honored by your support. All contributors are listed below in acknowledgement of my gratitude. If you found value here, perhaps you'd like to Your readership is greatly appreciated with or without a donation. This Week's Theme: Context A Semi-Long View June 18, 2007 Allow me to summarize the economic Optimists and Pessimists core positions: Which is right? Or are both right? This week's theme is Context, for establishing the appropriate context goes a long way toward resolving apparent contradictions. In this sense, problem-solving (and forecasting) boils down to assembling a context which accounts for the known facts and the influences of history, culture and events. One philosophic word for this is "totalization" (from Critique de la Raison Dialectique). By way of an example: consider welfare. Those ideologically against welfare focus on those gaming the system (the scofflaws and cheats), and other deficiencies such as dependency being passed down to the next generation. Those ideologically predisposed to support welfare focus on those impoverished children and mothers whose lives have been improved by welfare, and those who successfully transition from dependency to the workforce. But the larger context of welfare must include its size in the overall Federal Budget (modest) and various technocratic methods/policies to minimize cheating and encourage job skills and entry-level employment of people who were previously "hard-core unemployed." Belief systems may drive politics but they don't provide context or understanding. To establish some basic context for any economic forecast, I've drawn a graphic depiction of some major forces which have influenced the global economy over the past 40 years.